Why use a broker for debt consolidation mortgages

A broker debt consolidation mortgage is a remortgage that rolls multiple unsecured debts into a single secured loan, managed with professional broker expertise to simplify repayments and reduce monthly outgoings. The industry term for this is a debt consolidation remortgage, and understanding why a mortgage broker is central to the process is the difference between a successful application and a costly rejection. For UK homeowners carrying credit card balances, personal loans, or car finance alongside their mortgage, this approach can cut the number of monthly payments to one and potentially lower the overall interest rate. The broker’s role is not simply to find a deal. It is to build a case that lenders accept.

Why use a broker for a debt consolidation mortgage

A mortgage broker acts as an expert intermediary, translating complex financial situations into cases that lenders are willing to approve. This matters most when you are consolidating unsecured debt into a secured mortgage, because lenders treat that transaction with greater scrutiny than a standard remortgage. Going directly to a bank means your application is assessed by an automated scoring system with no room for nuance. A broker presents your case manually, with context.

Mortgage brokers access a broad range of lenders, including specialist lenders whose products are not available on the high street or through comparison websites. This is particularly valuable if you have a complex income, a patchy credit history, or a high level of unsecured debt relative to your income. A broker at Prosperhomeloans, for example, can approach lenders who specifically underwrite debt consolidation cases rather than forcing your situation into a standard residential mortgage product.

The practical benefits of using a broker include:

- Access to specialist lenders not available directly to borrowers, including those who accept complex credit profiles

- Manual case presentation that highlights compensating factors such as property equity and repayment history

- Holistic affordability reviews that go beyond what online calculators show in terms of hypothetical savings

- Paperwork and liaison management throughout the application and underwriting process

- No offer, no fee structures where typical costs such as legal fees range from £0 to £2,000, sometimes rolled into the loan

Pro Tip: Ask your broker upfront whether they operate on a no offer, no fee basis. Many independent brokers only receive payment when the mortgage completes, which means their incentive is fully aligned with getting you a successful outcome.

The affordability review a broker conducts is not the same as entering figures into a website calculator. It accounts for your existing mortgage balance, the debts you want to consolidate, your income stability, your property’s current value, and your long-term repayment capacity. That full picture is what lenders need to see, and a broker knows how to present it.

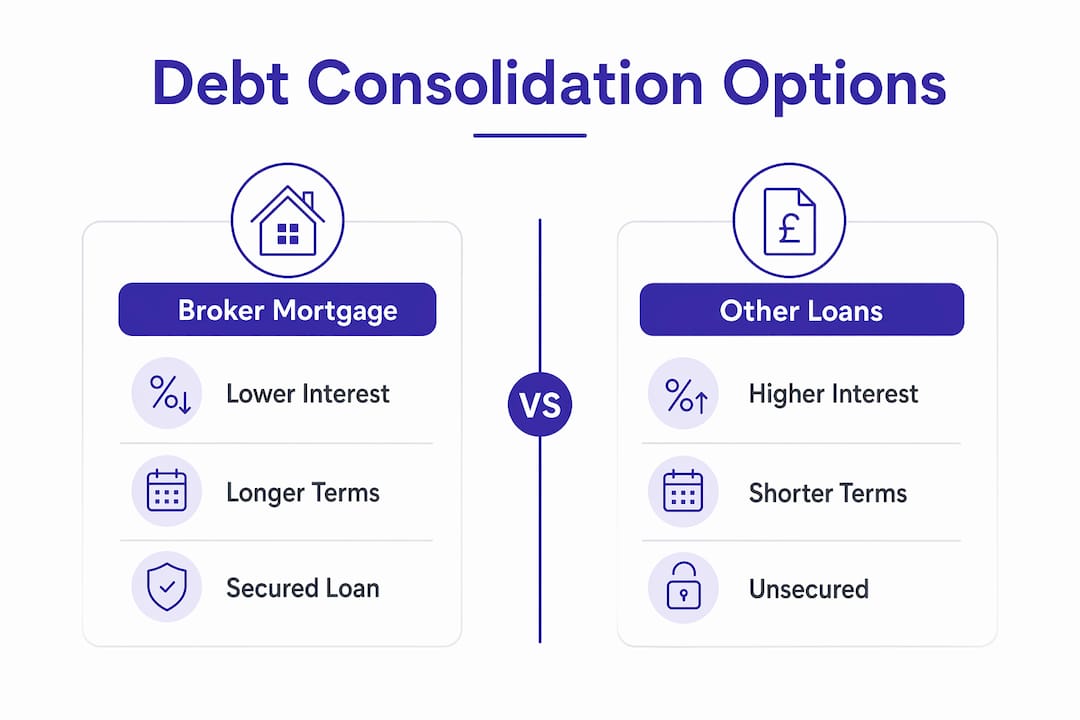

How does a broker mortgage compare to other debt consolidation options?

Understanding the alternatives helps you decide whether a debt consolidation remortgage is the right route for your circumstances. The table below compares the most common debt management strategies available to UK borrowers.

| Option | Typical interest rate | Loan term | Secured on home? | Best suited to |

|---|---|---|---|---|

| Debt consolidation remortgage | 4% to 7% (variable) | 10 to 25 years | Yes | Homeowners with equity and multiple debts |

| Personal consolidation loan | 6% to 20% | 1 to 7 years | No | Borrowers with good credit and smaller debts |

| Balance transfer credit card | 0% introductory, then 20%+ | 12 to 30 months | No | Credit card debt under £10,000 |

| Direct lender remortgage | Similar to broker rate | 10 to 25 years | Yes | Straightforward cases with clean credit |

The key distinction is that consolidating unsecured debt into a mortgage can lower monthly payments by reducing interest rates and combining several repayments into one. However, spreading short-term debt over a 20-year mortgage term means you may pay more in total interest, even at a lower rate. A broker runs those numbers for your specific situation rather than offering a generic estimate.

Personal loans suit borrowers who can manage a higher monthly payment over a shorter term and want to keep their home equity untouched. Balance transfer cards work for smaller credit card balances if you can clear them within the introductory period. The broker remortgage route works best when the combined debt is large enough that the interest saving justifies the transaction costs and the extended term.

Going directly to a lender for a remortgage is an option, but it limits you to that lender’s products and criteria. If your case involves any complexity, such as self-employment, a recent missed payment, or a high debt-to-income ratio, a direct application is more likely to result in a declined decision or a less favourable rate.

What are the risks of consolidating debt into a mortgage?

Debt consolidation via a remortgage carries real risks that every borrower must understand before proceeding. The most significant is that your home secures the new loan. If you cannot maintain repayments, the lender can repossess your property. That risk does not exist with unsecured personal loans or credit cards.

The process of managing those risks responsibly involves several steps:

- Understand the total cost over the full term. A lower monthly payment spread over 20 years may cost more in total interest than the original debts combined. Ask your broker to show you both figures.

- Close the credit accounts you consolidate. Without closing credit accounts post-consolidation, borrowers frequently reborrow, which places their home at risk. This is one of the most common mistakes inexperienced applicants make.

- Build a post-consolidation budget. Debt consolidation is a financial reset, not a solution for overspending. Success depends entirely on disciplined habits after the mortgage completes.

- Commit to a repayment plan. Reputable brokers often require clients to demonstrate a realistic budget before submitting an application, because lenders want evidence of sustainable affordability.

- Monitor your finances ongoing. Debt consolidation mortgages should be part of a broader financial strategy that includes regular reviews, not a one-time fix.

Pro Tip: Before you apply, list every debt you plan to consolidate alongside its current interest rate and remaining balance. Your broker will need this information, and having it ready speeds up the affordability review considerably.

A broker’s value in this context is not just finding a product. It is helping you understand whether consolidation is genuinely the right decision for your financial position, and ensuring the plan you commit to is one you can sustain.

What is the step-by-step process for a broker debt consolidation mortgage?

Knowing what to expect at each stage reduces anxiety and helps you prepare the right documents. Here is how the process typically unfolds when you work with a broker.

- Initial financial review. Your broker reviews your income, existing mortgage, outstanding debts, and monthly expenditure. This conversation establishes whether consolidation is viable and what equity you have available to borrow against.

- Property valuation and borrowing limits. The broker calculates how much equity you hold in your property and what the maximum borrowing would be under responsible lending rules. Most lenders cap consolidation remortgages at 85% to 90% of the property’s value.

- Sourcing suitable products. Using their lender panel, the broker identifies products that match your credit profile, income type, and consolidation amount. This is where access to specialist lenders becomes critical for complex cases.

- Application submission. The broker prepares and submits the full application, including supporting documents such as payslips, bank statements, and a schedule of debts to be consolidated. They liaise directly with the underwriter if queries arise.

- Mortgage offer and legal completion. Once approved, a formal mortgage offer is issued. A solicitor handles the legal transfer, and the new lender pays off the consolidated debts directly in most cases.

- Post-settlement support. A good broker does not disappear after completion. Prosperhomeloans provides ongoing support to help clients stay on track with their repayment plan and review the mortgage at the end of any fixed rate period.

The entire process from initial review to completion typically takes six to twelve weeks, depending on the lender and the complexity of the case.

Key takeaways

Using a mortgage broker for debt consolidation is the most effective route for UK homeowners with complex finances, multiple debts, or imperfect credit histories, because brokers combine lender access, manual case presentation, and affordability expertise that no direct application can replicate.

| Point | Details |

|---|---|

| Broker access to lenders | Brokers reach specialist lenders unavailable directly, improving approval chances for complex cases. |

| No offer, no fee structure | Many brokers only charge on completion, aligning their incentive with your successful outcome. |

| Risk of secured borrowing | Consolidating into a mortgage puts your home at risk if repayments are not maintained. |

| Post-consolidation discipline | Closing credit accounts and budgeting strictly after completion prevents reaccumulating debt. |

| Process takes 6 to 12 weeks | From initial review to completion, expect a structured timeline managed by your broker. |

Paul’s view: why the broker difference is bigger than most people expect

Most people who come to us thinking about a debt consolidation remortgage have already tried the comparison websites. They have a number in their head from an online calculator, and they assume the broker process is just a formality to get that rate confirmed. In my experience, that assumption is wrong more often than it is right.

The cases where a broker makes the biggest difference are not the straightforward ones. They are the clients who have a missed payment from two years ago, or who are self-employed with variable income, or who have a debt-to-income ratio that an automated system flags immediately. Automated lender scoring often rejects borrowers with bruised credit or complex income, but a broker can manually present compensating factors to secure approvals. I have seen clients declined by two high-street lenders and then approved by a specialist lender the same week, simply because the case was presented properly.

The other thing I would say is that the affordability conversation matters as much as the rate. A broker who is doing their job properly will tell you if consolidation is not the right move for your situation. That honest assessment is worth more than any product comparison. If the numbers do not work long-term, the right answer is to say so and explore alternatives such as a debt management plan or a shorter-term personal loan instead.

My advice is simple. If your financial situation is straightforward and your credit is clean, a direct remortgage application might work. If there is any complexity at all, use a broker. The cost of getting it wrong is your home.

— Paul

How Prosperhomeloans can help with your debt consolidation mortgage

Prosperhomeloans is an independent mortgage and protection adviser with access to a wide lender panel, including specialist lenders who handle debt consolidation remortgages for clients with complex financial profiles. We operate on a no offer, no fee basis, which means you pay nothing unless your mortgage completes. Our process starts with a thorough affordability review, not a generic quote, so you understand exactly what consolidation means for your finances before you commit. If you are ready to simplify your debt repayments and want expert guidance at every stage, speak to our team to arrange a free mortgage consultation today.

FAQ

What is a debt consolidation remortgage?

A debt consolidation remortgage combines multiple unsecured debts such as credit cards, personal loans, and car finance into a single secured mortgage, reducing the number of monthly payments and potentially lowering the overall interest rate.

Why use a broker rather than applying directly to a lender?

Brokers access a wider range of lenders, including specialists unavailable directly, and can manually present your case to overcome automated rejections caused by complex income or credit history.

Does consolidating debt into a mortgage put my home at risk?

Yes. Because the new loan is secured against your property, failing to maintain repayments gives the lender the right to repossess your home. This is why affordability must be assessed carefully before proceeding.

How much does it cost to use a mortgage broker for consolidation?

Many independent brokers operate on a no offer, no fee basis, with typical transaction costs including legal fees ranging from £0 to £2,000, sometimes rolled into the new loan balance.

What should I do after my debt consolidation mortgage completes?

Close the credit accounts you have consolidated, build a strict monthly budget, and avoid taking on new unsecured debt. Consolidation is a financial reset that only works if spending habits change alongside it.