Why construction workers struggle with mortgages in the UK

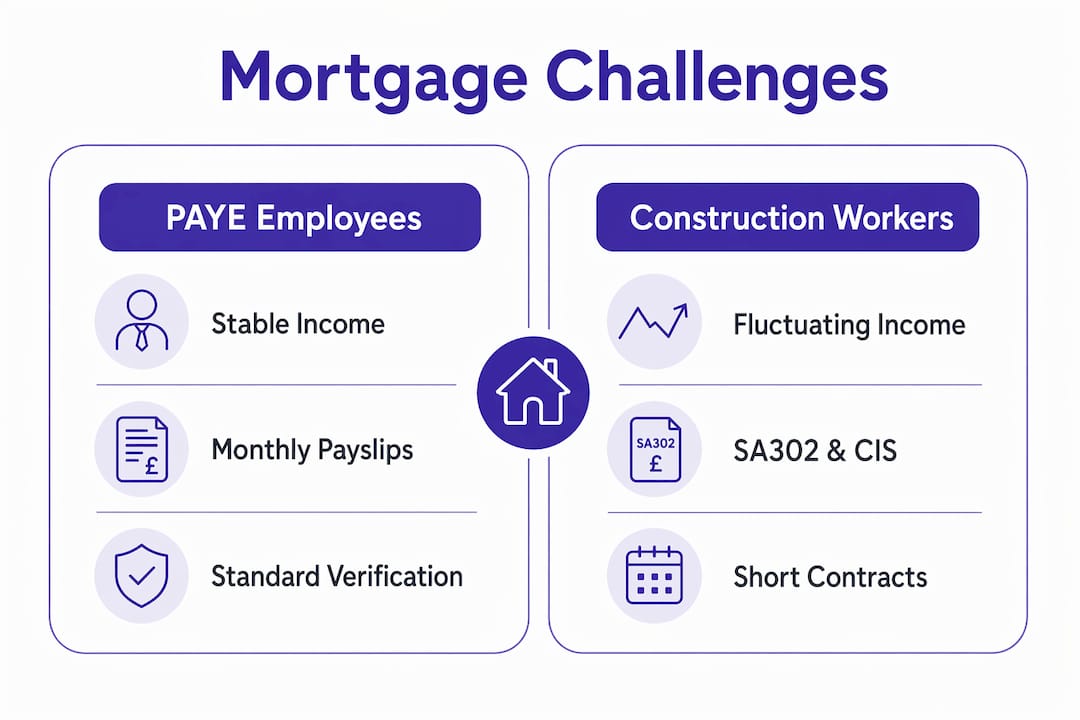

Construction workers are defined as one of the highest-risk borrower categories by mainstream UK lenders, not because they earn too little, but because their income does not fit the standard assessment model. The core problem is a mismatch: lenders are built around steady PAYE payslips, while construction work runs on short contracts, stage payments, and seasonal shifts. The Construction Industry Scheme (CIS), administered by HM Revenue & Customs, deducts tax at source and provides verifiable income records, yet many lenders still treat CIS workers with the same scepticism applied to unverified self-employment. Understanding why construction workers struggle with mortgages is the first step to doing something about it.

Why construction workers struggle with mortgages: the income mismatch

The root cause of construction jobs mortgage difficulties is structural. Mainstream lenders flag fluctuating income as unstable regardless of a worker’s actual earning capacity. That assessment is not based on what you earn. It is based on how predictably you earn it.

Construction work is paid in stages. A groundworker finishing a commercial foundation may receive a large payment in march, nothing in april, and then two smaller payments in may. To a lender’s automated system, that pattern looks unreliable. To the worker, it is a normal project cycle.

Short contracts compound the problem. A six-week contract on a housing development is standard in the industry, but a lender’s credit assessor may record it as a gap in employment. Short contract duration and gaps between jobs are routine in construction, yet they are viewed negatively by most high-street lenders.

Seasonal slowdowns add another layer. Groundwork and external trades slow in winter. A plasterer or roofer earning well from april through october may show reduced income in january and february. Averaged over a full year, the figure looks lower than the worker’s true earning power during active months.

The common barriers to mortgage approval for construction workers include:

- Irregular monthly income that does not match standard affordability calculators

- Short or rolling contracts recorded as employment gaps

- Stage payments misread as inconsistent earnings

- Seasonal income dips that pull down annual averages

- Multiple income sources across different sites or contractors

Pro Tip: Keep a running log of every contract, start date, end date, and payment received. A clear paper trail of continuous work, even across multiple employers, tells a far stronger story than payslips alone.

Why does CIS income cause problems with lenders?

The Construction Industry Scheme is a tax mechanism, not a sign of financial instability. Under CIS, the contractor deducts tax and National Insurance at source before paying the subcontractor. CIS tax is deducted at source as an advance payment to HMRC, which means income is verified and traceable. That should make CIS workers easier to assess, not harder.

The problem lies in how lenders interpret the documentation. Most high-street lenders request SA302 forms, which are HMRC’s summary of self-assessment tax returns. SA302s average income across the tax year. If your earnings rose sharply in the second half of the year, the SA302 average understates your current earning power. SA302 averages obscure current earning power for workers whose income is growing or changing.

Lenders also require trading history. Two years of trading history is the standard requirement for self-employed borrowers, even when a CIS worker has a current contract and a consistent recent income. A worker who moved from PAYE employment to CIS subcontracting 18 months ago may be turned down simply because the clock has not run long enough, despite earning more now than ever before.

The table below shows how CIS income is treated differently from PAYE income in a typical lender assessment:

| Factor | PAYE employee | CIS subcontractor |

|---|---|---|

| Income verification | Monthly payslips | SA302 and tax year overview |

| Assessment method | Last 3 months’ payslips | 2-year average |

| Employment gaps | Rarely flagged | Often flagged |

| Trading history required | Not applicable | Typically 2 years |

| Automated system recognition | High | Low to moderate |

Pro Tip: Ask your accountant to produce a current year income projection alongside your SA302. Some specialist lenders will accept this as supporting evidence of your actual earning trajectory.

Which lender policies make home financing harder for construction workers?

Lender policies are built around a PAYE benchmark. Permanent, salaried employment is the reference point against which all other income types are measured. Construction workers, whether operating under CIS, through an umbrella company, or via an agency, fall outside that benchmark in ways that trigger caution.

Automated underwriting systems are a particular obstacle. Umbrella company arrangements may not produce traditional payslips, which confuses automated systems that expect a standard payslip format. The system cannot categorise the income cleanly, so it flags the application for manual review or declines it outright.

Affordability checks rely on averages and historical data. If your income rose significantly in the past year, the lender’s model may still use a lower figure drawn from older records. The result is that your assessed borrowing capacity is lower than your real financial position justifies.

The policies that most commonly affect construction workers include:

- Minimum trading history rules that exclude workers with fewer than two years of CIS or self-employment records

- Payslip-only income verification that cannot accommodate stage payments or CIS vouchers

- Automated affordability calculators that average income across 24 months, penalising recent growth

- Employment gap policies that flag short contracts as breaks in work rather than normal project cycles

- Umbrella company income treated as neither fully employed nor fully self-employed, creating classification confusion

Flexible workers feel economic pressure first, particularly during periods of hiring freezes or cost controls. That economic context makes lenders even more cautious about contract-based income, even when long-term demand for construction skills remains strong.

What practical steps improve mortgage approval odds for construction workers?

The most effective step is working with a mortgage broker who specialises in CIS and construction worker applications. A specialist broker knows which lenders accept CIS vouchers as income proof, which will consider day rates rather than SA302 averages, and which have manual underwriting processes that allow a fuller picture of your finances.

-

Find a CIS-specialist broker. Not every broker understands construction income. A specialist will match you to lenders whose criteria fit your actual situation, saving time and protecting your credit file from unnecessary declined applications.

-

Use income flex products. Income flex products accept day rates without requiring SA302 averages, which is a significant advantage for workers whose recent contracts reflect higher earnings than their tax return average shows.

-

Prepare thorough documentation. Gather CIS payment statements, contracts (current and recent), bank statements covering 12 months, and a tax year overview from HMRC. The more clearly you can evidence continuous work and consistent income, the stronger your application.

-

Address gaps proactively. If you had a period between contracts, write a brief explanation. Lenders respond better to a clear account of a planned gap than to silence that leaves them to draw their own conclusions.

-

Consider specialist lenders. Some lenders have built products specifically for self-employed and contract workers, with criteria that reflect how construction income actually works rather than how a salaried employee’s income works.

-

Check your credit file before applying. Declined applications leave a mark. Review your credit report through Experian, Equifax, or TransUnion before submitting anything, and resolve any errors or outstanding issues first.

Mortgage applications fail largely due to insufficient documentation and perceived income instability rather than actual affordability problems. That is a solvable problem with the right preparation.

Key takeaways

Construction workers face mortgage difficulties because lender systems are designed for PAYE income, not the contract-based, stage-paid earnings typical of the construction industry.

| Point | Details |

|---|---|

| Income mismatch is the core issue | Lenders assess construction income as unstable even when earnings are consistent and verifiable. |

| CIS income is misunderstood | Tax deducted at source proves income authenticity, but SA302 averages often understate current earning power. |

| Automated systems create barriers | Umbrella and agency arrangements confuse standard underwriting tools, causing delays or refusals. |

| Specialist brokers make a difference | A CIS-specialist broker matches you to lenders whose criteria reflect how construction income actually works. |

| Documentation is your strongest asset | CIS vouchers, contracts, and 12 months of bank statements build a credible case where payslips cannot. |

What I’ve learnt from helping construction workers get mortgages

The most persistent myth I encounter is that construction workers simply cannot get mortgages. That is not true. What is true is that the wrong lender, approached without preparation, will say no. The right lender, approached with the right documentation and the right broker, will often say yes.

What surprises many workers is how much the choice of broker matters. A generalist broker may not know that certain lenders will accept 12 months of CIS payment statements in place of two years of SA302s. That single piece of knowledge can be the difference between approval and rejection.

I also see workers underestimate the value of their own records. Your CIS vouchers, your contracts, your bank statements: these are evidence of a real, working income. They tell a story that a payslip cannot. The problem is that most lenders are not set up to read that story. Specialist lenders are, and that is where the opportunity lies.

Preparation matters more than most workers realise. Spending two or three months organising documentation, clearing any credit issues, and understanding what a lender will ask for puts you in a far stronger position than applying cold and hoping for the best.

— Paul

How Prosperhomeloans helps construction workers secure a mortgage

Prosperhomeloans specialises in mortgage advice for construction workers and self-employed applicants across the UK. We understand CIS income, day rate assessments, and the documentation that specialist lenders actually need.

Whether you work under CIS, through an umbrella company, or on rolling contracts, we match you to lenders whose criteria reflect your real financial position. Our advisors take the time to understand your income pattern before recommending any product. Visit Prosperhomeloans to speak with an advisor who knows the construction mortgage market and can guide you through the process with clarity and confidence.

FAQ

Why do construction workers get refused mortgages?

Construction workers are refused mortgages primarily because their income is irregular and does not fit standard lender assessment models. Perceived income instability and insufficient documentation are the leading causes of refusal, not actual unaffordability.

Can CIS workers get a mortgage in the UK?

Yes, CIS workers can get a mortgage. Specialist lenders and brokers with CIS expertise can assess CIS payment statements and day rates rather than relying solely on SA302 averages.

How many years of accounts do construction workers need for a mortgage?

Most high-street lenders require two years of self-employment or CIS trading history. Specialist lenders may accept 12 months of records alongside a current contract as sufficient evidence.

Does working through an umbrella company affect my mortgage application?

Working through an umbrella company can complicate income verification because automated underwriting systems may not recognise the payslip format. A specialist broker can identify lenders whose manual underwriting processes handle umbrella income correctly.

What documents do construction workers need for a mortgage?

The strongest applications include CIS payment statements, a current contract, 12 months of bank statements, an SA302 and tax year overview from HMRC, and a brief explanation of any gaps between contracts.