What is a remortgage for debt? UK guide 2026

A remortgage for debt consolidation is defined as replacing your existing mortgage with a larger one and using the additional funds to clear unsecured debts such as credit cards and personal loans. This approach centralises multiple repayments into a single monthly mortgage payment, often at a lower interest rate. The appeal is real, but so are the risks. This guide explains exactly how the process works, what it costs, and whether it suits your situation as a UK homeowner in 2026.

What is a remortgage for debt consolidation?

Remortgaging to pay off debt means borrowing more than you currently owe on your mortgage and directing that extra money to settle outstanding unsecured debts. The industry term for this is a debt consolidation remortgage. It is not a new product. It is simply a larger mortgage that absorbs debts you previously held separately.

Consider a practical example. If your property is worth £280,000 and your current mortgage balance is £160,000, a lender may allow you to remortgage up to £190,000. The extra £30,000 clears your credit card balances or personal loans. You then repay everything through one monthly mortgage payment rather than several separate bills.

The key distinction is that unsecured debts become secured against your home. That shift in risk is the central fact every homeowner must understand before proceeding.

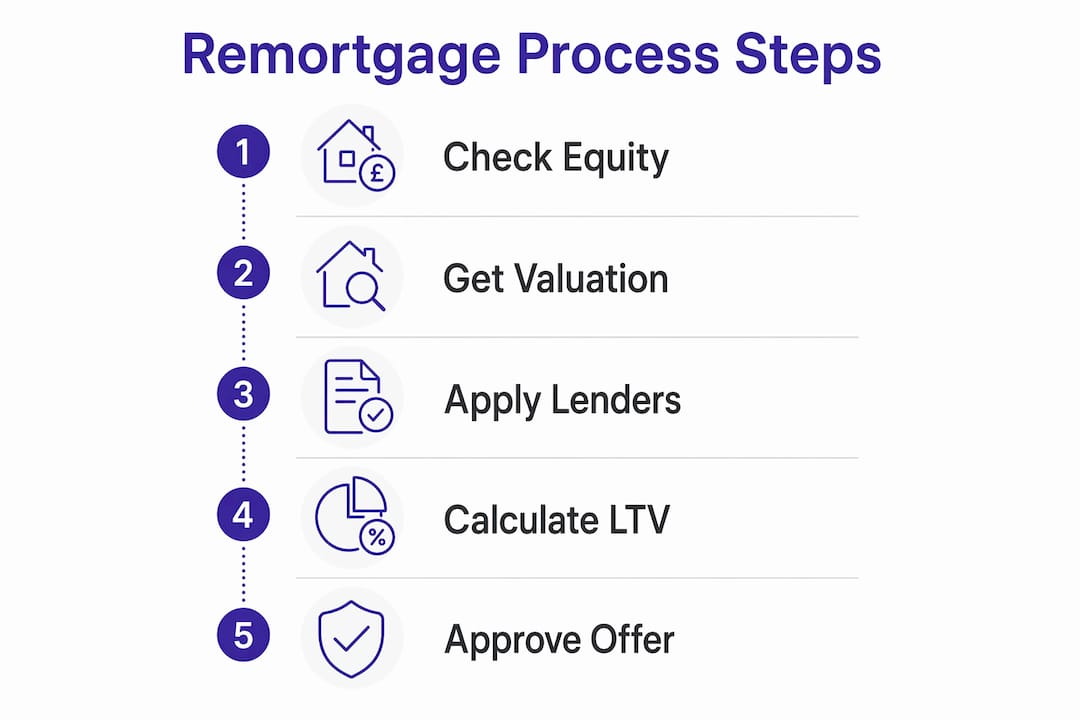

How does remortgaging for debt consolidation work?

The process follows a clear sequence. Understanding each stage helps you prepare and avoid surprises.

- Property valuation. Your lender commissions a valuation to confirm your home’s current market value. This determines how much equity you hold and how much you can borrow.

- Application and affordability assessment. You apply for the new, larger mortgage. Lenders stress-test repayments at higher interest rates to confirm you can still afford payments if rates rise.

- Offer and legal process. A solicitor handles the legal transfer, repays your existing mortgage, and releases the additional funds to clear your nominated debts.

- Completion. Your old mortgage closes. Your new, larger mortgage begins. Your unsecured debts are cleared.

Loan-to-value limits explained

Most lenders require a loan-to-value (LTV) ratio of no more than 85%–90% after consolidation. On a £250,000 property, that means your total mortgage cannot exceed £212,500–£225,000. The table below illustrates how this works in practice.

| Property Value | Maximum LTV (85%) | Maximum LTV (90%) | Existing Mortgage | Maximum Extra Borrowing |

|---|---|---|---|---|

| £200,000 | £170,000 | £180,000 | £130,000 | £40,000–£50,000 |

| £280,000 | £238,000 | £252,000 | £160,000 | £78,000–£92,000 |

| £350,000 | £297,500 | £315,000 | £220,000 | £77,500–£95,000 |

Pro Tip: Request an up-to-date valuation before approaching lenders. Online estimates can differ significantly from a formal survey, and your borrowing limit depends entirely on the confirmed figure.

What are the benefits and risks of using a remortgage to clear debt?

A debt consolidation remortgage offers genuine advantages, but it carries risks that are often underestimated. A balanced view is the only responsible starting point.

The benefits

- Lower interest rate. Mortgage rates are typically lower than credit card or personal loan rates, which can reduce your monthly outgoings.

- Simplified finances. One payment replaces several. That clarity alone reduces the chance of missed payments.

- Improved cash flow. Lower monthly costs free up income for savings or other priorities.

- Alternative to insolvency. For homeowners with equity, remortgaging avoids the credit damage caused by formal insolvency options such as an Individual Voluntary Arrangement (IVA) or bankruptcy.

The risks

- Your home is now at risk. Unsecured debts become secured against your property. If you fall behind on payments, your lender can repossess your home.

- Total debt does not shrink. Remortgaging does not reduce the amount you owe. It restructures it over a longer term, which can increase the total interest you pay over the life of the loan.

- Extended repayment term. Spreading debt over 20 or 25 years means paying far more in interest than you would clearing a credit card in two or three years.

“A key misconception is that remortgaging for debt consolidation automatically improves financial stability. Instead, it transfers risk to the home, requiring rigorous affordability checks.” — JMW Solicitors

Pro Tip: Before committing, calculate the total interest you will pay over the full mortgage term on the consolidated amount. Compare that figure with the total interest on your current debts at their existing rates. The monthly saving may look attractive, but the lifetime cost can tell a very different story.

Remortgage vs personal loan: which suits you better?

Remortgaging is not the only route to debt consolidation. Understanding where it sits among the alternatives helps you choose the right path.

| Method | Requires Home Equity | Credit Score Impact | Debt Written Off | Typical Cost |

|---|---|---|---|---|

| Debt consolidation remortgage | Yes | Minimal if managed well | No | Arrangement and legal fees |

| Personal loan | No | Moderate | No | Higher interest rate |

| Debt Management Plan | No | Moderate | Partial | Agency fees may apply |

| IVA | No | Severe, lasts 6 years | Yes (partial) | Insolvency practitioner fees |

| Bankruptcy | No | Severe, lasts 6 years | Yes (most debts) | Court fees |

Remortgaging suits homeowners who have meaningful equity, a stable income, and the discipline to avoid accumulating new unsecured debt after consolidation. A personal loan suits those with smaller debts, no equity, or who want to avoid securing borrowing against their property. For a broader perspective on how mortgage refinancing compares across different markets, the underlying principles of cost and risk transfer remain consistent.

Formal insolvency options such as an IVA or bankruptcy write off a portion of debt but leave a lasting mark on your credit file. Remortgaging restructures debt without write-off, preserving your credit profile if you maintain payments.

What practical steps should you take before remortgaging for debt?

Preparation separates a sound decision from a costly mistake. Follow these steps before approaching any lender.

- Calculate your available equity. Subtract your current mortgage balance from your property’s market value. That figure is your equity. Lenders will only release a portion of it.

- Work out the break-even point. Upfront costs include arrangement fees of £500–£2,000 and legal fees. Divide the total upfront cost by your projected monthly saving to find how many months before you are in profit.

- Assess the mortgage term carefully. Remortgaging resets the mortgage term clock. Extending back to 25 or 30 years lowers monthly payments but raises total interest paid significantly. Consider keeping the term as short as your budget allows.

- Compare fixed and variable rates. A fixed rate gives payment certainty for two to five years. A variable rate may start lower but exposes you to rate rises. Given current market conditions, most advisers recommend fixing for stability.

- Check for early repayment charges. Your existing mortgage may carry a penalty for leaving before the fixed term ends. Factor this into your total cost calculation.

- Seek professional advice. An independent mortgage adviser reviews your full financial picture and accesses deals not available directly to consumers.

Pro Tip: Always understand the total cost over the full mortgage term, not just the monthly saving. A £200 monthly reduction sounds compelling until you realise it costs £15,000 more in total interest over 20 years.

What eligibility criteria do UK lenders apply?

Lenders assess several factors before approving a debt consolidation remortgage. Meeting these criteria is not optional. Falling short on any one of them can result in a declined application.

- Sufficient equity. You need enough equity to borrow the additional amount while staying within the lender’s LTV limit, typically 85%–90%.

- Acceptable credit score. A poor credit history signals risk to lenders. Some specialist lenders accept adverse credit, but at higher rates.

- Stable, provable income. Lenders require payslips, tax returns, or SA302 forms for self-employed applicants. Income must comfortably cover the new, larger repayment.

- Affordability stress test. Lenders test whether you can afford repayments if interest rates rise above current levels. Passing this test is mandatory.

- Clean payment history on your current mortgage. Missed mortgage payments in the past 12 months make approval significantly harder.

- Reason for borrowing. Lenders ask why you are increasing borrowing. Debt consolidation is an accepted reason, but lenders scrutinise the amounts and types of debt involved.

If you are already in financial distress, some lenders will decline on the basis that the additional borrowing increases rather than reduces your risk profile. In those cases, speaking to a debt charity such as StepChange before approaching lenders is a sensible first step.

Key takeaways

A debt consolidation remortgage restructures what you owe rather than reducing it, making financial discipline and a clear understanding of total costs the deciding factors in whether it works for you.

| Point | Details |

|---|---|

| Core definition | A remortgage for debt replaces your mortgage with a larger one to clear unsecured debts. |

| LTV limits apply | Most lenders cap borrowing at 85%–90% of your property’s value after consolidation. |

| Risk shifts to your home | Unsecured debts become secured, meaning missed payments can lead to repossession. |

| Total cost matters most | Monthly savings can be misleading if a longer term increases lifetime interest significantly. |

| Professional advice is critical | An independent adviser accesses more deals and assesses your full financial position accurately. |

The uncomfortable truth about debt consolidation remortgages

I have worked with many homeowners who arrive at a debt consolidation remortgage with genuine relief in their eyes. The monthly saving is real. The simplicity is real. But the relief sometimes masks a pattern that the remortgage alone cannot fix.

The most common mistake I see is treating the remortgage as the finish line rather than the starting point. Credit cards are cleared, the monthly payment drops, and within 18 months those same cards carry new balances. The homeowner now has both a larger mortgage and fresh unsecured debt. That outcome is worse than where they started.

Remortgaging requires strong financial discipline because it secures previously unsecured debts against your home. The stakes are categorically higher. I always encourage clients to pair a consolidation remortgage with a clear budget and, where appropriate, a conversation with a financial counsellor about spending habits.

The other thing most articles gloss over is the solicitor’s role. Legal fees are not just a line item. A good solicitor ensures the funds are directed correctly and that you fully understand what you are signing. JMW Solicitors and similar specialist firms add real value here, particularly for complex cases involving multiple creditors.

My honest position is this: a debt consolidation remortgage is a legitimate and often sensible tool for the right homeowner. It is not a shortcut. Used with clear eyes and professional guidance, it can genuinely improve your financial position. Used without discipline, it compounds the problem.

— Paul

How Prosperhomeloans can help you remortgage for debt

Remortgaging for debt consolidation involves more moving parts than a standard remortgage. Getting the numbers right, choosing the correct product, and understanding the long-term implications requires expert guidance.

Prosperhomeloans is an independent mortgage and protection adviser with direct access to a wide range of lenders, including those who specialise in debt consolidation cases. We assess your equity, income, and credit position to identify the most suitable deal for your circumstances. We handle the paperwork, liaise with solicitors, and keep the process straightforward from start to finish. If you are considering a debt consolidation remortgage, speak with our team today and get clear, honest advice with no obligation.

FAQ

What is a remortgage for debt in simple terms?

A remortgage for debt is when you replace your existing mortgage with a larger one and use the extra money to pay off unsecured debts such as credit cards or personal loans. It consolidates multiple debts into a single monthly mortgage payment.

Can i remortgage for debt if i have bad credit?

Some specialist lenders accept applications from homeowners with adverse credit, but rates will be higher and LTV limits tighter. Speaking to an independent adviser gives you the clearest picture of which lenders are likely to approve your application.

Does remortgaging for debt reduce what i owe?

No. Remortgaging does not reduce the total amount owed. It restructures the debt over a longer term, which may lower monthly payments but can increase the total interest paid over time.

How much equity do i need to remortgage for debt consolidation?

You need enough equity to borrow the additional amount while keeping your LTV at or below 85%–90%. On a £250,000 property, your total mortgage after consolidation should not exceed £212,500–£225,000.

What are the main risks of a debt consolidation remortgage?

The primary risk is that your unsecured debts become secured against your home. If you miss payments, your lender can repossess your property. Extending the mortgage term also increases the total interest you pay over the life of the loan.