What is a mortgage in principle? UK buyer's guide

A mortgage in principle (MIP) is a lender’s preliminary estimate of how much they may be willing to lend you, based on a brief review of your income, outgoings, and credit profile. Also known as an agreement in principle (AIP) or decision in principle (DIP), the terminology varies across lenders such as HSBC, Nationwide, and NatWest, but the concept is identical. It is not a guaranteed mortgage offer. It is a conditional, non-binding signal that tells you, and the sellers you approach, that a lender considers you a credible borrower. For any UK homebuyer, understanding what an MIP is and how to use it effectively is one of the most practical steps you can take before you begin viewing properties.

What is a mortgage in principle and how does it work?

A mortgage in principle is an early-stage borrowing estimate that improves buyer credibility without committing either party to a formal agreement. Lenders issue it after reviewing basic financial information, and it gives you a working figure to take into property searches and negotiations.

The process is straightforward. You provide a lender or mortgage broker with details about your income, regular outgoings, employment status, and any existing debts. The lender then runs a credit check and produces a figure indicating the maximum they would likely lend under current conditions.

Soft checks vs hard checks

One of the most consequential decisions at this stage is whether the lender uses a soft or hard credit check. Soft credit checks do not affect your credit score, whereas hard checks leave a visible mark on your credit file. If you apply for multiple MIPs in a short period and each triggers a hard check, your credit score can dip temporarily. Always ask the lender which type of check they use before you proceed.

The documents and information typically required at MIP stage include:

- Proof of income: payslips, P60, or self-assessment tax returns for the self-employed

- Bank statements covering the last three to six months

- Details of any outstanding loans, credit cards, or financial commitments

- Proof of identity and address

MIPs typically last between 30 and 90 days, depending on the lender. If your property search extends beyond that window, you will need to reapply. This is worth planning for, particularly in competitive markets where searches can run for several months.

Pro Tip: Ask your lender or broker upfront whether their MIP application uses a soft or hard credit check. If it is a hard check, limit your applications to one or two lenders to protect your credit score during the search period.

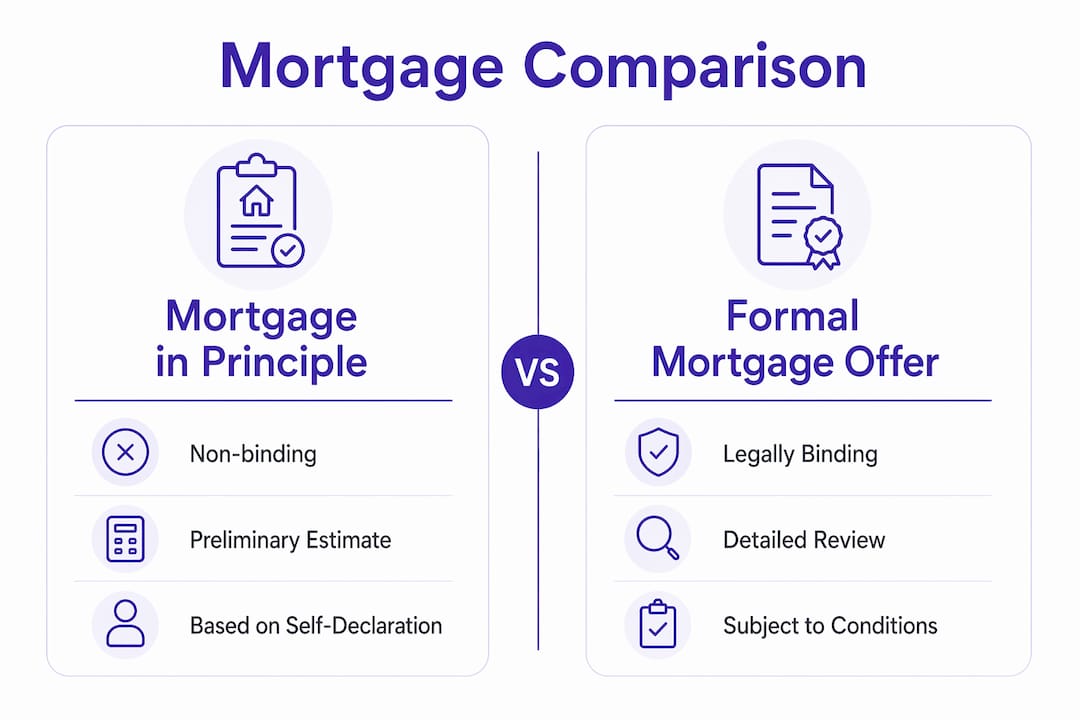

What is the difference between a mortgage in principle and a formal mortgage offer?

The distinction between an MIP and a formal mortgage offer is one of the most misunderstood points in the UK homebuying process. Treating them as equivalent is a key reason property purchases fall through.

An MIP is provisional. It is based on the information you self-declare and a preliminary credit review. The lender has not verified your documents, assessed the property, or committed to lending you anything. A formal mortgage offer, by contrast, is issued only after a full mortgage application with detailed underwriting, a hard credit check, and a property valuation. Once issued subject to its stated conditions, a mortgage offer represents a legally binding commitment from the lender.

The table below sets out the key differences clearly.

| Feature | Mortgage in principle | Formal mortgage offer |

|---|---|---|

| Binding on lender | No | Yes, subject to conditions |

| Credit check type | Usually soft | Always hard |

| Property valuation required | No | Yes |

| Document verification | Minimal | Full underwriting |

| Required for contract exchange | No | Yes |

| Typical validity | 30 to 90 days | Three to six months |

Solicitors will not proceed to exchange contracts without a valid formal mortgage offer in place. This is a legal requirement, not a preference. An MIP, however convincing it looks on paper, carries no weight at the exchange stage.

Understanding mortgage deal comparisons between MIP and mortgage offer stages can also help you identify which lender is likely to offer the most favourable terms before you commit to a full application.

Pro Tip: Once your offer on a property is accepted, move quickly to convert your MIP into a full mortgage application. Delays at this stage can cause your MIP to expire, which may require a new credit check and could slow down your solicitor’s timeline.

What are the practical benefits and limitations of a mortgage in principle?

An MIP serves a clear and practical purpose in the homebuying process, but it has firm limits that every buyer should understand before relying on it.

Benefits worth knowing

An MIP strengthens your credibility with estate agents and sellers. In a competitive market, sellers and their agents routinely favour buyers who can demonstrate financial readiness. Presenting an MIP signals that you have already engaged with a lender and are not simply browsing. This can meaningfully improve your chances of having an offer accepted, particularly when competing against buyers without one.

Beyond negotiating position, an MIP gives you a realistic budget ceiling before you fall in love with a property you cannot afford. This saves time for everyone involved and focuses your search on properties within genuine reach.

The key benefits are:

- Clearer understanding of your borrowing capacity before you begin viewing

- Stronger negotiating position with sellers and estate agents

- Faster progression to a full mortgage application once an offer is accepted

- Useful signal to yourself about whether your finances are in good order

Limitations to keep in mind

The limitations are equally important. An MIP is not a guarantee. Lenders can withdraw it if your circumstances change, if the property valuation comes back lower than expected, or if the full underwriting process reveals information that was not apparent at the MIP stage. A change in employment, a new credit commitment, or a significant drop in income between MIP and full application can all result in a revised or declined offer.

Multiple MIP applications with hard credit checks can also temporarily lower your credit score, which is counterproductive when you are about to apply for one of the largest financial products available. Time your MIP request carefully. Apply when you are genuinely ready to begin viewing and making offers, not months in advance.

How does a mortgage in principle affect foreign nationals in the UK?

Foreign nationals and skilled worker visa holders face more stringent lending criteria when applying for a mortgage in the UK. Understanding how an MIP fits into this process is particularly relevant for this group.

Visa holders typically face stricter requirements but can secure mortgages with the correct documentation and a sufficient deposit. Many lenders require a larger deposit from foreign nationals, often 25% or more, compared to the standard 5% to 10% for UK nationals. Stable employment evidence and a clear immigration status are central to any application.

An MIP can be especially valuable for foreign nationals precisely because it helps demonstrate financial readiness to sellers who may be uncertain about a buyer’s circumstances. Obtaining an MIP early in the process signals seriousness and gives the buyer a clearer picture of what lenders are likely to offer given their specific situation.

Key considerations for foreign nationals seeking an MIP include:

- Visa type and remaining duration: most lenders require at least two to three years remaining on a visa at the point of application

- Deposit size: a larger deposit reduces lender risk and improves the likelihood of a positive MIP outcome

- Employment history in the UK: lenders generally prefer at least one year of UK-based employment

- Credit history: foreign nationals with limited UK credit history may need to build this before applying

- Documentation: passport, visa, proof of address, payslips, and bank statements are typically required

Not all high street lenders will consider applications from foreign nationals. Specialist lenders and independent brokers with experience in this area are often better placed to find suitable options. This is where working with an adviser who understands the nuances of what is mortgage in principle for foreign nationals can make a significant difference to the outcome.

Key takeaways

A mortgage in principle is a conditional, non-binding estimate from a lender that strengthens your buying position but must be converted into a full mortgage offer before contracts can be exchanged.

| Point | Details |

|---|---|

| MIP is not a guarantee | Lenders can withdraw an MIP if circumstances change before the full application. |

| Soft vs hard credit checks | Always confirm which check type applies to protect your credit score during the search. |

| MIP validity window | Most MIPs last 30 to 90 days, so time your application to match your search timeline. |

| Foreign nationals face stricter criteria | Larger deposits and clear visa status are typically required to obtain an MIP. |

| Mortgage offer is legally binding | Only a formal mortgage offer, not an MIP, satisfies solicitors at the exchange stage. |

Why I think most buyers misuse their mortgage in principle

In my experience working with buyers across a range of circumstances, the mortgage in principle is consistently either underused or misunderstood. Buyers either skip it entirely because they assume it is unnecessary at the early stages, or they treat it as the finish line when it is really just the starting block.

The most common mistake I see is buyers who secure an MIP, find a property they love, and then delay converting to a full application. By the time they move, their MIP has expired, their circumstances have shifted slightly, or the lender’s criteria have changed. That delay can cost them the property entirely.

What I would encourage every buyer to do is treat the MIP as a budgeting and negotiation tool, not a mortgage. Use it to set your ceiling, sharpen your search, and signal credibility to sellers. Then, the moment your offer is accepted, treat the full application as urgent. Do not wait.

For foreign nationals in particular, I would strongly recommend working with a specialist broker before even approaching a lender for an MIP. The criteria vary significantly between lenders, and a poorly timed hard credit check from an unsuitable lender can do real damage to an already complex application.

The MIP is one of the most useful tools in the homebuying process when used correctly. The key is knowing what it is, what it is not, and how to time it well within your wider mortgage strategy.

— Paul

How Prosperhomeloans can help you get started

At Prosperhomeloans, we work with first-time buyers, home movers, and foreign nationals to make the mortgage process straightforward from the very first step. Whether you need guidance on obtaining an MIP, understanding your borrowing capacity, or progressing to a full mortgage application, our independent advisers are here to support you at every stage.

We take the time to understand your individual circumstances, whether you are a UK national with a straightforward application or a skilled worker visa holder navigating more complex lending criteria. Our role is to find the right lender and the right deal for your situation, saving you time and reducing the stress that so often accompanies the mortgage process. Get in touch with the team at Prosperhomeloans to discuss your options and take the first step with confidence.

FAQ

What does a mortgage in principle actually confirm?

A mortgage in principle confirms that a lender is willing, in principle, to lend you a specific amount based on your preliminary financial information. It is not a guarantee and is subject to full verification during a formal application.

How long does a mortgage in principle last?

Most MIPs remain valid for 30 to 90 days from the date of issue. If your property search continues beyond this period, you will need to reapply, which may involve another credit check.

Does getting a mortgage in principle affect my credit score?

It depends on whether the lender uses a soft or hard credit check. Soft checks have no impact on your credit score, while hard checks leave a visible mark that can temporarily reduce your score if repeated frequently.

Can foreign nationals get a mortgage in principle in the UK?

Yes, foreign nationals and skilled worker visa holders can obtain an MIP, though lenders typically require a larger deposit and clear evidence of stable UK employment and immigration status. Working with a specialist broker significantly improves the chances of a successful outcome.

Is a mortgage in principle the same as a mortgage offer?

No. An MIP is a provisional, non-binding estimate, while a formal mortgage offer is a legally binding commitment issued after full underwriting, a hard credit check, and a property valuation. Solicitors require a mortgage offer before contracts can be exchanged.