What is a large loan mortgage? Your 2026 guide

A large loan mortgage is defined as a mortgage where the amount borrowed significantly exceeds standard residential loan values, typically starting from £500,000 and most commonly associated with loans above £1 million. These are not simply scaled-up versions of ordinary mortgages. They involve specialist underwriting, stricter lending criteria, and often a choice between high-street lenders and private banks. If you are considering purchasing a high-value property or financing a major project, understanding how large loan mortgages work is the first step to approaching lenders with confidence. Prosperhomeloans works with borrowers at this level every day, and the differences from standard lending are significant.

What is a large loan mortgage and what qualifies?

A large loan mortgage is typically defined as a loan exceeding £1 million, though many lenders treat loans from £500,000 upwards as large. That threshold matters because it determines which lending rules, affordability models, and underwriting processes apply to your application.

Lenders assess large mortgages using a combination of loan-to-income (LTI) multiples and loan-to-value (LTV) ratios. High-street lenders use income multiples of up to 5.5 times combined income for eligible professionals. That means a couple with a combined gross income of £200,000 could, in theory, borrow up to £1.1 million through a high-street product. LTV caps on large loans are generally tighter than on standard mortgages, with many lenders limiting borrowing to 75%–85% of the property value.

The income types lenders accept also differ at this level. Salary alone is rarely the whole picture. Lenders at the large loan tier routinely consider:

- Basic salary and guaranteed contractual bonuses

- Self-employment income verified through two to three years of accounts or tax returns

- Rental income from investment properties

- Investment dividends and share-based remuneration

- Pension income for older borrowers

Compliance with affordability models and LTI caps applies to all lenders, but the degree of discretion increases considerably with client complexity and asset profile. A borrower with a straightforward salary may find a high-street route sufficient. A borrower with a mix of income sources, foreign assets, or a complex financial profile will almost certainly need a private bank or specialist lender.

Pro Tip: Professionals such as doctors, lawyers, and engineers may qualify for enhanced income multiples of up to 5.5 times their income on certain high-street large loan products. Always confirm your professional status upfront when applying.

How does underwriting differ for large mortgage loans?

High-value borrowing requires more than scaling a standard mortgage. Once a loan exceeds £1 million, manual risk-oriented underwriting becomes the norm rather than the exception. A computer-generated decision is rarely sufficient at this level.

The underwriting process for a large loan mortgage typically follows these stages:

- Income verification. Lenders examine every income stream in detail. Bonuses must be evidenced over multiple years. Dividends require company accounts. Salary from overseas employers triggers additional scrutiny.

- Asset assessment. Private banks in particular assess your total balance sheet, not just your income. Liquid assets, investment portfolios, and property holdings all contribute to the lender’s view of your risk profile.

- Currency risk review. If part of your income arrives in a foreign currency, mainstream lenders apply a discount, known as a haircut, before including it in affordability calculations. Foreign currency income such as USD, EUR, CHF, or AED is accepted by some lenders but at a reduced rate to account for exchange rate fluctuation.

- Exit strategy review. For interest-only or part-and-part loans, lenders require a credible, documented plan for repaying the capital. This is not optional at the large loan level.

- Stress testing. Lenders model your ability to service the debt if interest rates rise, your income drops, or asset values fall.

Pro Tip: Prepare a clear written summary of your income sources, assets, and intended repayment strategy before approaching any lender. Underwriters at this level respond well to borrowers who present their financial position clearly and completely.

Private banks apply discretionary, risk-based underwriting that incorporates total income, assets, and exit strategies, offering considerably more flexibility than policy-led high-street models. That flexibility comes with a relationship requirement. Private banks typically expect you to hold or move assets under management with them as part of the arrangement. Understanding the terms and conditions of any lending arrangement is critical at this level, and reviewing guidance on lending risk management before committing helps you ask the right questions.

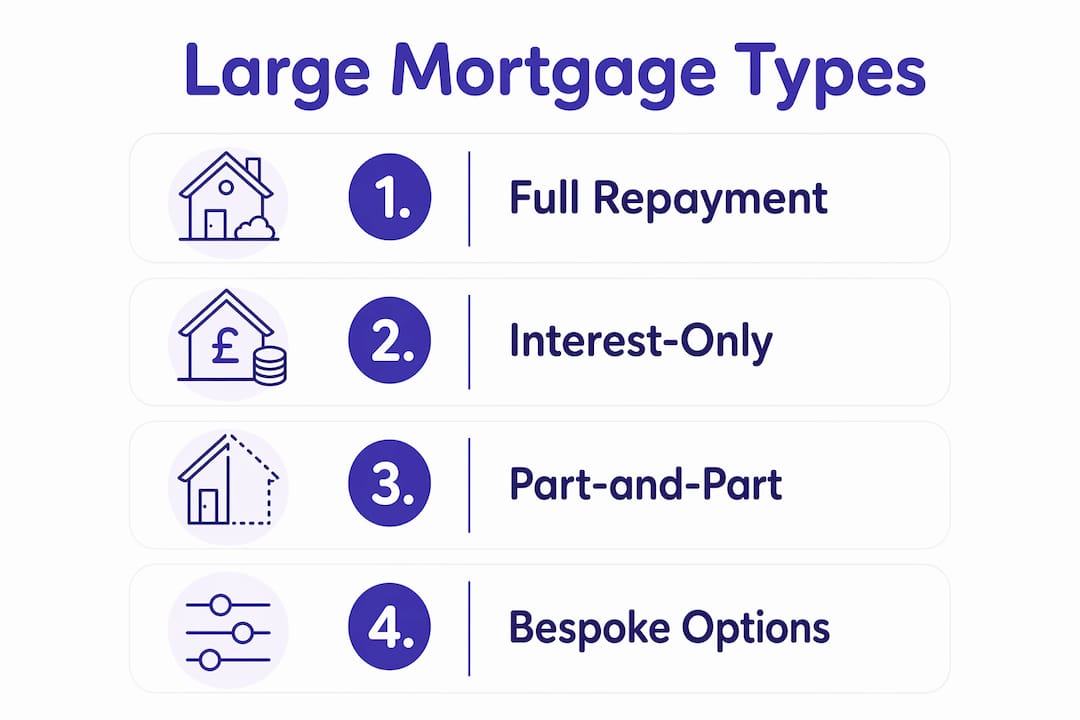

What types of large mortgages are available?

The large mortgage definition covers several distinct repayment structures. Choosing the right one affects your monthly outgoings, your tax position, and your long-term financial plan.

| Mortgage type | How it works | Best suited to |

|---|---|---|

| Full repayment | Monthly payments cover both interest and capital | Borrowers who want certainty and full ownership at term end |

| Interest-only | Monthly payments cover interest only; capital repaid separately | High-income borrowers with a clear exit strategy |

| Part-and-part | A blend of repayment and interest-only on the same loan | Borrowers who want lower monthly costs with some capital reduction |

| Bespoke private bank | Fully tailored structure, potentially in multiple currencies | High net worth clients with complex international finances |

Interest-only is the structure most commonly associated with high-value mortgages, but it carries the strictest requirements. Pure interest-only large mortgages face tighter LTV limits and require documented evidence of a credible repayment plan. Accepted exit strategies include property sale, bonus income, pension lump sums, investment portfolios, or cash reserves. Lenders will not accept vague assurances. Each strategy must be evidenced and realistic.

Part-and-part mortgages offer a practical middle ground. You repay a portion of the capital each month while keeping payments lower than a full repayment mortgage. This suits borrowers who want to reduce their outstanding balance gradually without committing to full repayment costs from day one.

Private banks offer bespoke options that go beyond what high-street products allow. These can include loans structured across multiple currencies, phased repayment schedules tied to expected income events such as a business sale or bonus cycle, and interest-only terms extending beyond standard limits. The trade-off is that private bank relationships require a higher level of financial disclosure and often a minimum asset threshold.

How to apply for a large home loan successfully

Securing a large loan mortgage requires preparation that goes well beyond gathering a few payslips. The documentation and strategy you bring to the table directly affect both your approval chances and the terms you receive.

Key steps to prepare a strong application:

- Compile full income evidence. Gather at least two to three years of payslips, P60s, tax returns, and company accounts where relevant. Include evidence of bonuses, dividends, and any other income streams.

- Prepare an asset statement. List all assets including savings, investments, pension values, and property holdings. Private banks in particular will want a complete picture of your balance sheet.

- Document your exit strategy. If you are applying for an interest-only or part-and-part mortgage, prepare written evidence of how you will repay the capital. Vague plans are rejected. Documented plans with supporting evidence are accepted.

- Check your credit profile. Large loan lenders scrutinise credit history carefully. Resolve any outstanding issues before applying. A clean credit record strengthens your position considerably.

- Consider combining incomes. Where two applicants are involved, combining incomes maximises the loan-to-income multiple available. Including all eligible income streams, such as bonuses and rental income, increases the total figure lenders will consider.

- Work with a specialist broker. A broker with experience in large loan mortgages knows which lenders are most likely to approve your specific profile. They can also negotiate terms and present your case in the most favourable light.

Avoiding common pitfalls matters as much as strong preparation. Overstretching affordability is the most frequent mistake at this level. A lender may approve a loan that leaves you financially exposed if rates rise or income falls. Borrow what you can comfortably service, not the maximum a lender will offer. Prosperhomeloans helps clients assess this balance honestly, so you borrow with confidence rather than anxiety.

Key takeaways

A large loan mortgage requires specialist underwriting, documented income, and a credible exit strategy, making early preparation and expert guidance the most reliable path to approval.

| Point | Details |

|---|---|

| Large mortgage definition | Loans from £500,000 are considered large; loans above £1 million trigger specialist underwriting. |

| Income multiples | High-street lenders offer up to 5.5x income for eligible professionals; private banks assess total assets. |

| Exit strategy required | Interest-only large loans require documented repayment plans such as property sale, pensions, or investments. |

| Lender choice matters | High-street suits straightforward profiles; private banks suit complex income, foreign currency, or bespoke needs. |

| Preparation is decisive | Full income evidence, a clean credit profile, and a clear exit strategy significantly improve approval chances. |

My honest view on large loan mortgages

Having worked with borrowers at the large loan level for many years, the single biggest mistake I see is treating a large mortgage as simply a bigger version of a standard one. The criteria are different, the underwriting is different, and the consequences of a poorly structured loan are far more serious.

The borrowers who succeed are the ones who engage early and disclose everything. Lenders at this level are not looking for perfection. They are looking for transparency and a coherent financial story. A borrower with a complex income mix who presents it clearly will often fare better than one with a straightforward salary who has not prepared properly.

My strongest advice is to be honest about your exit strategy from the start. I have seen applications fail not because the borrower could not afford the loan, but because they had no documented plan for repaying the capital. That is a fixable problem if you address it before applying.

Private banks are worth considering even if you think a high-street route will work. The flexibility they offer on income types, repayment structures, and loan sizes can make a meaningful difference to the terms you receive. The relationship requirement is real, but for borrowers with significant assets, it is often a worthwhile arrangement.

Finally, do not borrow to the absolute limit of what a lender will approve. The large loan market in 2026 operates in an environment where rates can shift and income can change. Build in a buffer. A mortgage you can comfortably service in a stress scenario is always the right choice.

— Paul

How Prosperhomeloans supports large mortgage applications

Prosperhomeloans specialises in making large and complex mortgage applications straightforward for clients who need more than a standard high-street product.

Whether you are purchasing a high-value property, refinancing an existing large loan, or exploring bespoke lending options through a private bank, our advisors assess your full financial profile and match you with the most suitable lender. We handle the documentation, manage lender relationships, and present your case in the strongest possible way. Clients who work with us avoid the delays and rejections that come from approaching the wrong lender with an unprepared application. Visit Prosperhomeloans to speak with an advisor and get personalised guidance on your large mortgage options.

FAQ

What is the minimum loan size for a large mortgage?

Most lenders treat loans from £500,000 as large, with loans above £1 million triggering full specialist underwriting and manual risk assessment.

What income multiples apply to large loan mortgages?

High-street lenders offer income multiples of up to 5.5 times combined income for eligible professionals, while private banks assess total assets and income mix rather than applying a fixed multiple.

Can I get a large mortgage on an interest-only basis?

Yes, but interest-only large mortgages face tighter LTV limits and require documented evidence of a credible exit strategy such as property sale, pension funds, or investment portfolios.

Does foreign currency income count towards a large mortgage?

Foreign currency income in USD, EUR, CHF, or AED is accepted by some lenders, but mainstream providers apply a discount to account for exchange rate risk before including it in affordability calculations.

Do I need a broker for a large loan mortgage?

A specialist broker significantly improves your chances of approval by identifying the right lender for your profile, presenting your application correctly, and negotiating terms that a direct approach rarely achieves.