What is a contractor mortgage? Your 2026 UK guide

A contractor mortgage is a standard residential mortgage assessed using specialist income calculation methods designed to reflect contractors’ actual earning capacity rather than a traditional salary. Most high-street lenders assess income using HMRC SA302 tax returns, which often underrepresent what contractors genuinely earn. Specialist lenders take a different approach, using your day rate to calculate a more accurate picture of your income. At Prosperhomeloans, we work with contractors every day who are surprised to discover how much more they can borrow once their income is assessed correctly. Understanding what is a contractor mortgage is the first step to unlocking your full borrowing potential.

How do lenders calculate income for contractor mortgages?

The income calculation method your lender uses determines how much you can borrow. Two distinct approaches exist, and the difference between them can be substantial.

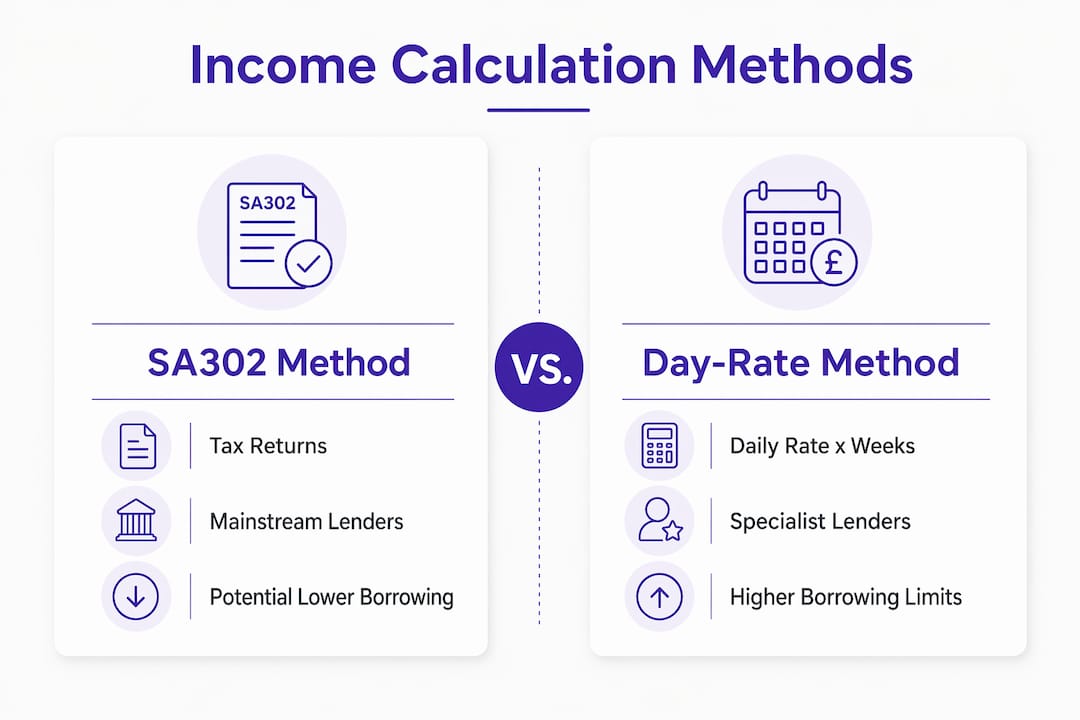

The SA302 method

Mainstream lenders, including Halifax, Nationwide, Barclays, and HSBC, assess Limited Company contractor income via SA302 tax forms at branch level. They typically average your net profit over two years. The problem is that most contractors structure their income tax-efficiently, drawing a low salary and taking dividends. This keeps your tax bill down but makes your declared income look far smaller than your actual commercial earnings.

The tax-efficient nature of contracting can paradoxically reduce your mortgage borrowing power when lenders rely solely on declared taxable income. A contractor earning £500 per day may show only £40,000 to £50,000 on their SA302, even though their commercial earnings are far higher.

The day-rate method

Specialist lenders use a different formula. They take your day rate and multiply it by five days and then by 46 or 48 working weeks per year. This produces an annualised income figure that reflects what you actually earn in the market. Lenders such as Kensington Mortgages, Saffron Building Society, and Vida Homeloans use this day-rate assessment method for contractors.

The impact on borrowing capacity is significant. For a £500 per day contractor, the SA302 method produces a maximum mortgage of approximately £304,000. The day-rate method produces a maximum of approximately £517,500. That difference of over £200,000 can mean the difference between buying a flat and buying a house, particularly in London and the South East.

Specialist lenders also apply income multiples of 4x to 5x the annualised day rate, with some reaching 5.5x for higher earners. That multiplier, applied to a realistic income figure, is what makes contractor mortgages so powerful for the right borrower.

Pro Tip: Always ask a broker which income assessment method a lender uses before applying. Applying to the wrong lender can result in a declined application that leaves a mark on your credit file.

| Assessment method | Income basis | Example max borrowing (£500/day) |

|---|---|---|

| SA302 (mainstream) | Salary plus dividends from tax return | Approximately £304,000 |

| Day-rate (specialist) | Day rate × 5 days × 46 weeks | Approximately £517,500 |

What are the benefits of contractor mortgages?

Contractor mortgages give you access to borrowing that reflects your real earning power, not just what appears on a tax return. The benefits go beyond a higher loan figure.

- Higher borrowing capacity. Day-rate underwriting can unlock borrowing limits 30% to 70% higher than SA302 self-employed assessments. For many contractors, this opens up a completely different range of properties.

- Flexibility for variable income. Specialist lenders understand that contractors work in rolling contracts rather than permanent employment. They assess your earning pattern rather than penalising gaps between contracts.

- Retained profit as a deposit. Contractors with funds sitting in their limited company can extract dividends to use as a deposit. Using retained profits for a deposit improves your loan-to-value ratio and gives you access to better mortgage products and lower rates.

- Reduced barriers with the right lender. Standard high-street applications based on salary and dividends can underestimate borrowing capacity by 30% to 70%. Specialist lenders remove that barrier by assessing income differently.

- Umbrella company contractors benefit too. Contractors working through umbrella companies are typically assessed as employees under PAYE. This simplifies the mortgage application process considerably, as lenders treat the income as employed income.

Pro Tip: If you are a limited company contractor, speak to your accountant before applying. Extracting the right amount of dividends in the tax year before your application can significantly improve your declared income without creating an unexpected tax liability.

The contractor home loan market has grown considerably as lenders have become more familiar with how contractors earn and manage their finances. The key is matching yourself to the right lender from the outset.

What documents do contractors need for a mortgage application?

Thorough documentation is the foundation of a successful contractor mortgage application. Lenders using the day-rate method need evidence that your contract income is genuine, consistent, and ongoing.

Prepare the following before you apply:

- Current contract. Your most recent contract should show your day rate, the client or agency name, and the contract end date. Lenders want to see that you are actively working and that the contract has at least four to six weeks remaining.

- Contract history. A clear record of previous contracts demonstrates continuity of work. Gaps are not automatically disqualifying, but you should be prepared to explain them.

- Invoices. Copies of recent invoices confirm that your contract income is being paid and matches the rate stated in your contract. Lenders use these to verify income consistency.

- Accountant’s reference letter. This is one of the most underused documents in contractor mortgage applications. An accountant’s reference letter explaining retained profits can be pivotal in bridging lender doubts about income stability and funds availability. It tells the lender why money is sitting in your company rather than being drawn as income.

- SA302 tax returns. Even if your lender uses day-rate assessment, many will still request two years of SA302 forms as supporting evidence. Have these ready from HMRC or your accountant.

- Bank statements. Both personal and business bank statements, typically covering three to six months, show the flow of income and confirm that your declared earnings match your actual receipts.

Stable, ongoing contracts are the key criterion for lenders using day-rate underwriting. The stronger your contract history, the more confident a lender will be in your application.

How does the contractor mortgage application process work?

Securing a contractor home loan follows the same broad steps as any residential mortgage, but the lender selection stage is far more important for contractors than for salaried employees.

- Choose a specialist broker. A whole-of-market broker with experience in contractor lending knows which lenders use day-rate assessment and which rely on SA302 forms. Specialist mortgage brokers knowledgeable about contractor incomes provide significant advantages in navigating lender requirements and unlocking higher lending. Prosperhomeloans works across the full market to find the right fit for your income profile.

- Understand lender panels. Not every lender accepts every type of contractor. Some lenders specialise in IT contractors, others in construction or professional services. Your broker should match you to a lender whose panel aligns with your sector and contract structure.

- Set realistic expectations on loan-to-value. A larger deposit improves your loan-to-value ratio and gives you access to better contractor mortgage rates. Most specialist lenders offer products from 75% to 90% LTV, with the most competitive rates available at 75% or below.

- Check your credit history. A clean credit file strengthens any application. Address any defaults, missed payments, or county court judgements before you apply, as specialist lenders still conduct full credit assessments.

- Consider contract timing. Applying when your contract has recently been renewed or has a long remaining term gives lenders greater confidence. Applying with only two or three weeks left on a contract can raise concerns about income continuity.

- Gather your documents early. The application process moves faster when your documentation is complete from the start. Missing documents are the most common cause of delays in contractor mortgage applications.

The mortgage options for contractors have expanded significantly as specialist lenders have entered the market. Working with a broker who understands this space means you are not limited to the products available on the high street.

Key takeaways

A contractor mortgage assessed by day-rate underwriting can unlock borrowing limits 30% to 70% higher than SA302 self-employed assessments, making lender and broker selection the most important decision in your application.

| Point | Details |

|---|---|

| Day-rate assessment unlocks more | Specialist lenders calculate income from your day rate, not your tax return, increasing borrowing capacity significantly. |

| SA302 method underestimates earnings | Mainstream lenders using SA302 forms can underestimate contractor borrowing capacity by 30% to 70%. |

| Documentation quality matters | A strong contract history, invoices, and an accountant’s reference letter are critical for specialist lender approval. |

| Retained profit can fund your deposit | Dividends extracted from your limited company can improve your loan-to-value ratio and product range. |

| Broker selection is decisive | A whole-of-market broker familiar with contractor lending directs you to the right lender from the outset. |

Paul’s view: the mistake most contractors make

Most contractors I speak to have already been turned down by a high-street bank before they come to us. The frustrating part is that the refusal was almost always avoidable. They applied to a lender that used SA302 assessment, their declared income looked low, and the bank said no. Their actual earning capacity was never in question.

The real issue is that tax-efficient contracting structures, which are entirely sensible from a financial planning perspective, can look like low income to a lender who does not understand contracting. A contractor drawing £12,000 in salary and £30,000 in dividends looks very different to a lender than a contractor earning £500 per day on a rolling contract. Both might be the same person.

My advice is always the same: do not apply to a mainstream lender without first speaking to a broker who specialises in contractor mortgages. The difference in outcome is not marginal. For a £500 per day contractor, it can mean borrowing £517,500 instead of £304,000. That is not a rounding error. That is a different property entirely.

The other mistake I see regularly is contractors who have retained significant profits in their company but have not thought about using those funds as a deposit. An accountant’s reference letter explaining the purpose of those retained profits can change how a lender views your entire application. It turns a potential red flag into a sign of financial discipline.

If you are asking yourself whether a contractor mortgage is right for you, the answer is almost certainly yes, provided you apply through the right channel with the right documentation.

— Paul

How Prosperhomeloans supports contractors with specialist mortgages

Contractors deserve mortgage advice that reflects how they actually earn, not how a standard application form expects them to earn.

Prosperhomeloans is a whole-of-market independent mortgage broker with direct access to specialist lenders who use day-rate underwriting. We guide you through every stage, from organising your documentation and accountant’s reference to matching you with the lender best suited to your contract structure and income profile. Whether you are a limited company contractor, a sole trader, or working through an umbrella company, we find the right mortgage solution for your circumstances. Get in touch with Prosperhomeloans today and let us do the work of finding you the best deal.

FAQ

What is a contractor mortgage in the UK?

A contractor mortgage is a standard residential mortgage assessed using specialist income methods, such as day-rate annualisation, rather than traditional SA302 tax returns. It is designed to reflect contractors’ actual earning capacity and typically enables higher borrowing than mainstream applications.

How is income calculated for a contractor mortgage?

Specialist lenders calculate income by multiplying your day rate by five days and then by 46 or 48 working weeks per year. This annualised figure is then used with an income multiple of 4x to 5.5x to determine your maximum borrowing.

What documents do I need for a contractor mortgage application?

You need your current contract, a contract history, recent invoices, two years of SA302 tax returns, personal and business bank statements, and an accountant’s reference letter explaining any retained profits in your company.

Can I use retained profits as a deposit for a contractor mortgage?

Yes. Dividends extracted from your limited company can be used as a deposit. A larger deposit improves your loan-to-value ratio and gives you access to better contractor mortgage rates and a wider product range.

Are contractor mortgage rates higher than standard mortgage rates?

Contractor mortgage rates from specialist lenders are generally competitive with standard residential rates. The rate you receive depends on your loan-to-value ratio, credit history, and the lender’s assessment of your income profile rather than your employment status alone.