Subcontractor remortgage process explained: 2026 guide

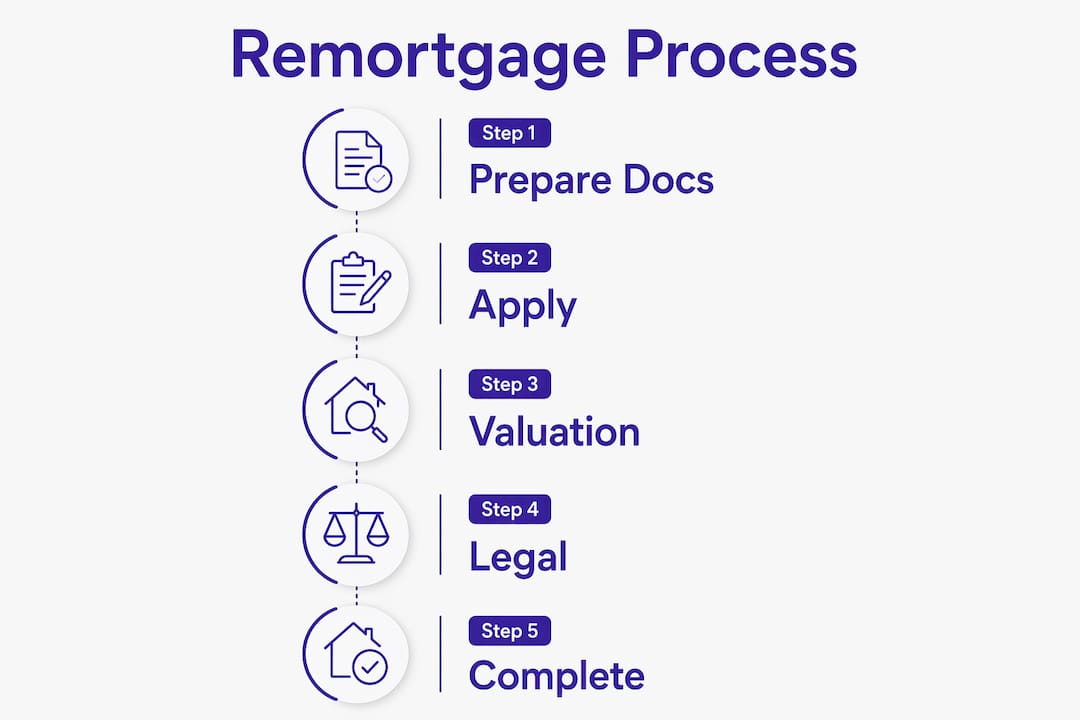

Remortgaging as a subcontractor is the process of switching your existing mortgage to a new deal, either with your current lender or a new one, to secure a lower rate, release equity, or both. The subcontractor remortgage process explained in full covers everything from income documentation to conveyancing and fees. Unlike standard employed borrowers, subcontractors face additional scrutiny from lenders such as Barclays, Leeds Building Society, and Halifax, who need to verify irregular income through CIS deduction certificates and SA302 tax calculations. The full process typically takes 4–8 weeks from application to completion. Getting it right from the start saves both time and money.

What documentation do UK subcontractors need for remortgaging?

Subcontractors must provide proof of identity, address, and income to satisfy lender requirements, and the income evidence is where most applications run into difficulty. Lenders cannot rely on a payslip. They need a clear picture of what you earn, how consistently you earn it, and how your tax affairs are managed.

Here is what you will need to prepare:

- Proof of identity: A valid passport or driving licence

- Proof of address: Recent utility bills or bank statements dated within the last three months

- SA302 tax calculations: Covering the last two to three years, obtained from HMRC or your accountant

- CIS deduction certificates: Monthly statements showing gross pay and tax deducted at source

- Bank statements: Typically three to six months of statements showing regular income deposits

- Current mortgage details: Your latest mortgage statement and any redemption figure

- Details of other financial commitments: Outstanding loans, credit cards, or hire purchase agreements

One area that catches subcontractors out is missing CIS statements. HMRC does not reissue monthly CIS deduction statements once they have been issued, so lost records can complicate both your tax refund claims and your mortgage application. Store them digitally as soon as they arrive, using a folder system by tax year.

Pro Tip: Use a dedicated email folder or cloud storage such as Google Drive to save each monthly CIS statement the moment it arrives. Rebuilding a two-year paper trail from scratch is far harder than maintaining one in real time.

Accurate record-keeping is not just good practice. It is the single biggest factor in how quickly your remortgage application moves forward.

Which mortgage products best suit subcontractors?

The right remortgage product depends on your financial goals, your risk appetite, and how long you plan to stay in the property. Subcontractors have access to the same products as employed borrowers, but eligibility criteria differ.

Fixed vs tracker rates

A fixed-rate mortgage locks your monthly payment for a set period, typically two or five years. This suits subcontractors well because it provides payment certainty even when contract income fluctuates. A tracker rate follows the Bank of England base rate, which can mean lower payments when rates fall but higher payments when they rise. For most subcontractors managing variable income, a fixed rate offers more predictability.

| Product Type | Rate Stability | Typical Term | Best For |

|---|---|---|---|

| 2-year fixed | High | 2 years | Short-term certainty, flexibility to switch |

| 5-year fixed | High | 5 years | Long-term stability, lower remortgage frequency |

| Tracker | Variable | 2–5 years | Borrowers expecting rate falls |

| Discount variable | Variable | 2–3 years | Short-term savings with some risk |

Staying with your lender vs switching

Staying with your current lender through a product transfer is faster and involves less paperwork. Switching to a new lender takes longer but often unlocks better rates and incentives. Many lenders offer free valuations and free legal work as part of remortgage packages, which can significantly reduce your upfront costs when switching.

A specialist contractor mortgage broker provides whole-of-market access and handles the paperwork on your behalf, often at no direct cost to you because the lender pays their fee. This is particularly valuable for subcontractors whose income structure requires careful presentation to lenders.

Pro Tip: Do not judge a remortgage deal on headline rate alone. A fee-free deal at a slightly higher rate can cost less overall than a low-rate deal with a £999 arrangement fee, depending on your loan size and term.

What are the legal steps in a subcontractor remortgage?

Conveyancing for a remortgage is simpler than for a property purchase because no change of ownership takes place. Remortgage conveyancing typically completes within 2–6 weeks, and a solicitor or licensed conveyancer manages the legal work on your behalf.

Here is how the legal process unfolds:

- Instruction of solicitor: Your lender appoints a solicitor, or you instruct your own if required. Many lenders include free legal work in their remortgage packages.

- Anti-money laundering checks: The solicitor verifies your identity and address to comply with UK regulations. This is a legal requirement, not a reflection of your creditworthiness.

- Title check: The solicitor reviews the title register at HM Land Registry to confirm ownership and check for any restrictions or charges on the property.

- Redemption statement: Your solicitor requests a redemption figure from your existing lender, confirming the exact amount needed to pay off your current mortgage.

- Review of mortgage offer: Once your new lender issues a formal mortgage offer, your solicitor reviews the terms and advises you on any conditions.

- Mortgage deed signing: You sign the new mortgage deed, which is a legal document binding you to the new loan terms.

- Completion: Funds are transferred to redeem the existing mortgage, and the new lender’s charge is registered with HM Land Registry.

If you are staying with your current lender on a product transfer, you may avoid conveyancing entirely. This reduces both cost and time, though it also means you are limited to that lender’s product range.

What costs should subcontractors budget for when remortgaging?

UK remortgage costs typically include arrangement fees of £0–£1,999, valuation fees of £150–£1,500, and solicitor fees that are often covered by lender packages. Understanding each cost helps you compare deals accurately rather than being surprised at completion.

| Cost Type | Typical Range | Notes |

|---|---|---|

| Arrangement fee | £0–£1,999 | Can be added to mortgage balance |

| Valuation fee | £150–£1,500 | Often free with lender incentives |

| Legal/conveyancing fee | £300–£600 | Often covered by lender packages |

| Broker fee | £0–£500 | Many brokers charge nothing to the client |

| Early repayment charge | 1–5% of balance | Only applies if leaving a deal early |

Early Repayment Charges (ERCs) are the largest potential cost. ERCs typically range from 1–5% of the outstanding mortgage balance and reduce each year over the deal period. On a £250,000 mortgage, a 3% ERC equals £7,500. That figure alone makes timing your remortgage correctly one of the most financially significant decisions you will make.

Adding your arrangement fee to the mortgage balance is an option many borrowers choose to avoid an upfront payment. However, a £1,000 arrangement fee added to a 25-year mortgage at 4.5% interest could cost roughly £670 in additional interest over the term. Paying the fee upfront, if you can afford to, is usually the cheaper option.

Pro Tip: Always calculate the total cost of a remortgage deal over the full fixed period, not just the monthly payment. Add up arrangement fees, any ERC, and estimated interest to get a true comparison figure.

How can subcontractors manage the remortgage application process?

A smooth remortgage application comes down to preparation and timing. Subcontractors who start early and use the right support avoid the most common delays.

- Start researching 4–6 months before your current deal ends. This gives you time to compare products, gather documents, and avoid rolling onto your lender’s standard variable rate, which is almost always higher.

- Get a Decision in Principle (DIP). A DIP uses a soft credit check and gives you a clear indication of how much you can borrow before you commit to a full application.

- Prepare all documentation in advance. Have your SA302 forms, CIS statements, bank statements, and ID ready before you apply. Delays in document submission are the most common cause of slow applications.

- Use a whole-of-market broker. A broker with experience in subcontractor financing options can identify lenders most likely to accept your income structure and negotiate on your behalf.

- Review your formal mortgage offer carefully. Check the rate, term, fees, and any conditions before signing. Ask your broker or solicitor to clarify anything you do not understand.

- Set a calendar reminder for your next review. Once your new deal is in place, note the date it ends and set a reminder for 4–6 months before. Repeat the process to keep your mortgage working for you.

Pro Tip: A Decision in Principle does not affect your credit score if the lender uses a soft search. Ask your broker to confirm this before proceeding, as some lenders still use hard searches at the DIP stage.

Key takeaways

Subcontractors who prepare their income documentation thoroughly and time their remortgage correctly will secure the best available rates and avoid unnecessary costs.

| Point | Details |

|---|---|

| Documentation is critical | SA302 forms, CIS statements, and bank statements are the foundation of any subcontractor remortgage application. |

| Timing avoids ERCs | Starting your search 4–6 months before your deal ends prevents costly early repayment charges. |

| Compare total costs | Arrangement fees, valuation fees, and legal costs must be added together to compare deals accurately. |

| Use a specialist broker | A whole-of-market broker with contractor experience provides access to lenders suited to subcontractor income. |

| Legal steps are manageable | Remortgage conveyancing is simpler than a purchase and typically completes within 2–6 weeks. |

What i have learned from years of subcontractor remortgage cases

The most consistent mistake I see subcontractors make is treating the remortgage process as identical to what an employed borrower experiences. It is not. Lenders assess subcontractor income differently, and the way you present that income on paper matters enormously.

I have worked with subcontractors who had strong earnings but poorly organised records, and their applications stalled for weeks while we chased down missing CIS statements or waited for HMRC to process SA302 requests. The subcontractors who sailed through had everything filed and ready. That preparation is entirely within your control.

My honest advice: do not rush into the first deal that looks attractive. I have seen borrowers save on headline rate only to pay more overall once ERCs and arrangement fees were factored in. The numbers only tell the full story when you look at the total cost across the fixed period.

Patience during the conveyancing stage also pays off. Solicitors are working through title checks and Land Registry processes that cannot be skipped. Chasing daily does not speed things up. What does help is responding to any requests from your solicitor or broker within 24 hours.

Remortgaging as a subcontractor is absolutely achievable, and the financial rewards, whether through a lower monthly payment or released equity, are real. The process rewards those who prepare well and take advice from people who understand the construction industry and the CIS scheme.

— Paul

Ready to remortgage? Prosperhomeloans can help

Prosperhomeloans specialises in mortgage and protection advice for subcontractors and self-employed individuals across the UK. We understand how CIS income, SA302 returns, and irregular payment schedules affect your application, and we know which lenders are most receptive to your circumstances.

Whether you are looking to reduce your monthly payments, release equity, or simply move off a standard variable rate, we can search the whole market on your behalf and handle the paperwork from start to finish. Most of our clients pay nothing for our advice, as lender fees cover our service. Visit Prosperhomeloans today to speak with a specialist and take the first step towards a better mortgage deal.

FAQ

What income proof do subcontractors need to remortgage?

Subcontractors need SA302 tax calculations, CIS monthly deduction certificates, and three to six months of bank statements. These documents give lenders a reliable picture of your income despite its variable nature.

How long does the subcontractor remortgage process take?

The remortgage process typically takes 4–8 weeks from application to completion. Delays most often occur when documentation is incomplete or when conveyancing queries arise.

Can subcontractors remortgage easily without two years of accounts?

Some lenders will consider applications with one year of accounts, particularly when CIS deduction certificates show consistent gross income. A specialist broker can identify which lenders apply more flexible criteria.

What is an early repayment charge and when does it apply?

An Early Repayment Charge applies when you leave a fixed or discounted mortgage deal before the agreed end date. ERCs typically range from 1–5% of your outstanding balance and reduce each year of the deal period.

Should subcontractors use a mortgage broker for remortgaging?

A specialist broker with contractor experience provides whole-of-market access and presents your income in the most favourable way to lenders. Many brokers charge nothing directly to the client, as lenders pay their fee.