Subcontractor limited company mortgage differences explained

The subcontractor limited company mortgage difference comes down to one thing: how a lender calculates your income. Operating through a limited company means your earnings are structured differently from a salaried employee or a sole trader, and lenders treat that structure in ways that can either significantly increase or reduce your borrowing power. Specialist lenders such as Halifax and Nationwide assess contractor income differently, and brokers like Prosperhomeloans can help you present your finances in the way that works best for your situation. Understanding these differences before you apply is the single most effective step you can take.

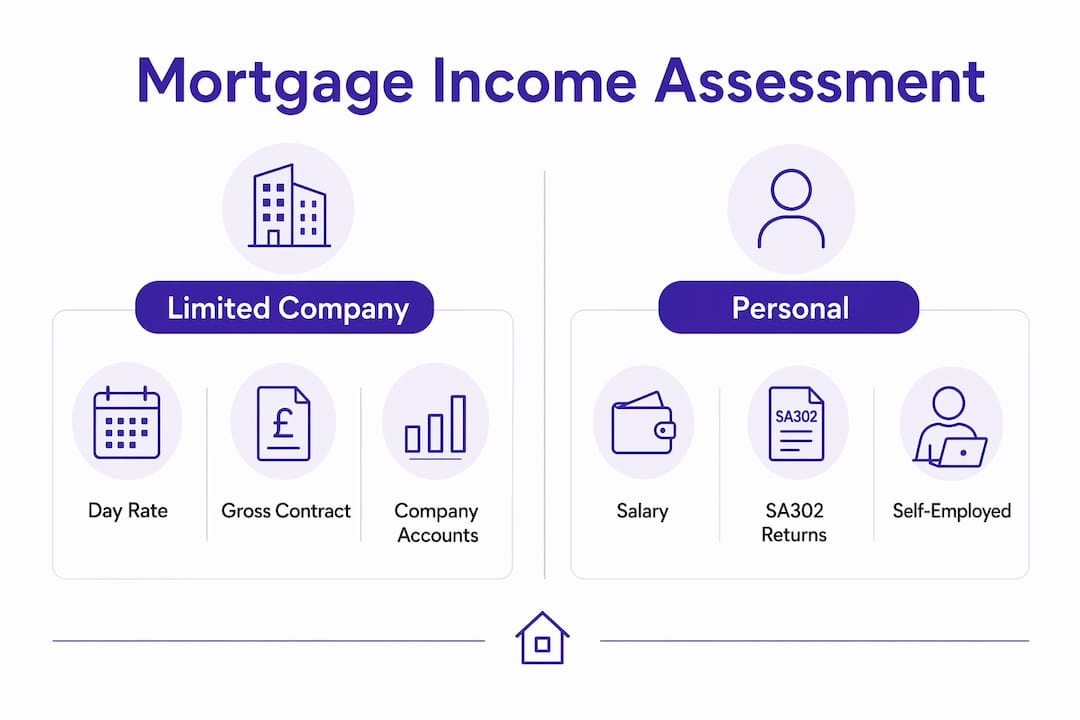

What is the subcontractor limited company mortgage difference?

The core distinction between a limited company mortgage and a personal or self-employed mortgage lies in income assessment. When you apply for a mortgage as an individual, lenders look at your salary, your SA302 tax returns, and typically two to three years of self-assessment records. When you apply through a limited company, lenders must decide whether to assess your director’s salary and dividends, your gross contract day rate, or a combination of both.

For subcontractors working outside IR35, specialist lenders often use the gross contract rate to calculate borrowing capacity, which produces a far higher figure than salary-based assessments. This is the most important difference in contractor mortgages and the one that most directly affects what you can borrow. A subcontractor earning £500 per day could potentially borrow £495,000 outside IR35 compared to £286,000 inside IR35, a difference of over £200,000 on the same gross income.

IR35 status is therefore not just a tax question. It is a mortgage question. If you are inside IR35, your lender will typically use your umbrella PAYE salary for affordability purposes. That net umbrella salary is usually only 58 to 62 per cent of your gross day rate, which reduces your borrowing capacity proportionally. Understanding your IR35 position before applying is not optional. It is the foundation of your mortgage strategy.

How do lenders assess subcontractor income for limited company mortgages?

Lender policies on contractor income vary considerably, and this variability is one of the most misunderstood aspects of buying a home as a subcontractor. Some lenders annualise your day rate as if you were a permanent employee, multiplying your daily rate by the number of working days in a year. Others require two full years of company accounts and SA302 returns, treating you more like a traditional self-employed applicant.

| Scenario | Day rate | IR35 status | Estimated borrowing |

|---|---|---|---|

| Outside IR35, day rate method | £500/day | Outside | Up to £495,000 |

| Inside IR35, umbrella salary | £500/day | Inside | Up to £286,000 |

| SA302 accounts method | £500/day | Outside | Varies by profit drawn |

The table above illustrates why IR35 status and lender choice matter so much. A subcontractor on the same day rate can face a borrowing gap of more than £200,000 depending on which method applies.

Some lenders also consider retained profits within company accounts as part of effective income for underwriting. Others ignore retained profits entirely, which can significantly reduce the borrowing limit for contractors who reinvest earnings into their business rather than drawing a high salary. This is a critical point that many subcontractors miss when they approach high-street lenders directly.

“The lender you choose matters as much as the rate they offer. A lender who understands contractor income will assess your finances completely differently from one who does not.”

Pro Tip: Before applying, ask any lender or broker directly whether they use day rate annualisation or company accounts for income assessment. The answer will tell you immediately whether they are the right fit for a subcontractor in your position.

IT and engineering contractors often receive more favourable assessments from lenders due to perceived income stability and sector reputation. If you work in construction or trades, you may need to work harder to demonstrate contract continuity, which is another reason specialist broker support is worth considering.

How do limited company buy-to-let mortgages compare to personal ones?

For subcontractors looking to invest in property, the differences in contractor mortgages between limited company buy-to-let and personal buy-to-let are significant. The structural, cost, and deposit requirements differ in ways that affect both short-term cash flow and long-term tax efficiency.

Key structural differences:

- Limited company buy-to-let mortgages are typically structured as interest-only products, which keeps monthly costs lower and improves cash flow for portfolio landlords

- SPV limited companies (Special Purpose Vehicles) with SIC codes 68100 or 68209 are preferred by many lenders for buy-to-let mortgages because they offer clearer risk assessment

- Personal buy-to-let mortgages are assessed on individual income and personal credit history, making them more straightforward but less tax-efficient for higher-rate taxpayers

- Limited company mortgages require a personal guarantee from directors, meaning your personal finances remain exposed despite the company structure

Cost and deposit requirements:

- Deposits typically range from 20 to 35 per cent for limited company buy-to-let mortgages, which is higher than many personal mortgage products

- Interest rates for limited company buy-to-let products sit at approximately 4.5 to 7.5 per cent as of 2026, reflecting the niche nature of this market

- Application timelines run from six to twelve weeks, longer than standard residential mortgages, due to additional legal and administrative requirements

Pro Tip: If you are setting up a limited company specifically for property investment, use an SPV rather than your trading company. Lenders prefer the clean structure, and it simplifies both accounting and future mortgage applications.

Specialist limited company mortgage lending remains a niche market with fewer lenders and less competitive rates than the mainstream. However, the strategic benefits for higher-rate taxpaying subcontractors can outweigh the additional costs, particularly when mortgage interest is treated as a deductible business expense against corporation tax.

What steps should UK subcontractors take when applying in 2026?

Applying for a limited company mortgage as a subcontractor requires preparation that goes beyond what a standard residential applicant needs. The following steps reflect what we consistently see working for subcontractors who secure the best outcomes.

-

Engage a specialist contractor mortgage broker early. Using a specialist broker can improve your borrowing capacity by £50,000 to £150,000 compared with going directly to a high-street lender. Brokers who understand subcontractor income know which lenders use day rate assessment and which require accounts.

-

Clarify your IR35 status before applying. Your IR35 position directly determines which income assessment method applies. If you are close to a contract renewal, consider the timing of your application carefully. Applying outside IR35 on a current contract produces a stronger application than applying mid-contract inside IR35.

-

Prepare your documentation thoroughly. You will typically need your current contract, recent CIS vouchers or invoices, two years of company accounts, SA302 tax returns, and a personal bank statement history. Lenders assessing limited company income want to see the full picture.

-

Understand personal guarantee requirements. Most lenders granting limited company mortgages require directors to sign personal guarantees. This means your personal assets are at risk if the company defaults. Factor this into your risk assessment before proceeding.

-

Present retained profits strategically. If your company holds significant retained profits, work with your broker to identify lenders who include these in their affordability calculations. Not all do, but those who do can unlock substantially higher borrowing limits.

-

Avoid common pitfalls. Do not apply to multiple lenders simultaneously without broker guidance, as hard credit searches can damage your credit score. Do not draw down large dividends immediately before applying, as this can distort your income picture.

Pro Tip: Ask your broker to provide a Decision in Principle from a lender who uses day rate assessment before you make any formal offer on a property. This protects you and confirms your borrowing capacity on the right terms.

How do tax considerations affect the choice between mortgage types?

Tax treatment is one of the most compelling reasons subcontractors consider limited company mortgage structures, but it is also one of the most complex areas to navigate without professional advice.

Potential tax advantages of limited company mortgages:

- Mortgage interest on a limited company buy-to-let is deductible against corporation tax, unlike personal mortgage interest which has been restricted to a basic-rate tax credit since 2020

- Corporation tax on company profits is currently lower than higher-rate income tax, which can make retaining profits within a company more tax-efficient for reinvestment

- Subcontractors can explore tax deductions available to limited companies that are not accessible to sole traders or personal landlords

Areas where limited company structures are less advantageous:

- Basic-rate taxpayers often gain little from the limited company structure, as the personal mortgage interest restriction has less impact at lower tax rates

- Capital Gains Tax and Stamp Duty Land Tax implications on transferring personally held properties into a limited company can be substantial

- Company setup costs, ongoing accountancy fees, and the administrative burden of running a separate SPV add to the overall cost of the structure

- Tax planning strategies that work well for one subcontractor may not suit another depending on income level, portfolio size, and long-term plans

The decision between a limited company mortgage and a personal mortgage is not purely a mortgage question. It is a tax planning question that requires input from an independent tax adviser who understands both contractor income and property investment. We always recommend taking that advice before committing to a structure.

Key takeaways

The subcontractor limited company mortgage difference is determined primarily by IR35 status, lender income assessment method, and tax structure, making specialist broker advice the single most important factor in securing the right deal.

| Point | Details |

|---|---|

| IR35 status changes everything | Outside IR35, day rate assessment can increase borrowing by over £200,000 compared to inside IR35 umbrella salary assessment. |

| Lender choice is critical | Some lenders use day rate annualisation; others require two years of accounts. The right lender makes a significant difference to what you can borrow. |

| Limited company buy-to-let costs more upfront | Deposits of 20 to 35 per cent and rates of 4.5 to 7.5 per cent apply, but tax efficiencies can offset these costs for higher-rate taxpayers. |

| Specialist brokers improve outcomes | Using a specialist contractor broker can increase borrowing capacity by £50,000 to £150,000 versus applying directly to a high-street lender. |

| Tax advice is non-negotiable | The choice between limited company and personal mortgage structures has significant tax implications that require independent professional advice. |

Why the right broker changes everything for subcontractors

After working with subcontractors and contractors for years, the pattern I see most often is this: the subcontractors who struggle with mortgage applications are not the ones with the weakest finances. They are the ones who went to the wrong lender first.

High-street lenders are built for salaried employees. Their underwriting systems are not designed to interpret a limited company structure, a day rate contract, or the nuances of IR35. When a subcontractor walks into a high-street branch and gets declined or offered a fraction of what they could borrow, it is not because their income is insufficient. It is because the lender’s model does not know what to do with it.

The subcontractors I see securing the best mortgage deals are those who understand their IR35 position clearly, have their documentation in order, and work with a broker who has direct relationships with lenders that specialise in contractor income. That combination is not complicated, but it requires knowing where to look.

I would also caution against over-optimising for tax efficiency at the expense of simplicity. A limited company buy-to-let structure can be genuinely advantageous for higher-rate taxpayers, but the administration, the personal guarantee exposure, and the additional costs are real. For some subcontractors, a straightforward personal mortgage remains the better choice. The key is making that decision with full information, not assumptions.

— Paul

How Prosperhomeloans helps subcontractors secure the right mortgage

If you are a subcontractor operating through a limited company and you want clarity on your mortgage options, Prosperhomeloans is built for exactly this situation.

We work with a panel of specialist lenders who understand contractor income, day rate assessment, and the differences that IR35 status creates in affordability calculations. Our advisers know how to present your limited company income in the way that maximises your borrowing power, whether you are buying a home or investing in buy-to-let property. We handle the complexity so you do not have to. Contact Prosperhomeloans today for a no-obligation conversation about your mortgage options as a subcontractor.

FAQ

What is the main difference between a limited company mortgage and a personal mortgage?

The primary difference is how lenders assess your income. Personal mortgages use salary and SA302 tax returns, while limited company mortgages may use day rate annualisation, company accounts, or a combination of both, producing significantly different borrowing outcomes.

Does IR35 status affect my mortgage application as a subcontractor?

Yes, directly. Outside IR35, specialist lenders can use your gross day rate to calculate borrowing capacity. Inside IR35, lenders use your net umbrella salary, which is typically only 58 to 62 per cent of your gross rate, reducing what you can borrow considerably.

Do I need a specialist broker for a limited company mortgage?

Using a specialist contractor mortgage broker can increase your borrowing capacity by £50,000 to £150,000 compared with applying directly to a high-street lender, because specialist brokers access lenders who understand contractor income structures.

What deposit do I need for a limited company buy-to-let mortgage?

Limited company buy-to-let mortgages typically require a deposit of between 20 and 35 per cent, which is higher than many personal mortgage products. Interest rates currently range from approximately 4.5 to 7.5 per cent as of 2026.

Is a limited company mortgage always more tax-efficient for subcontractors?

Not always. Limited company structures offer tax advantages for higher-rate taxpayers, particularly through mortgage interest deductions against corporation tax. However, basic-rate taxpayers may see limited benefit, and the additional costs and administration can outweigh the savings. Independent tax advice is always recommended.