Self-employed vs subcontractor mortgage: 2026 guide

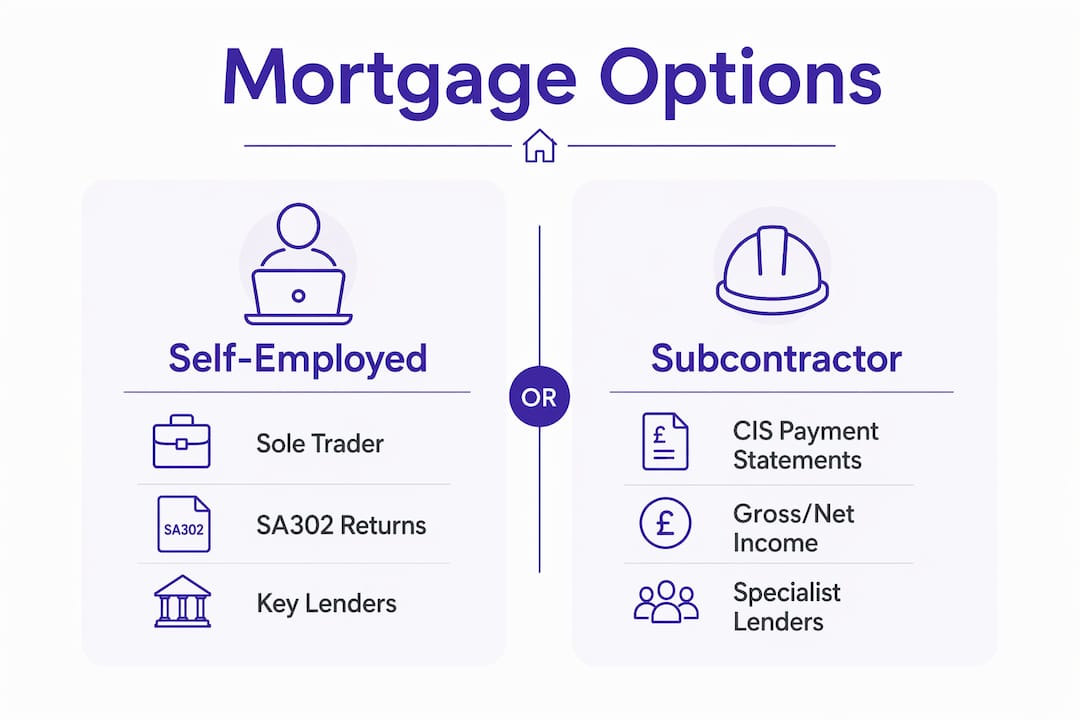

A self-employed vs subcontractor mortgage refers to the distinct ways UK lenders evaluate income, financial stability, and documentation for these two groups when assessing home loan applications. The distinction matters more than most applicants realise. Self-employed borrowers typically rely on HMRC self-assessment tax returns and SA302 forms, while subcontractors working under the Construction Industry Scheme (CIS) can present CIS payment statements and contract evidence as proof of income. Getting this right from the start determines how much you can borrow and which products you can access.

How do lenders assess income differently for self-employed vs subcontractors?

Lenders assess self-employed applicants primarily through SA302 tax returns and their corresponding tax year overviews from HMRC. These documents show net profit after expenses, which becomes the figure used in affordability calculations. If your accountant has legitimately reduced your taxable income through allowable expenses, that same reduction can lower the amount a lender will lend you.

Subcontractors registered under CIS are assessed differently by lenders who understand the scheme. Rather than relying solely on net profit, some lenders accept gross CIS income as the basis for affordability, which can significantly increase borrowing capacity. This is one of the most important practical distinctions in the self-employed vs subcontractor mortgage comparison.

Lenders prefer documented income of at least two years for both groups. That two-year threshold exists because it demonstrates a reliable revenue stream rather than a single good year. Less than two years of trading history typically disqualifies applicants from many standard products.

Key income evidence lenders request includes:

- SA302 forms and tax year overviews for the past two years (self-employed)

- CIS payment statements showing gross income deducted at source (subcontractors)

- Bank statements covering three to six months of personal and business accounts

- Accountant letters confirming income, trading status, and financial health

- Contracts or letters of engagement to evidence ongoing work (particularly useful for subcontractors)

Pro Tip: If you are a subcontractor, ask your lender or broker explicitly whether they will assess your gross CIS income rather than your net profit. The difference can add tens of thousands of pounds to your maximum loan.

Expense ratios create another layer of complexity. Residential electricians carry 40–55% expense ratios, while general contractors can see ratios of 70–80%. Those figures mean a general contractor earning £100,000 in revenue may show only £20,000–£30,000 in net profit, which directly caps their borrowing power unless the lender is given proper context.

What mortgage options are available to self-employed and subcontractors?

The mortgage market in 2026 offers more options for non-standard borrowers than it did a decade ago, but the right product depends heavily on your employment structure.

| Borrower Type | Typical Product | Income Evidence Used | Key Lenders |

|---|---|---|---|

| Sole trader (self-employed) | Standard residential mortgage | SA302, tax returns, bank statements | NatWest, Halifax, Nationwide |

| CIS subcontractor | Specialist contractor mortgage | Gross CIS statements, contracts | Aldermore, Foundation Home Loans |

| Limited company contractor | Residential mortgage (self-employed basis) | SA302, company accounts, dividends | Aldermore, specialist brokers |

| Day rate contractor | Contractor mortgage | Daily rate annualised, contracts | Foundation Home Loans, specialist lenders |

Standard residential mortgages are accessible to self-employed borrowers who can demonstrate two years of stable net profit. The calculation is straightforward: most lenders will offer four to four and a half times your average net profit over two years. The challenge is that legitimate tax planning often reduces the net profit figure, which works against you at the mortgage stage.

Lenders such as Aldermore and Foundation Home Loans consider daily rate income from self-employed and contractor borrowers, provided full supporting documentation is in place. This is particularly relevant for subcontractors who work on fixed-term contracts with a clear daily or weekly rate. Annualising that rate (daily rate multiplied by 46–48 working weeks) can produce a much higher income figure than tax returns alone would suggest.

Limited company contractors are often treated as self-employed for mortgage purposes. This means the lender looks at your SA302 and company accounts rather than your company’s turnover. If you pay yourself a low salary and take dividends, both figures are typically combined for affordability purposes.

Which documentation improves mortgage approval for self-employed applicants?

Strong documentation is the single most controllable factor in your mortgage application. Both self-employed individuals and subcontractors can materially improve their approval chances by preparing the right paperwork before approaching a lender.

For self-employed borrowers, the core documents are:

- SA302 tax calculations for the last two tax years

- Corresponding HMRC tax year overviews

- Three to six months of personal bank statements

- Three to six months of business bank statements

- A letter from a qualified accountant confirming your trading status and income

For subcontractors, the documentation list overlaps but includes CIS-specific evidence:

- CIS payment and deduction statements (monthly vouchers from contractors)

- Current contracts or letters of engagement from principal contractors

- Bank statements showing regular CIS payments received

- An accountant’s letter explaining your gross income and expense structure

A professional accountant’s expense ratio letter is often the most influential document in the underwriting process for contractors and subcontractors. It translates complex revenue and expense flows into a net margin figure that lenders can use with confidence. Without it, an underwriter may apply a generic expense assumption that underestimates your true income.

Separating your business and personal finances is equally important. Lenders scrutinise bank statements carefully, and keeping business finances separate removes ambiguity about where income originates. Mixed accounts create questions that slow down underwriting and can trigger additional information requests.

Pro Tip: Commission a formal accountant’s letter specifically written for mortgage purposes, not just a standard reference. Ask your accountant to include your average net profit, your expense ratio, and a statement confirming your business is a going concern.

Working with a specialist accountant who understands mortgage underwriting is worth the investment. The essential guide to accountants for sole traders explains how professional income statements can directly influence what lenders will offer you.

How do expense ratios and cash flow affect mortgage eligibility?

Expense ratios are the percentage of gross revenue consumed by business costs. They vary significantly by trade, and understanding your own ratio is critical before you apply for a mortgage.

| Trade | Typical Expense Ratio | Net Income on £80,000 Revenue |

|---|---|---|

| Residential electrician | 40–55% | £36,000–£48,000 |

| Plumber / gas engineer | 45–60% | £32,000–£44,000 |

| General contractor | 70–80% | £16,000–£24,000 |

| IT contractor (day rate) | 15–25% | £60,000–£68,000 |

A general contractor earning £80,000 in revenue may show net income of just £16,000–£24,000 on their tax return. At a standard four times income multiplier, that translates to a maximum mortgage of £64,000–£96,000. The same contractor, assessed on gross CIS income with an accountant’s letter explaining the expense structure, could access a substantially higher loan.

Cash flow patterns also differ between self-employed individuals and subcontractors. Subcontractors frequently experience payment delays tied to project milestones, retentions held by principal contractors, and seasonal construction cycles. Subcontractor financing options such as invoice financing and lines of credit address short-term project costs, but these are distinct from residential mortgages. Lenders reviewing bank statements may see irregular deposits and interpret them as income instability unless you explain the pattern clearly.

Mobilisation capital advances secured against contracts are another tool subcontractors use for project startup costs, accessible within 24–72 hours without traditional bank underwriting. While useful for cash flow, these advances appear on bank statements and can raise questions during mortgage underwriting if not explained. A brief covering letter from your accountant or broker addressing the nature of these transactions removes any doubt.

The most common misconception is that earning more automatically means borrowing more. For self-employed and subcontractor borrowers, the relationship between gross revenue and mortgage eligibility is filtered through expense ratios, tax treatment, and lender policy. Understanding your trade’s expense ratio and communicating it effectively through a CPA or accountant letter can materially increase your borrowing capacity.

Key takeaways

Self-employed and subcontractor borrowers face different lender assessments, and understanding which income evidence applies to your situation is the most direct way to maximise your mortgage eligibility.

| Point | Details |

|---|---|

| Income evidence differs by status | Self-employed borrowers use SA302 returns; CIS subcontractors can use gross payment statements. |

| Two years of history is the standard | Most lenders require at least two years of documented income to consider your application. |

| Expense ratios directly affect borrowing | A high expense ratio reduces net profit, which caps your loan unless explained by an accountant’s letter. |

| Product choice depends on your structure | Sole traders, CIS subcontractors, and limited company contractors each access different mortgage products. |

| Documentation quality changes outcomes | A well-prepared accountant’s letter and separated bank accounts can materially improve your approval chances. |

What i have learned after years of advising self-employed borrowers

The biggest mistake I see self-employed individuals and subcontractors make is approaching a high street lender without specialist preparation. Standard bank branches are not set up to assess CIS income or explain expense ratios to underwriters. They apply generic criteria, and that almost always works against non-standard borrowers.

What actually moves the needle is preparation done three to six months before you apply. Get your SA302s in order. Commission an accountant’s letter written specifically for mortgage purposes. If you are a CIS subcontractor, gather every monthly payment statement you have. These documents do not just satisfy a checklist. They tell a coherent financial story that an underwriter can follow.

The other thing I would say is this: do not let tax efficiency work against your mortgage. Many self-employed clients have spent years legitimately reducing their taxable income, then wonder why lenders will not lend them what they need. There is a balance to strike, and a specialist broker who understands both the tax and mortgage sides of your situation can help you find it before you file your next return.

Seek advice early. The clients who come to us six months before they want to buy are in a far stronger position than those who come to us the week they find a property.

— Paul

How Prosperhomeloans supports self-employed and subcontractor applicants

Prosperhomeloans specialises in finding the right mortgage for self-employed individuals and subcontractors across the UK. We work with lenders who understand CIS income, daily rate contracts, and the realities of running your own business. That means we can match you with products that reflect your actual earnings rather than just your tax return.

Whether you are a sole trader with two years of accounts, a CIS subcontractor with strong gross income, or a limited company contractor looking for the right lender approach, we can help. Our advisors take the time to understand your financial picture before recommending a solution. Visit Prosperhomeloans to speak with an advisor who knows exactly how to present your application to the right lender.

FAQ

What is the difference between a self-employed and subcontractor mortgage?

A self-employed mortgage is assessed using SA302 tax returns and net profit, while a subcontractor mortgage can be assessed using gross CIS payment statements and contract evidence. The key difference is which income figure the lender uses for affordability calculations.

How many years of accounts do i need as a self-employed applicant?

Most lenders require a minimum of two years of documented income history. Less than two years in business typically disqualifies applicants from standard mortgage products.

Can a CIS subcontractor get a mortgage based on gross income?

Yes. Some lenders, including Aldermore and Foundation Home Loans, will assess CIS subcontractors on gross income rather than net profit, which can significantly increase borrowing capacity compared with a standard self-assessment basis.

Does being a limited company contractor affect my mortgage options?

Yes. Limited company contractors are treated as self-employed for mortgage purposes, meaning lenders assess salary and dividends from SA302 returns rather than company turnover. A specialist broker can identify lenders with the most favourable approach for your structure.

How do i improve my chances of mortgage approval as a subcontractor?

Gather two years of CIS payment statements, maintain separate business and personal bank accounts, and commission an accountant’s letter that explains your gross income and expense ratio. These three steps address the most common reasons subcontractor applications are delayed or declined.