Secured loan vs remortgage explained for UK homeowners

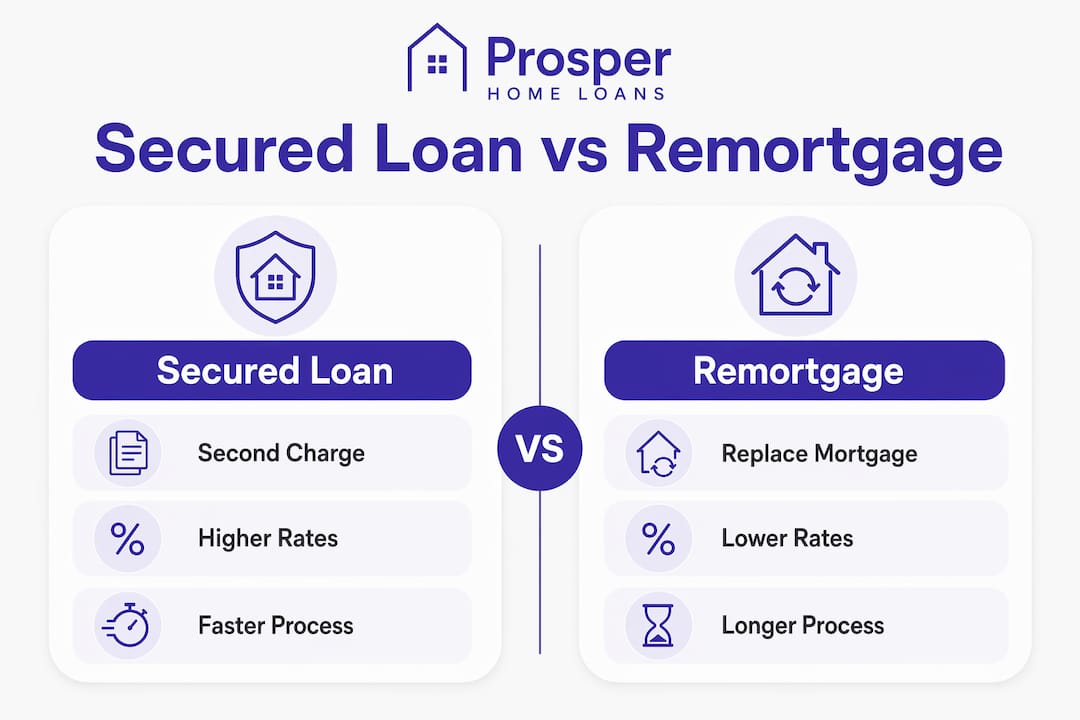

A secured loan is defined as a second legal charge loan registered on your property alongside your existing mortgage, while a remortgage replaces your current mortgage entirely with a new deal. These are the two most common ways UK homeowners borrow against their property, and choosing between them has real financial consequences. The secured loan vs remortgage explained comparison comes down to one core question: do you want to keep your existing mortgage or replace it? Getting this decision right can save you thousands of pounds in charges, interest, and fees.

How does a secured loan work compared to a remortgage?

A secured loan sits behind the first mortgage as a second legal charge, registered at HM Land Registry. Your original mortgage stays in place, untouched. The secured loan is a separate borrowing arrangement with its own lender, its own rate, and its own monthly payment.

A remortgage works differently. It repays your existing mortgage balance in full and replaces it with a new loan, usually from a different lender. You end up with one mortgage, one payment, and one lender. The new mortgage covers both your original balance and any additional funds you want to release.

The practical difference shows up immediately in your monthly outgoings. With a secured loan, you make two separate payments each month. With a remortgage, everything consolidates into one. Neither approach is automatically better. The right choice depends on your existing rate, your remaining mortgage term, and whether your lender charges an early repayment penalty.

Key mechanics to understand:

- A secured loan leaves your first mortgage deal completely intact.

- A remortgage triggers a full exit from your current mortgage deal.

- Secured loans are assessed by a second charge lender, not your existing mortgage provider.

- Remortgages require you to pass a full affordability and credit assessment with the new lender.

- Both options use your property as security, so your home is at risk if you cannot keep up repayments.

Pro Tip: If your current mortgage has more than 12 months left on a fixed rate, calculate the early repayment charge before assuming a remortgage is cheaper. The penalty alone can outweigh any rate saving.

What are the cost differences between a secured loan and a remortgage?

Interest rates on secured loans are generally higher than remortgages, ranging roughly 4% to 12% depending on loan-to-value ratio, credit score, and the amount borrowed. That headline figure can make secured loans look expensive. The comparison is more nuanced than it first appears.

A remortgage often carries a lower headline rate, but it applies to your entire mortgage balance, not just the new money you are borrowing. If you originally borrowed £200,000 at 1.9% and you remortgage the full balance at 4.5% to release £30,000, you are paying the higher rate on all £200,000. The secured loan charges a higher rate only on the £30,000.

Early Repayment Charges on an existing mortgage typically range from 1% to 5% of the outstanding balance. On a £200,000 mortgage, that is between £2,000 and £10,000 in exit penalties alone. A secured loan avoids triggering these charges entirely, because it does not repay the first mortgage.

| Cost factor | Secured loan | Remortgage |

|---|---|---|

| Interest rate | Higher rate, on new borrowing only | Lower rate, on entire mortgage balance |

| Early repayment charge | Not triggered | Triggered if in fixed period |

| Arrangement fee | Typically lower | Can be £999 or more |

| Valuation fee | Usually required | Usually required |

| Legal costs | Minimal | Solicitor fees apply |

| Monthly payments | Two separate payments | One combined payment |

Remortgaging can spread all borrowing over a new, longer term, which may increase total interest paid compared to adding a secured loan over a shorter term on just the new borrowing. Borrowers regularly underestimate how term extension affects total cost.

Pro Tip: Isolate the cost of the new borrowing only when comparing total interest between a remortgage and a secured loan. Failing to do so can falsely suggest secured loans are always more expensive, which is not the case in many practical scenarios.

When is a secured loan or remortgage the better choice?

The decision hinges on practical borrower circumstances, particularly the size of any early repayment charge on the existing mortgage. There is no universal answer, but there are clear patterns that point toward one option or the other.

A secured loan tends to suit you better when:

- You are mid-way through a fixed rate deal with a significant early repayment charge.

- Your existing mortgage rate is below current market rates, particularly deals secured between 2020 and 2022.

- You want to borrow a specific sum without disturbing a favourable long-term mortgage arrangement.

- You need funds quickly, since secured loans can be arranged faster than remortgages due to less paperwork and complexity.

- Your circumstances have changed and you may not pass a full remortgage affordability assessment.

A remortgage tends to suit you better when:

- Your fixed rate period is ending and you face moving to a higher standard variable rate.

- Your existing mortgage rate is already uncompetitive and you would benefit from switching.

- You want to consolidate all borrowing into one simple monthly payment.

- You are borrowing a large sum and the lower remortgage rate on the full balance produces a better total cost outcome.

- Your income and credit profile are strong and you will pass the full reassessment comfortably.

Secured loans also offer flexibility in accessing funds in stages, preserving existing deals, and avoiding mortgage break penalties. This makes them particularly useful for home improvement projects where costs arrive in phases rather than as a single lump sum.

How do the application processes differ?

A remortgage triggers a full reassessment of income, employment, and credit status. The new lender treats your application as if you are taking out a mortgage for the first time. This matters if your circumstances have changed since your original mortgage was approved.

A secured loan application is generally more flexible. Second charge lenders assess affordability differently and often accept a wider range of income types, employment situations, and credit histories. This flexibility can be the deciding factor for homeowners who are self-employed, have changed jobs, or carry some adverse credit.

The practical steps for a remortgage application look like this:

- Obtain a new mortgage agreement in principle from your chosen lender.

- Submit full documentation including payslips, bank statements, and proof of identity.

- The lender instructs a valuation of your property.

- A solicitor handles the legal transfer and repayment of the existing mortgage.

- Completion typically takes 4–8 weeks from application.

A secured loan follows a shorter path. The second charge lender assesses your application, instructs a valuation, and registers the second charge at HM Land Registry. The process typically completes faster than a remortgage, which matters when you need funds within a specific timeframe.

Having a secured loan does not necessarily affect your ability to remortgage in the future, but any affordability assessment will account for the secured loan repayment as an existing financial commitment. Credit score, loan-to-value ratio, and overall affordability remain the key factors.

Key takeaways

A secured loan keeps your existing mortgage intact and adds a second charge, while a remortgage replaces the entire mortgage, making the right choice dependent on your current rate, early repayment charges, and personal financial circumstances.

| Point | Details |

|---|---|

| Core difference | A secured loan adds a second charge; a remortgage replaces the first mortgage entirely. |

| Early repayment charges | ERCs of 1%–5% on the existing balance can make a secured loan cheaper overall. |

| Interest rate comparison | Secured loan rates are higher but apply only to new borrowing, not the full mortgage balance. |

| Application flexibility | Secured loans suit borrowers with changed circumstances who may not pass a full remortgage assessment. |

| Total cost calculation | Always isolate the cost of new borrowing only to make an accurate like-for-like comparison. |

Paul’s view: the number that changes everything

Most homeowners focus on the headline interest rate when comparing these two options. That is the wrong starting point. The number that actually changes the outcome is the early repayment charge on your existing mortgage.

I have seen clients dismiss a secured loan because the rate looked higher, only to discover their ERC was £6,000. Once that penalty was factored in, the secured loan was clearly the better financial decision. The rate comparison only tells part of the story.

The other factor I see underestimated regularly is term extension. Remortgaging feels tidy because you end up with one payment. But if you add 15 years to your mortgage term to keep that payment manageable, the total interest cost can far exceed what a shorter-term secured loan would have cost. Tidy is not always cheap.

My honest advice is this: do not make this decision based on a single number. Compare the total cost of both options over the same period, account for all fees, and consider what your existing mortgage rate is actually worth to you. If you locked in a rate below 2% in 2021, that deal has real monetary value. Protect it unless the numbers clearly say otherwise.

— Paul

Explore your options with Prosperhomeloans

Whether you are considering a secured loan or a remortgage, getting the right advice from the start saves both time and money.

At Prosperhomeloans, we are independent mortgage and protection advisors who work across the whole of the UK market. We compare secured loan and remortgage options side by side, accounting for your existing deal, any early repayment charges, and your personal circumstances. We do the heavy lifting so you can make a confident, informed decision. Speak to our team at Prosperhomeloans to find the right solution for your situation.

FAQ

What is the main difference between a secured loan and a remortgage?

A secured loan is a second legal charge added to your property alongside your existing mortgage. A remortgage replaces your existing mortgage with a new deal, usually from a different lender.

Will a secured loan affect my ability to remortgage later?

Having a secured loan does not prevent you from remortgaging, but future lenders will include the secured loan repayment in their affordability assessment. Your credit score and loan-to-value ratio remain the key eligibility factors.

When does a secured loan work out cheaper than a remortgage?

A secured loan is often cheaper when your existing mortgage carries a significant early repayment charge, typically 1%–5% of the outstanding balance, or when your current mortgage rate is well below today’s market rates.

How long does a secured loan application take compared to a remortgage?

Secured loans generally complete faster than remortgages due to less paperwork and a more flexible assessment process. A remortgage typically takes 4–8 weeks from application to completion.

Can I get a secured loan if my circumstances have changed since my original mortgage?

Yes. Secured loan lenders use more flexible income and credit criteria than remortgage lenders. Homeowners who are self-employed, have changed jobs, or carry some adverse credit often find a secured loan more accessible than a remortgage.