Secured loan broker role explained for UK borrowers

A secured loan broker is a qualified, FCA-regulated intermediary who helps borrowers find appropriate secured loan products by assessing their financial circumstances, managing lender relationships, and guiding the application from start to completion. Understanding the secured loan broker role explained in full gives you a clear picture of why so many borrowers achieve better outcomes with professional guidance than without it. Secured loans are regulated, advised products. That means a qualified broker must be involved to verify suitability and provide personalised cost illustrations before any commitment is made. At Prosperhomeloans, we work with borrowers every day who benefit directly from this structured, expert-led process.

What does a secured loan broker do?

A secured loan broker acts as the intermediary between you and a panel of lenders, matching your financial profile to the most suitable loan products available. The broker’s primary job is not simply to find a rate. It is to assess whether a secured loan is appropriate for your circumstances in the first place.

The assessment process covers several key areas:

- Affordability review: The broker examines your income, outgoings, existing debts, and property equity to determine what you can realistically repay.

- Credit risk evaluation: Your credit history is reviewed to identify which lenders are likely to accept your application and on what terms.

- Lender matching: Your profile is compared against the criteria of lenders on the broker’s panel to find the closest fit.

- Soft search checks: Soft search technology allows brokers to check your eligibility without leaving a mark on your credit file. Hard searches by direct lenders do leave a mark, which can affect future borrowing.

- Personalised illustrations: FCA regulations mandate that brokers provide full cost illustrations before you commit to any product.

This process protects you from applying to lenders who would decline you, which matters because each declined application can damage your credit score.

Pro Tip: Ask your broker how many lenders are on their panel before you proceed. A broker with access to 30 or more lenders gives you far more competitive options than one with a restricted panel.

The broker also has a legal obligation to act in your best interest. That duty applies regardless of how the broker is paid, which brings us to the question of fees.

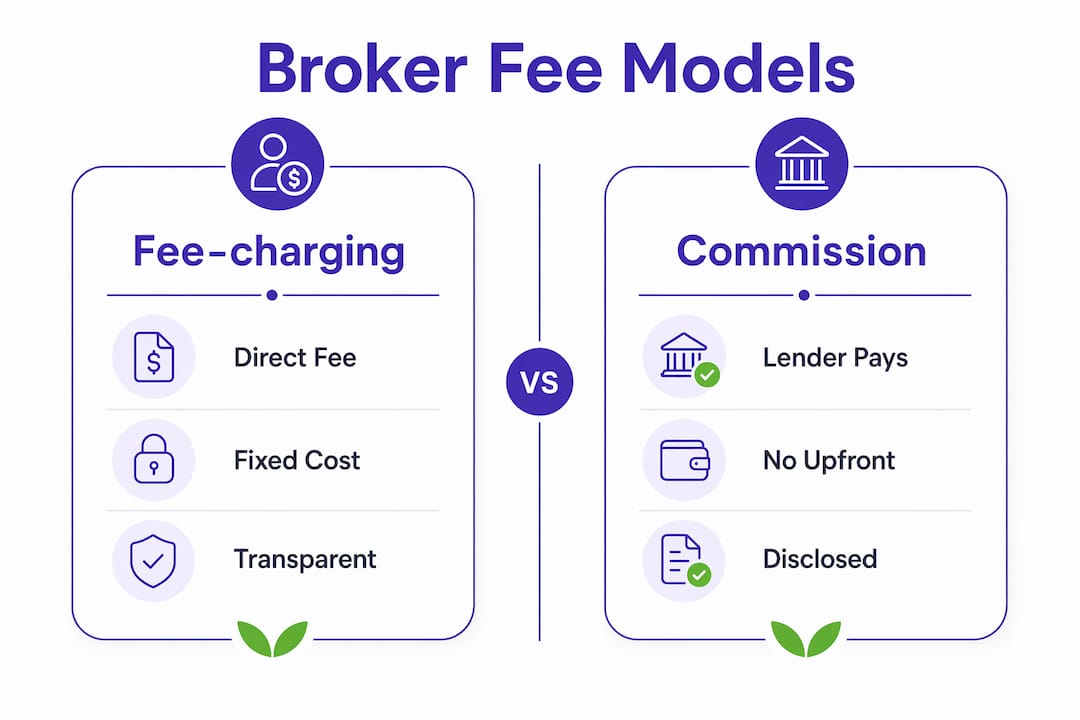

How are secured loan brokers paid in the UK?

Broker fee structures in the UK follow one of three models, each with different implications for you as a borrower.

| Fee model | How it works | Typical cost to borrower |

|---|---|---|

| Fee-charging | Broker charges you directly for their service | £500–£1,500 or 0.5%–1.5% of loan amount |

| Commission-only | Lender pays the broker; no direct cost to you | £0 direct cost, but commission built into product |

| Hybrid | Broker charges a reduced fee and receives lender commission | Lower direct fee than pure fee-charging model |

FCA rules require brokers to disclose all fees and commissions before making a recommendation. That disclosure must happen in writing, and you must receive it before any application is submitted on your behalf.

A common misconception is that commission-only brokers are less independent than fee-charging ones. Independence is better measured by the breadth of a broker’s lender panel, not by their fee model. A whole-of-market broker with access to 30 or more lenders provides genuinely competitive advice regardless of how they are remunerated.

Pro Tip: Always ask for a Key Facts Illustration (KFI) before signing anything. This document sets out the total cost of the loan, including broker fees, so you can compare products on a like-for-like basis.

The hybrid model is increasingly common among specialist brokers. It balances the broker’s commercial needs with a lower upfront cost to you, while still maintaining full FCA disclosure obligations.

Why use a broker instead of going directly to a lender?

Going directly to a lender feels straightforward, but it carries real risks that many borrowers only discover mid-application. A broker provides several advantages that a direct lender simply cannot replicate.

- Whole-of-market access: A broker with a broad lender panel presents you with options from across the market, not just one lender’s product range. This increases the likelihood of finding a competitive rate suited to your profile.

- Credit file protection: Brokers use soft search checks to filter out unsuitable lenders before any hard search is triggered. This protects your credit score during the exploratory phase.

- Access to specialist lenders: Many specialist lenders only accept applications via brokers. If your situation involves self-employment, complex income, or a non-standard property, a broker may be the only route to the right product.

- Active case management: Experienced brokers coordinate all aspects of the application, including liaising with valuers, solicitors, and lenders, to keep the process on track and prevent unnecessary delays.

- Reduced application errors: A broker reviews your documentation before submission. Errors or missing information are caught early, reducing the risk of a declined application or a prolonged process.

The broker-only market is a significant sector in UK secured lending. Loans that are inaccessible without an intermediary are particularly common for borrowers with non-standard profiles or properties. Without a broker, those products simply are not available to you.

The active case management point deserves emphasis. When a valuation is delayed or a solicitor is slow to respond, a broker chases on your behalf. You do not have to navigate those conversations yourself, which reduces both stress and the risk of the application stalling.

What are the key responsibilities of a secured loan broker?

A secured loan broker carries both legal and ethical duties under FCA regulation. These responsibilities exist to protect you throughout the loan process.

- Conduct a suitability assessment. The broker must verify that a secured loan is appropriate for your needs, not just affordable. This includes reviewing your financial position, your reasons for borrowing, and whether alternative products might serve you better.

- Provide personalised cost illustrations. Before any recommendation is made, the broker must present a full illustration of costs, including interest, fees, and the total amount repayable over the loan term.

- Disclose all fees and commissions. Every fee the broker receives, whether from you or from a lender, must be disclosed in writing before the application proceeds.

- Act in your best interest. The broker’s advice must prioritise your financial wellbeing. This duty applies regardless of which lender offers the highest commission.

- Manage third-party costs transparently. Costs such as valuation fees and legal fees must be clearly explained. If any fees are refundable in certain circumstances, the broker must clarify that upfront.

- Maintain clear communication. FCA regulations require brokers to keep you informed at every stage of the application. You should never be left wondering what is happening with your case.

These responsibilities are not optional. Brokers who fail to meet them risk losing their FCA authorisation. That regulatory framework is what separates a qualified secured loan broker from an unregulated introducer.

Key takeaways

A secured loan broker is a regulated professional whose value lies in matching your financial profile to the right lender, protecting your credit file, and managing the application process from assessment to completion.

| Point | Details |

|---|---|

| Broker role | Acts as an FCA-regulated intermediary between borrower and lender, assessing suitability and managing the full application. |

| Credit protection | Soft search technology prevents hard credit inquiries during eligibility checks, preserving your borrowing power. |

| Fee transparency | All broker fees and lender commissions must be disclosed in writing before any recommendation is made. |

| Broker independence | Panel breadth, not fee model, determines how independent a broker’s advice truly is. |

| Specialist access | Many lenders only accept applications via brokers, making broker involvement essential for non-standard cases. |

Why I think most borrowers underestimate what a broker actually does

People tend to think of a secured loan broker as someone who searches a comparison site on your behalf and takes a cut. That view misses the most important part of the job.

The real value is in active case management. When I look at the cases where borrowers have struggled, the common thread is not the rate they were offered. It is the process falling apart after the application was submitted. A valuation comes back lower than expected. A solicitor misses a deadline. A lender requests additional documents and nobody chases the response. Without a broker coordinating those moving parts, applications stall, and borrowers end up paying more or missing their window entirely.

Whole-of-market access matters too, but not for the reason most people assume. It is not just about having more options. It is about having access to lenders who do not appear on any public comparison tool. Specialist lenders who work exclusively through brokers often offer products that are genuinely better suited to complex borrower profiles. If you go direct, you never see those products.

The other thing I would highlight is the credit file protection angle. Most borrowers do not realise that applying directly to multiple lenders, even just to compare offers, can leave a trail of hard searches on their credit file. A broker filters that process before a single hard search is triggered. That is not a minor administrative detail. It can affect your ability to borrow for months afterwards.

— Paul

How Prosperhomeloans connects you with the right broker

Working with a qualified secured loan broker makes a measurable difference to the outcome of your application. Prosperhomeloans connects you with FCA-regulated, whole-of-market brokers who assess your circumstances thoroughly and present options suited to your financial profile.

Every broker we work with is required to disclose fees transparently, conduct full suitability assessments, and manage your case actively from initial enquiry through to completion. Whether you are looking at debt consolidation, home improvements, or a more complex borrowing need, Prosperhomeloans gives you access to advisers who understand the secured loan market and know how to get applications across the line efficiently. You get clear advice, no unnecessary delays, and a broker who works in your interest throughout.

FAQ

What is a secured loan broker?

A secured loan broker is an FCA-regulated professional who acts as an intermediary between borrowers and lenders, assessing suitability and managing the secured loan application process on your behalf.

Do I have to pay a fee to use a secured loan broker?

Not always. Some brokers operate on a commission-only basis, meaning the lender pays them directly with no upfront cost to you. Fee-charging brokers typically charge between £500 and £1,500 or a percentage of the loan amount, and all fees must be disclosed before any recommendation is made.

Can a broker access lenders I cannot apply to directly?

Yes. Many specialist secured loan lenders only accept applications through FCA-authorised brokers, particularly for self-employed borrowers or non-standard properties. Without a broker, those products are not accessible to you.

Will using a broker affect my credit score?

Using a broker protects your credit score during the eligibility stage. Brokers use soft search technology to check your suitability with lenders without triggering hard credit searches, which means your credit file remains unaffected until a formal application is submitted.

How do I know if a secured loan broker is giving independent advice?

Check the breadth of their lender panel. A whole-of-market broker with access to a wide range of lenders provides more genuinely independent advice than one tied to a limited panel, regardless of their fee model.