New build London contractor mortgage process explained

The new build London contractor mortgage process is a structured sequence of stages that takes you from initial reservation through to receiving your keys. As a contractor or construction professional, you face a different set of lending criteria compared to salaried employees, and understanding those differences early saves you significant time and stress. The process typically spans 8–16 weeks for conveyancing alone, with additional stages before and after. At Prosperhomeloans, we work with contractors every day to cut through the complexity and secure the right deal efficiently.

What documents and prerequisites do contractors need for a new build mortgage in London?

Preparation is the single biggest factor separating successful contractor mortgage applications from rejected ones. Lenders assess your application differently from a standard employed applicant, so arriving with the right paperwork from the outset is non-negotiable.

Contractor-friendly lenders assess income based on your contract day rate rather than self-assessment tax returns. This is a significant advantage if your tax returns show lower net profit due to legitimate business expenses. However, it means you must present your contract documentation clearly and completely.

The core documents you need to gather include:

- Current contract: Your active contract, showing your day rate and end date. Lenders typically require at least 3–6 months remaining on the contract at the point of application.

- Contract history: Evidence of consistent contract renewals over a minimum of 12 months. Gaps between contracts raise red flags with underwriters.

- IR35 Status Determination Statement (SDS): Lenders use this document to assess your tax position and lending risk. Without it, many automated underwriting systems will flag your application immediately.

- Bank statements: Typically three to six months of personal and business account statements showing income receipt.

- Proof of identity and address: Passport, driving licence, and recent utility bills or council tax statements.

- SA302 forms or tax year overviews: Some lenders still request these alongside contract evidence, particularly for applications spanning more than one tax year.

Pro Tip: Obtain your IR35 SDS from your end client or agency before you begin the application. Proactive provision of IR35 documentation, combined with at least 12 months of consistent contract renewals, materially improves your mortgage success rate.

Contractors working in IT, engineering, and construction benefit from lender familiarity with these sectors. Lenders recognise that contract work in these fields carries lower income volatility than other freelance professions, which can positively influence their lending decision.

How does the new build mortgage application process work, step by step?

The mortgage journey for a new build property follows a clear sequence. Each stage has a defined purpose and approximate duration. Missing a step or misunderstanding the order can cause costly delays.

-

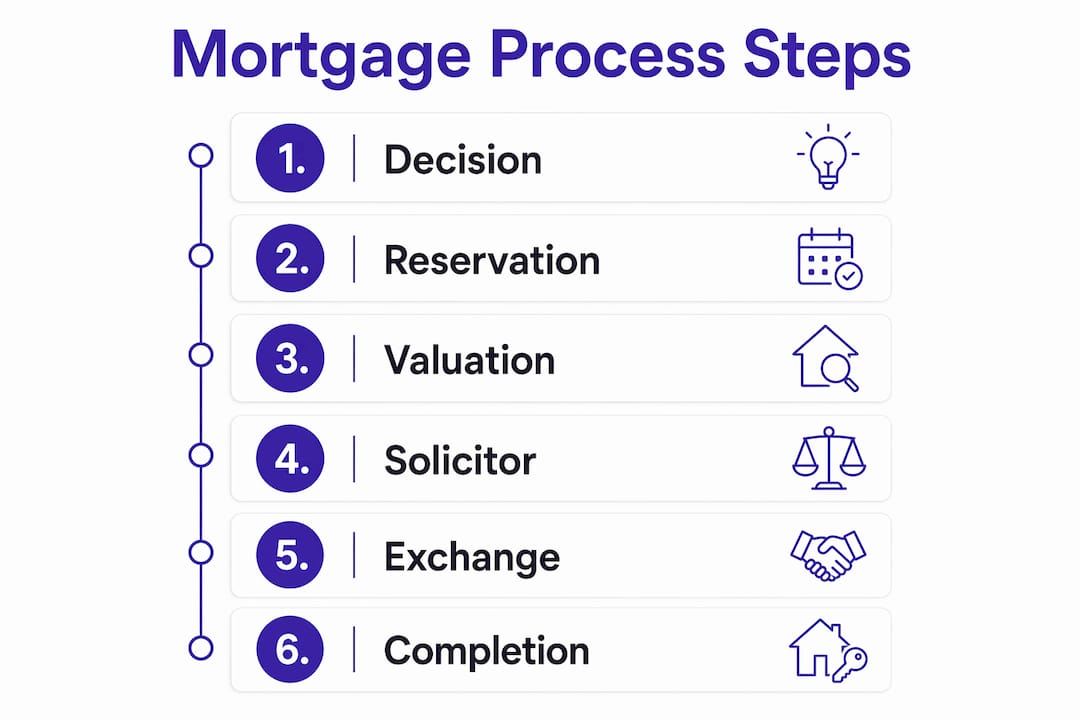

Decision in Principle (DIP). Before you reserve a property, obtain a DIP from a lender or through a broker like Prosperhomeloans. A DIP confirms the lender’s indicative willingness to lend based on a soft credit check. This stage takes 24–48 hours and gives you credibility with the developer.

-

Reservation and reservation fee. Once you identify your new build property, you pay a reservation fee of £500–£2,000 to the developer. This secures the property off-market while you arrange your mortgage and instruct a solicitor. The reservation period is commonly 28 days.

-

Full mortgage application. Submit your complete application with all supporting documents. Your broker coordinates this with the lender’s underwriting team. Expect this stage to take 1–3 weeks depending on lender workload and document completeness.

-

Mortgage valuation survey. The lender instructs a surveyor to value the new build property. A mortgage valuation survey typically takes 1–3 weeks and confirms the property’s value relative to the purchase price. If the valuation comes in below the agreed price, the lender may reduce the loan amount.

-

Formal mortgage offer. Once the valuation is satisfactory and underwriting is complete, the lender issues a formal mortgage offer. Mortgage offers are valid for six months, which is the critical window within which completion must occur.

-

Conveyancing. Your solicitor works in parallel with the mortgage process to carry out legal checks, review the developer’s contract, and prepare for exchange. New build conveyancing takes 8–16 weeks due to the complexity of off-plan legal documentation.

-

Exchange of contracts. You exchange contracts with the developer, typically within a 28-day window after reservation. At this point, you pay your deposit, usually around 10% of the purchase price, and become legally committed to the purchase.

-

Completion. Completion occurs when the build finishes and the developer notifies your solicitor. Completion takes place 1–4 weeks after exchange, at which point mortgage funds are released and you receive your keys.

| Stage | Approximate duration | Key action |

|---|---|---|

| Decision in Principle | 24–48 hours | Soft credit check; confirms indicative lending |

| Reservation | Day 1 | Pay £500–£2,000 fee; instruct solicitor |

| Full application | 1–3 weeks | Submit all contractor documents |

| Valuation survey | 1–3 weeks | Lender confirms property value |

| Formal mortgage offer | Issued after valuation | Valid for six months from issue date |

| Conveyancing | 8–16 weeks | Legal checks; contract review |

| Exchange | Within 28-day window | Pay 10% deposit; legally committed |

| Completion | 1–4 weeks post-exchange | Funds released; keys handed over |

Pro Tip: Instruct your solicitor on the same day you pay your reservation fee. Conveyancing for new builds takes longer than for existing homes, so starting immediately gives you the best chance of exchanging within the developer’s required window.

How do construction delays affect your mortgage timeline?

Build delays are the most common and least discussed risk in the new build mortgage process for contractors. Most buyers focus on the application itself and overlook what happens if the developer runs behind schedule.

The core problem is straightforward. Your mortgage offer validity of six months is fixed from the date of issue. If the build overruns and completion falls outside that window, your offer expires. You must then reapply, which may mean a new credit check, updated documents, and potentially a different interest rate if market conditions have shifted.

Contractors face a compounding risk here. If your current contract ends during the delay period and you take a short break before the next one, your income continuity evidence changes. A lender reviewing a reapplication may assess your situation less favourably than they did six months earlier.

Waiting for the developer to notify you of delays is often too late. By the time an official delay notice arrives, your options to protect the mortgage offer are already limited.

Practical steps to manage timing risk include:

- Negotiate a long-stop date in your purchase contract. This is a contractual deadline by which the developer must complete, or you can withdraw and recover your deposit.

- Monitor construction progress directly. Visit the site regularly or ask your solicitor to request progress updates from the developer’s legal team.

- Communicate with your lender early. Some lenders will extend a mortgage offer by up to two months if you notify them of a delay before the offer expires.

- Keep your contractor documents current. If reapplication becomes necessary, having up-to-date contracts and bank statements ready reduces turnaround time significantly.

Pro Tip: Ask your solicitor to include a long-stop date clause before you exchange contracts. Without it, you have no legal protection if the build runs months over schedule.

What challenges do contractors face and how can you overcome them?

Contractors encounter specific obstacles that salaried applicants do not face. Recognising these in advance lets you address them before they become problems.

| Common challenge | Practical solution |

|---|---|

| IR35 complexity confusing underwriters | Provide a formal SDS and a written summary of your working arrangements |

| Income variability between contracts | Show 12+ months of consistent contract renewals and a strong day rate |

| Short remaining contract term at application | Renew or extend your contract before submitting the full application |

| Automated rejection by high-street lenders | Use a specialist broker to access contractor-friendly lenders directly |

| Conveyancing delays causing exchange to slip | Instruct an experienced new build solicitor on day one of reservation |

The IR35 issue deserves particular attention. Proactive IR35 documentation prevents automated rejections that are common in standard high-street mortgage algorithms. Many lenders use automated systems that flag contractor applications without clear employment status evidence. A formal SDS bypasses this problem before it starts.

Income variability is the second major concern. Lenders want to see that your earnings are consistent and that your sector supports ongoing demand for your skills. A strong history of contract renewals in construction, engineering, or IT demonstrates exactly that. If you have had a gap between contracts in the past 12 months, be prepared to explain it clearly and in writing.

Pro Tip: If a high-street lender declines your application, do not reapply immediately. Each hard credit search affects your credit score. Work with a specialist broker to identify the right lender before submitting again.

Key takeaways

The new build London contractor mortgage process requires careful preparation of IR35 documentation, active timeline management, and access to contractor-friendly lenders to succeed.

| Point | Details |

|---|---|

| IR35 documentation is non-negotiable | Provide a formal Status Determination Statement before applying to avoid automated rejections. |

| Mortgage offers last six months | Align your application timing with the developer’s build schedule to avoid costly reapplication. |

| Conveyancing takes 8–16 weeks | Instruct a new build solicitor on reservation day to meet the 28-day exchange window. |

| Lenders assess contract day rates | Present current contracts and 12 months of renewals rather than relying on tax returns alone. |

| Long-stop dates protect your deposit | Negotiate this clause before exchange to retain legal protection against build overruns. |

What I have learned advising London contractors on new build mortgages

After years of working with contractors buying new build properties across London, the pattern I see most often is this: the application itself is rarely the problem. The problem is timing.

Contractors tend to be thorough with their documents because they are used to managing contracts professionally. What catches them out is the gap between when the mortgage offer is issued and when the build actually completes. Six months sounds like a long time. On a new build in London, it frequently is not.

The developers I have seen cause the most delays are those working on large mixed-use schemes where the residential element depends on commercial or infrastructure milestones outside their direct control. If you are buying on one of these developments, build in extra time and push your solicitor to negotiate a long-stop date before you exchange.

The other lesson I keep coming back to is lender selection. Not every lender understands contractor income, and applying to the wrong one wastes weeks. A specialist broker who works with contractors daily will know which lenders are currently processing contractor applications efficiently and which are creating underwriting delays. That knowledge alone can save you a month on your timeline.

My honest advice: treat the mortgage process as a project with a critical path, the same way you would manage a construction programme. Identify the dependencies, assign responsibility, and monitor progress. The contractors who do this consistently complete on time and on budget.

— Paul

How Prosperhomeloans supports London contractors with new build mortgages

Securing a mortgage as a contractor buying a new build property in London requires specialist knowledge that most general mortgage advisors simply do not have.

Prosperhomeloans works specifically with contractors and construction professionals to find the right lender, prepare the right documentation, and manage the timeline from DIP to completion. We understand how lenders assess contract day rates, IR35 status, and income continuity, and we use that knowledge to position your application correctly from the outset. If you are ready to move forward, speak to our team about contractor mortgage options tailored to your situation. We make the process straightforward, saving you time and reducing the stress of finding the right deal.

FAQ

What is the new build London contractor mortgage process?

The new build London contractor mortgage process is the sequence of stages from Decision in Principle through reservation, valuation, conveyancing, exchange, and completion. Contractors follow the same stages as other buyers but must meet additional income and IR35 documentation requirements.

How do lenders assess contractor income for a new build mortgage?

Contractor-friendly lenders assess income based on your contract day rate rather than self-assessment tax returns. They typically require evidence of a current contract with 3–6 months remaining and at least 12 months of consistent contract renewals.

How long does a new build mortgage offer last?

A mortgage offer is valid for six months from the date of issue. If the build is delayed beyond this period, you may need to reapply, which can result in a new credit check and potentially different lending terms.

What is an IR35 Status Determination Statement and why does it matter?

An IR35 Status Determination Statement is a formal document confirming whether your contract falls inside or outside IR35 tax rules. Lenders use it to assess your employment status and lending risk, and providing one proactively reduces the risk of automated rejection.

What reservation fee should I expect to pay on a new build in London?

Reservation fees on new build properties typically range from £500 to £2,000. This fee secures the property off-market for a limited period, commonly 28 days, while you arrange your mortgage and instruct a solicitor.