Mortgage affordability for subcontractors: 2026 guide

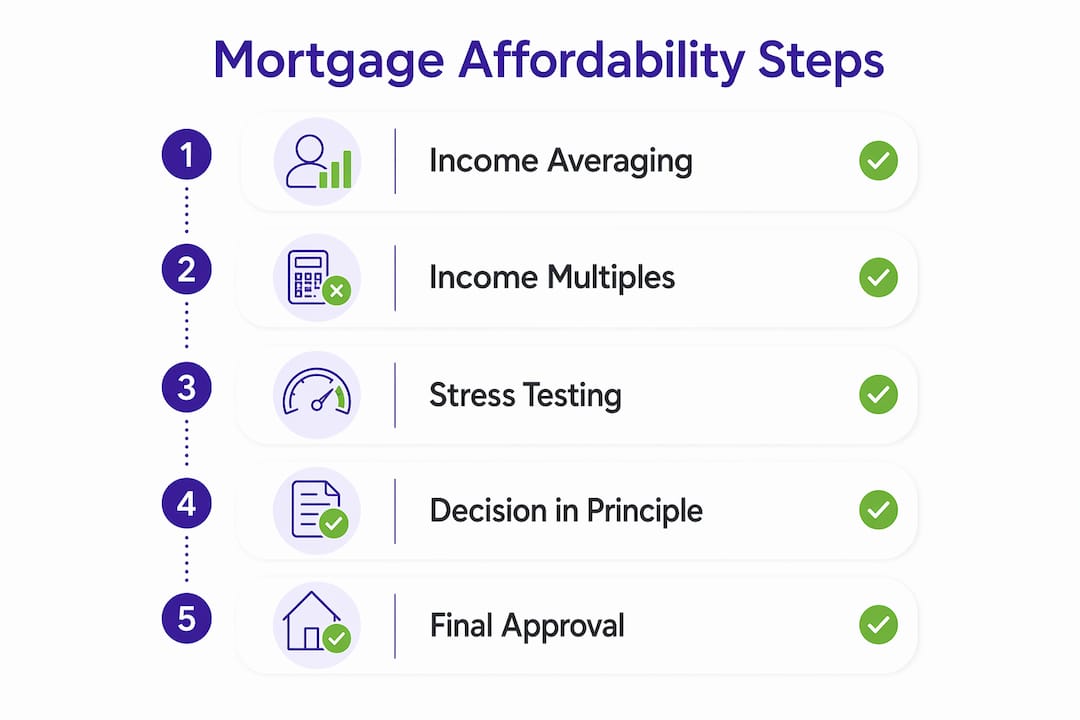

Mortgage affordability for subcontractors is defined as the maximum amount a lender will permit you to borrow, calculated using your averaged income, committed outgoings, and a stress-tested repayment figure. Unlike employed borrowers with payslips, subcontractors in the UK construction industry face a more detailed assessment because income varies month to month. Lenders typically average income over 2 to 3 years to establish a reliable earnings figure, then apply income multiples of 4 to 4.5 times that annual amount. Your CIS payment and deduction statements, SA302 tax returns, and bank statements are the core documents that drive every affordability decision.

How do lenders assess mortgage affordability for subcontractor income?

Lenders do not simply take your most recent year’s earnings and multiply them. They want confidence that you can service the mortgage during quieter months, which is why multi-year income averages are the standard approach. A subcontractor earning £45,000 in year one, £38,000 in year two, and £42,000 in year three would typically have their affordability calculated on an average of roughly £41,667, not the peak figure.

Once the lender has your average income, they apply an income multiple. Most high-street lenders use 4x to 4.5x annual earnings as their ceiling. A clean credit history and a larger deposit can push some lenders toward the higher end of that range, though multiples above 4.5x remain uncommon and require specific criteria to be met.

Affordability stress testing is the part most subcontractors overlook. Lenders stress-test repayments at rates of 7.0% to 8.5%, regardless of the actual deal rate you are offered. This means that even if your mortgage rate is 4.5%, the lender calculates whether you could afford payments at nearly double that. The practical effect is that your borrowing capacity is lower than the headline income multiple suggests.

Outgoings matter as much as income. Lenders factor in committed debts and costs such as car finance, personal loans, credit card balances, and childcare before arriving at a net affordability figure. A subcontractor earning £42,000 per year but carrying £600 per month in existing debt commitments will borrow considerably less than a colleague on the same income with no debts.

Key factors lenders weigh during mortgage affordability checks for subcontractors:

- Income averaging: 2 to 3 years of accounts or CIS records, smoothed to a reliable annual figure

- Income multiples: typically 4x to 4.5x, adjusted for deposit size and credit profile

- Stress testing: repayments calculated at 7.0% to 8.5% test rates

- Committed outgoings: all regular debt payments deducted before the affordability calculation

- Deposit size: a larger deposit reduces the loan-to-value ratio and can unlock better products

Pro Tip: Request a Decision in Principle before you start viewing properties. It gives you a realistic borrowing figure based on your actual subcontractor income and prevents wasted time on properties outside your range.

What proof of income do subcontractors need for a mortgage?

Subcontractor proof of income for a mortgage application must be thorough, consistent, and correctly calculated. Lenders are looking for a clear paper trail that confirms both the amount you earn and the regularity with which you earn it. Incomplete or incorrectly prepared documents are one of the most common reasons subcontractor mortgage applications stall.

The documents you will need to prepare:

- CIS payment and deduction statements: These are official records issued by your contractor showing gross payments made and tax deducted at source. CIS statements are critical evidence of your income and tax position. They must include your name, Unique Taxpayer Reference, the contractor’s details, and the breakdown of gross payment, materials deduction, and CIS tax deducted.

- SA302 tax returns: Your self-assessment tax calculations for the last 2 to 3 years provide HMRC-verified income figures. Most lenders require these as the primary income record alongside your CIS statements.

- Bank statements: Three to six months of personal bank statements showing regular income deposits corroborate what your CIS records and SA302s declare. Lenders look for consistency between what is declared and what actually lands in your account.

- Contracts and invoices: Current or recent contracts with contractors demonstrate ongoing work and future income. Invoices support the income figures shown in your bank statements and CIS records.

- Accountant’s certificate: Some lenders, particularly those offering specialist subcontractor mortgage options, request a signed letter from a qualified accountant confirming your income and trading status.

A critical detail that catches many subcontractors out: CIS statements must exclude VAT from the gross payment figure, and the CIS deduction applies only to the labour element, not to materials costs. If your statements incorrectly include VAT or apply deductions to materials, your declared income will be wrong. Lenders and underwriters will spot the discrepancy, and it can trigger requests for additional evidence or, in some cases, a declined application.

“Organising tax returns, bank statements, contracts, and invoices efficiently helps subcontractors demonstrate income stability and enhances lender confidence.” — ForFinancialTips

Pro Tip: Keep a dedicated folder, physical or digital, updated quarterly with your latest CIS statements, bank statements, and any new contracts. When a mortgage application arises, you will have everything ready rather than scrambling to locate two-year-old documents.

How can subcontractors improve their mortgage affordability?

Improving your position before you apply is far more effective than trying to negotiate with a lender after a declined application. The steps below are practical and achievable for most subcontractors working in the UK construction sector.

- Increase your deposit. A deposit of 10% or more unlocks better mortgage rates and higher income multiples. Moving from a 5% to a 15% deposit can meaningfully change both the products available to you and the total amount you can borrow.

- Reduce existing debts. Paying off a car finance agreement or clearing a credit card before applying directly reduces your committed outgoings. This increases the net income figure lenders use in their affordability calculation.

- Maintain a clean credit history. Missed payments, defaults, or County Court Judgements restrict you to lenders with tighter criteria and lower multiples. Checking your credit file with Experian, Equifax, or TransUnion before applying gives you time to correct errors or address issues.

- Organise your income documentation. Lenders respond well to applications where the income trail is clear and consistent. Gaps, inconsistencies, or missing CIS statements create doubt and slow down underwriting.

- Consider a joint application. Joint mortgage applications combine incomes, and lenders apply the standard income multiples to the combined figure. If your partner or a family member has a stable employed income, a joint application can substantially increase your borrowing capacity.

- Work with a specialist broker. A broker with experience in mortgage scenario analysis for subcontractors knows which lenders are most receptive to CIS income and can match your profile to the right product from the outset.

Pro Tip: If your income has grown significantly in the last year, ask your broker whether any lenders will use your most recent year’s earnings rather than a straight average. Some lenders do offer this flexibility for applicants with a demonstrably upward income trend.

Common mistakes during mortgage affordability checks for subcontractors

Understanding where applications go wrong is just as useful as knowing what to do right. These are the errors we see most frequently when working with subcontractors on their mortgage applications.

- Relying on a single year of high earnings. Lenders focus on income stability across multiple years, not peak performance. Presenting only your best year without context raises questions rather than confidence.

- Incorrectly prepared CIS statements. Including VAT in the gross figure or applying CIS deductions to materials costs produces an inaccurate income declaration. This is one of the most common and most avoidable documentation errors.

- Underestimating the impact of stress testing. Many subcontractors calculate affordability based on current mortgage rates and are surprised when the lender’s figure comes back lower. The stress test at 7.0% to 8.5% is the real constraint, not the headline rate.

- Failing to account for all outgoings. Forgetting to include subscription services, hire purchase agreements, or informal financial commitments means your declared outgoings do not match your bank statements. Lenders cross-reference these figures.

- Missing CIS return deadlines. Late or missing CIS returns with HMRC can result in penalties and gaps in your official income record. Lenders reviewing your SA302s will see incomplete years, which undermines the income averaging process.

- Ignoring lender-specific criteria. Not all lenders assess subcontractor income the same way. Applying to a lender whose criteria does not accommodate CIS income without specialist guidance often results in a declined application that leaves a mark on your credit file.

“Lenders focus not just on high income years but confidence in servicing the mortgage during income dips, making multi-year averages critical for subcontractors.” — Rightmove

Reviewing the mortgage compliance requirements relevant to your application type before you submit can prevent the most common refusals. A specialist broker will walk through this with you in advance.

Key takeaways

Subcontractors secure mortgages by presenting averaged CIS income across 2 to 3 years, meeting stress-tested affordability thresholds, and providing complete, correctly calculated documentation.

| Point | Details |

|---|---|

| Income averaging is standard | Lenders use 2 to 3 years of CIS and SA302 records to calculate a reliable annual income figure. |

| Stress testing reduces borrowing capacity | Affordability is assessed at test rates of 7.0% to 8.5%, not the actual mortgage rate offered. |

| CIS statements must be accurate | VAT must be excluded and CIS deductions applied to labour only, not materials, to avoid errors. |

| Larger deposits improve your options | A deposit of 10% or more unlocks better rates and higher income multiples from more lenders. |

| Specialist brokers open more doors | Brokers experienced with subcontractor income know which lenders accept CIS evidence and how to present it. |

What I have learned from helping subcontractors get mortgages

After years of working with subcontractors across the UK construction industry, the pattern I see most often is this: the application does not fail because of the income. It fails because the income is not presented in a way lenders can easily verify.

The subcontractors who get the best outcomes are not necessarily the highest earners. They are the ones who have kept clean records, filed their CIS returns on time, and can produce two or three years of consistent documentation without gaps. A plasterer earning £38,000 consistently across three years will often get a better result than a groundworker who earned £55,000 last year but has patchy records before that.

What I tell every subcontractor we work with at Prosperhomeloans is this: start preparing your mortgage application at least six months before you intend to buy. Use that time to clear small debts, build your deposit, and get your CIS statements and SA302s in order. The lender’s underwriter is not trying to catch you out. They are trying to build confidence that you can manage repayments when work slows down in January or February. Your job is to give them that confidence through documentation, not just declarations.

The other thing worth saying plainly: not every lender is right for every subcontractor. High-street banks often apply rigid criteria that do not accommodate CIS income well. Specialist lenders and building societies frequently offer more flexible assessment methods. Knowing which lender to approach for your specific income profile is where a good broker earns their value.

— Paul

How Prosperhomeloans can help with your mortgage application

At Prosperhomeloans, we specialise in helping subcontractors and self-employed individuals get the mortgage they deserve, without the stress of navigating lender criteria alone. We know how CIS income is assessed, which lenders work well with construction industry applicants, and how to present your documentation in the strongest possible light.

Whether you are a first-time buyer or looking to remortgage, our advisors will review your income records, identify the most suitable lenders, and guide you through every step of the process. We take the complexity out of affordability checks so you can focus on finding the right property. Visit Prosperhomeloans to speak with an advisor who understands your situation and can find the right deal for you.

FAQ

How do lenders calculate mortgage affordability for subcontractors?

Lenders average your income over 2 to 3 years using CIS statements and SA302 tax returns, then apply income multiples of 4x to 4.5x. They also stress-test repayments at rates of 7.0% to 8.5% and deduct committed outgoings before arriving at a final borrowing figure.

What documents do I need as a subcontractor to prove income for a mortgage?

You will need CIS payment and deduction statements, SA302 self-assessment tax returns for 2 to 3 years, 3 to 6 months of bank statements, and copies of current contracts or invoices. Some lenders also request an accountant’s certificate confirming your income and trading status.

Can I get a mortgage as a subcontractor with irregular income?

Yes. Lenders assess subcontractor income by averaging earnings across multiple years rather than relying on a single figure. Consistent records, a clean credit history, and a deposit of at least 10% significantly improve your chances of approval.

Does a larger deposit improve mortgage affordability for subcontractors?

A deposit of 10% or more unlocks better mortgage rates and can increase the income multiples lenders are willing to apply. It also reduces the loan-to-value ratio, which lowers the lender’s risk and broadens the range of products available to you.

Why do subcontractor mortgage applications get declined?

The most common reasons are incomplete or incorrectly calculated CIS statements, relying on a single year of income rather than a multi-year average, and applying to lenders whose criteria does not accommodate CIS income. Working with a specialist broker reduces the risk of a declined application significantly.