London mortgage broker role explained for buyers

A London mortgage broker is a regulated intermediary who assesses your financial profile and matches you with suitable mortgage products from across the market. The broker’s role has expanded well beyond rate comparison. In London’s complex property market, a broker now acts as a strategic adviser who navigates lender policies, regulatory requirements, and your long-term financial goals. Understanding what a broker does, how they are paid, and how to choose the right one gives you a genuine advantage when securing a mortgage in one of the world’s most competitive cities.

What does the London mortgage broker role involve?

A mortgage broker is defined in industry practice as a professional who sits between you and the lender, working on your behalf to find the most suitable mortgage product for your circumstances. Brokers assess your financial profile, including your income, credit history, existing debts, and risk tolerance, before recommending products from a range of lenders. They are not tied to a single bank or building society, which means their recommendations reflect your needs rather than a lender’s sales targets.

Brokers are paid in one of three ways: lender commission, a fee charged directly to you, or a combination of both. Lender commission does not increase the cost of your mortgage. You are never obliged to proceed with a broker’s recommendation, which means you retain full control of the decision.

The role has evolved considerably. Mortgage brokers now guide clients through complex lender policies and help prevent application declines by preparing borrower profiles that meet specific lender criteria. In London, this includes navigating requirements such as EWS1 cladding forms for flats in high-rise buildings, high-value lending guidelines, and affordability assessments that vary significantly between lenders.

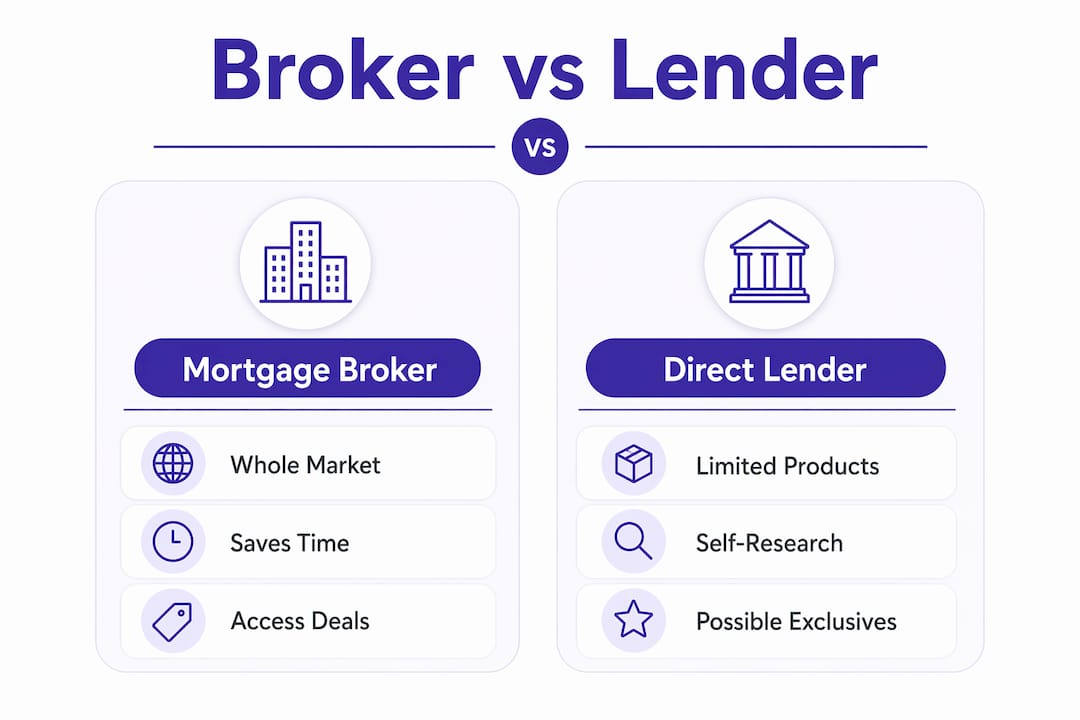

Broker vs lender: what is the difference?

Going directly to a lender limits you to that lender’s own product range. A broker gives you access to products from multiple lenders simultaneously, including exclusive deals not available on the high street. The practical difference is significant in London, where property prices mean that even a small difference in interest rate or product terms can translate into thousands of pounds over the life of a mortgage.

| Feature | Mortgage broker | Direct lender |

|---|---|---|

| Product access | Whole of market or multi-lender | Own products only |

| Time investment | Broker handles research and paperwork | You research and apply independently |

| Cost | Fee and/or lender commission | No broker fee |

| Exclusive deals | Often available | Rarely available |

| Personalised advice | Yes, regulated and tailored | Limited to product suitability |

| Application support | Full preparation and submission | Self-managed |

Brokers save borrowers time by handling lender research, application preparation, and communication on your behalf. The trade-off is that some brokers charge upfront fees. A whole-of-market broker, however, often secures a deal that more than offsets any fee through better rates or product terms.

Direct lenders do occasionally offer products that brokers cannot access. This is rare, but worth checking. The most reliable approach is to use a whole-of-market broker and ask them directly whether any lender exclusives exist outside their panel.

What services do London mortgage brokers provide?

London brokers provide a wider range of services than most borrowers expect. The core service is mortgage advice, but the practical support extends across the entire application process.

Key services include:

- Financial profile analysis. The broker reviews your income, credit score, outstanding debts, and employment status to establish what you can realistically borrow and from whom.

- Loan structure advice. Brokers factor in future income, life changes, and investment plans when recommending mortgage structures. A two-year fixed rate may suit one borrower; a tracker or longer fix may suit another.

- London-specific regulatory guidance. Brokers familiar with the London market understand EWS1 requirements for leasehold flats, Help to Buy equity loan redemptions, and the affordability stress tests applied by lenders to high-value properties.

- Access to exclusive products. Some lenders only distribute products through brokers. A whole-of-market broker can access these deals, which are not available if you apply directly.

- Application preparation. Brokers prepare and present borrower profiles tailored to each lender’s specific requirements, which materially improves the chance of first-application success.

- Protection advice. Many brokers, including those at Prosperhomeloans, also advise on life insurance, critical illness cover, and income protection alongside the mortgage itself.

Pro Tip: Ask any broker whether they are independent, tied, or multi-tied before you engage them. An independent broker accesses the whole market and acts solely in your interest. A tied broker is restricted to one lender’s products. A multi-tied broker works with a panel of lenders but not the full market.

How do London brokers help contractors and the flexible workforce?

Contractors face a specific challenge when applying for a mortgage. Most high-street lenders assess income using payslips and P60s. Contractors, who are often paid via limited companies, day rates, or CIS (Construction Industry Scheme) vouchers, do not fit this model. Many are declined or offered far less than their actual earnings justify.

Specialist brokers address this by assessing contractor income differently. The steps a good contractor mortgage broker follows are:

- Calculate annualised contract income. The broker takes your current day rate, multiplies it by the number of working days in a year, and presents this figure as your effective gross income. This is a widely accepted method with lenders who understand contractor finances.

- Identify lenders with contractor-friendly criteria. Not all lenders accept day-rate calculations. A specialist broker knows which lenders do and approaches them directly, avoiding unnecessary credit searches with unsuitable lenders.

- Prepare supporting documentation. This includes current contracts, evidence of contract history, and, where relevant, CIS vouchers or self-assessment tax returns.

- Present the application correctly. Specialist brokers bypass traditional underwriting by presenting contractor profiles in a format lenders accept, rather than forcing a contractor’s income into an employee template.

The result is that contractors often secure mortgage offers that reflect their real earnings rather than a conservative estimate based on limited company salary alone.

Pro Tip: When interviewing a broker as a contractor, ask specifically: “Which lenders on your panel accept day-rate income calculations?” If the broker cannot name at least three lenders with clear contractor criteria, they may not have the specialist knowledge you need.

How to choose the right mortgage broker in London

Choosing a broker in London requires more care than in most other UK cities. The market is larger, property values are higher, and the regulatory environment is more complex. The wrong broker can cost you time, money, and a mortgage offer.

Independent, tied, or multi-tied?

The most important distinction is between independent and tied brokers. An independent broker searches the whole market. A tied broker is restricted to one lender. A multi-tied broker works with a selected panel. For most borrowers in London, an independent whole-of-market broker delivers the best outcome because they are not constrained by commercial agreements with specific lenders.

FCA authorisation and credentials

Every mortgage broker operating in the UK must be authorised by the Financial Conduct Authority (FCA). Verify broker credentials on the FCA register before you engage anyone. This takes two minutes and confirms the broker is legally permitted to give mortgage advice. Brokers who are not FCA authorised cannot legally advise you on regulated mortgage products.

Questions to ask before you commit

- Are you independent, tied, or multi-tied?

- How many lenders are on your panel?

- Do you charge a fee, and if so, when is it payable?

- Have you arranged mortgages for borrowers with my employment type before?

- How do you handle cases where the first application is declined?

Red flags to avoid

- Brokers who cannot explain their fee structure clearly

- Brokers who recommend a product without reviewing your full financial profile

- Any adviser who is not on the FCA register

- Brokers who pressure you to proceed quickly without giving you time to review the recommendation

Pro Tip: Use the mortgage broker platform comparison tools available online to cross-check whether the products your broker recommends are genuinely competitive. A good broker will welcome this scrutiny.

Key takeaways

A London mortgage broker is a regulated adviser who accesses the whole market on your behalf, prepares your application to lender standards, and provides strategic advice that goes well beyond finding the lowest rate.

| Point | Details |

|---|---|

| Broker vs lender access | Brokers access multiple lenders and exclusive deals; direct lenders offer only their own products. |

| Payment structure | Brokers earn commission from lenders, charge client fees, or both; commission does not raise your mortgage cost. |

| Contractor support | Specialist brokers calculate day-rate income correctly and identify lenders with contractor-friendly criteria. |

| FCA authorisation | Always verify a broker’s FCA registration before engaging; unregistered advisers cannot legally advise you. |

| Independent vs tied | An independent whole-of-market broker acts solely in your interest; tied brokers are limited to one lender’s range. |

What I have learned about brokers after years in the London market

The London mortgage market has changed more in the past five years than in the previous fifteen. When I started advising clients, the conversation was almost always about rate. Borrowers wanted the lowest number on the page. That instinct is understandable, but it misses the point.

The rate is one variable. The lender’s criteria, the product’s flexibility, the early repayment charges, the overpayment allowances, and the lender’s appetite for your specific employment type all matter just as much. I have seen clients secure a mortgage at a slightly higher rate that saved them thousands because the product had no early repayment charges and they sold within three years.

The shift toward strategic advice is real. Borrowers who engage a broker early, before they have found a property, are in a materially stronger position. They know their borrowing capacity, they understand which lenders suit their profile, and they can move quickly when the right property appears. In London, where competitive offers are common, that speed is worth more than most people realise.

My honest view is that the independent whole-of-market broker model is the only one worth using in London. Tied brokers serve a purpose, but the restrictions on their product access are a genuine limitation in a market this complex. If a broker cannot tell you clearly and immediately whether they are independent, walk away.

— Paul

How Prosperhomeloans supports London borrowers

Prosperhomeloans is an independent mortgage and protection advisory service built for borrowers who want expert guidance without the stress of navigating the market alone.

Whether you are buying your first home, remortgaging, or dealing with a complex case such as contractor income or a leasehold flat, Prosperhomeloans works across the whole market to find the right solution. The team handles the research, the paperwork, and the lender communication on your behalf. For contractors and the self-employed, Prosperhomeloans has specific experience presenting income in the format lenders accept, which materially improves application outcomes. To find out what is available for your circumstances, speak to the team at Prosperhomeloans and get clear, honest advice from the start.

FAQ

What does a mortgage broker do in London?

A London mortgage broker assesses your financial profile and searches multiple lenders to find the most suitable mortgage product for your circumstances. They handle application preparation, lender communication, and regulatory guidance throughout the process.

Is a mortgage broker regulated in the UK?

Every mortgage broker in the UK must be authorised by the Financial Conduct Authority. You can verify any broker’s registration on the FCA register before engaging their services.

Do mortgage brokers charge fees?

Some brokers charge upfront or completion fees; others are paid solely by lender commission. Lender commission does not increase your mortgage cost, and brokers must disclose all fees before you proceed.

Can a mortgage broker help if I am a contractor?

Yes. Specialist brokers assess contractor income using day-rate calculations rather than payslips, and they identify lenders with criteria suited to flexible working arrangements. This approach often results in a higher mortgage offer than a direct application would achieve.

What is the difference between an independent and a tied broker?

An independent broker searches the whole mortgage market and acts solely in your interest. A tied broker is restricted to the products of one lender, which limits the options available to you.