How long trading before mortgage: UK self-employed guide

Two years of trading accounts is the standard benchmark for self-employed mortgage applicants in the UK. Most high street lenders will not consider your application without at least two years of finalised accounts, though specialist lenders can sometimes accept one year if your financial profile is strong. Knowing how long trading before mortgage applications become viable gives you a clear target to plan towards. The good news is that understanding lender requirements early puts you in a far stronger position when the time comes to apply.

What do lenders require for trading history?

Most lenders set two years of trading as the minimum for a self-employed mortgage application. This applies whether you are a sole trader, a partnership, or a limited company director. The two-year rule exists because lenders want to see a pattern of income, not just a single good year.

Documentation requirements are specific and non-negotiable. You will typically need to provide:

- Two to three years of SA302 tax calculations from HMRC, or your tax year overviews

- Finalised company accounts, prepared by a qualified accountant and no older than 18 months at the point of application

- At least three months of business bank statements

- Personal bank statements covering the same period

Draft accounts are routinely rejected. Lenders treat draft figures as unverified, and submitting them can delay or kill an application outright.

Income assessment also differs depending on your trading structure. Sole traders are assessed on net profit. Limited company directors are typically assessed on salary plus dividends by high street lenders, averaged over a two to three year period. Specialist lenders may instead use net profit share, which can significantly increase your borrowing power.

Pro Tip: Ask your accountant to prepare your SA302 documents and finalised accounts at the same time each year. Keeping these current means you are always application-ready, rather than scrambling when you find a property.

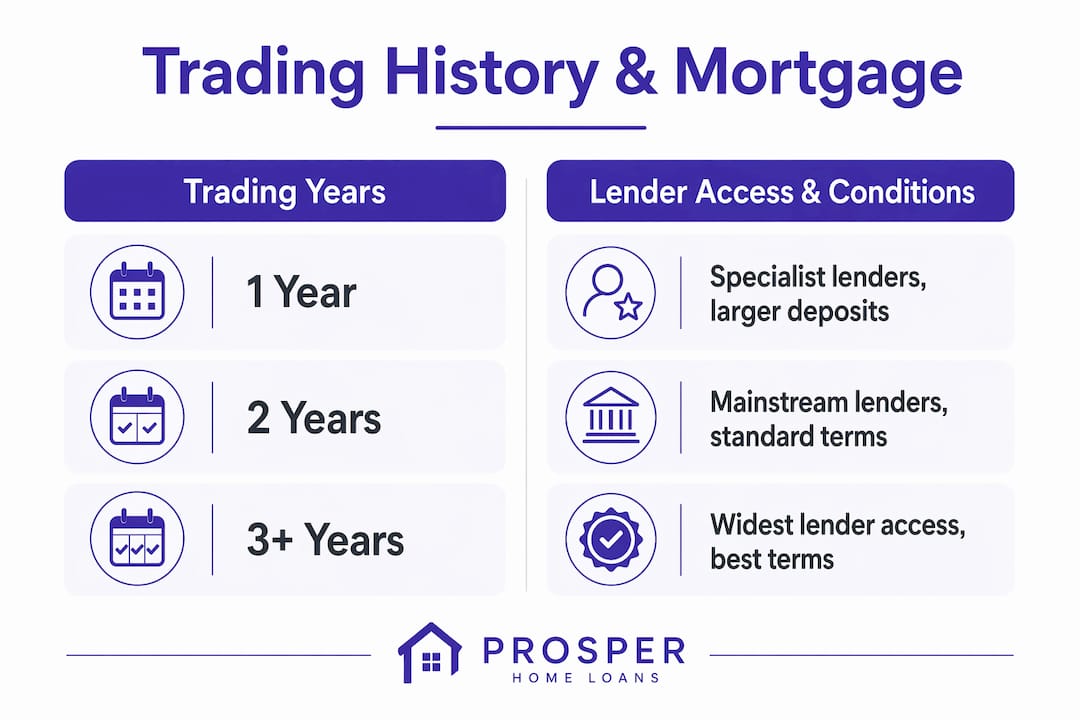

How does trading history length affect your mortgage options?

The number of years you have been trading directly shapes which lenders will consider you and on what terms. The difference between one, two, and three or more years of accounts is significant.

| Trading history | Lender access | Typical conditions |

|---|---|---|

| 1 year | Specialist lenders only | Larger deposit often required; higher rates likely |

| 2 years | Most high street and specialist lenders | Standard products available; rates competitive |

| 3+ years | Widest range of lenders | Best rates; strongest negotiating position |

Borrowers with three or more years of accounts access the widest range of mortgage products. Lenders can assess income trends across multiple years, which gives them confidence in the sustainability of your earnings.

Two years is considered the standard preferred position. At this point, most mainstream lenders will consider your application, and you will have access to competitive rates without needing to rely on specialist products.

One year of trading is the most restrictive position. Specialist lenders can accept applications at this stage, but you may face a larger deposit requirement and a narrower product range. A strong financial profile, such as significant assets or a clean credit history, improves your chances considerably.

Why income stability matters as much as trading length

Lenders prioritise evidence of income stability over the length of your trading history alone. A borrower with two years of consistent, growing income is viewed more favourably than one with three years of erratic earnings. This is the part many self-employed applicants overlook.

Income fluctuations do not automatically disqualify you, but they require explanation. If your earnings dropped significantly in one year, a lender will want to understand why. A well-prepared accountant can help you contextualise this within your accounts.

Key factors lenders examine for income stability include:

- Consistent or growing net profit across the trading period

- No unexplained large withdrawals or deposits in business accounts

- Salary and dividend patterns that are sustainable, not artificially inflated before application

- Accounts prepared by a qualified, regulated accountant

Planning salary and dividend patterns 12–24 months before you intend to apply is one of the most effective things a limited company director can do. Lenders want to see sustained income, not a sudden spike in the months before application.

Pro Tip: If your income fluctuates seasonally, keep a brief written record of the reasons. A letter from your accountant explaining a quiet period carries real weight during underwriting.

Can prior employment count towards your trading history?

Previous connected employment in the same industry can sometimes count towards the two-year trading requirement. This is one of the most underused advantages available to self-employed applicants, particularly limited company directors who moved from employment into running their own business in the same field.

The logic is straightforward. A structural engineer who spent ten years employed before setting up their own consultancy is not a financial unknown. Their industry experience and income track record reduce the lender’s perceived risk. Some lenders will factor this in when assessing how long you need to have been trading before a mortgage application becomes viable.

Here is how prior history can work in your favour:

- Same industry continuity. If you moved from employment to self-employment in the same sector, document this clearly. A CV or employment reference alongside your trading accounts strengthens the case.

- Prior limited company involvement. If you were a director or shareholder in a related business before your current company, some lenders will consider that history.

- Contractor to director transitions. Contractors who move to a limited company structure often retain credit history and income records that support an earlier application.

- Specialist lender criteria. Not all lenders apply the same rules. A specialist lender familiar with self-employed applicants is more likely to consider prior industry experience as part of the overall assessment.

The key is presenting this history clearly and consistently. A specialist mortgage adviser can identify which lenders are most likely to take a flexible view of your background.

Practical steps to prepare for your mortgage application

Starting your preparation 12–24 months before you plan to apply gives you the best chance of a successful outcome. This timeline allows you to address any gaps in your documentation, stabilise your income records, and clean up your finances before a lender scrutinises them.

The most important steps to take are:

- Get your accounts finalised promptly each year. Lenders require accounts no older than 18 months. Delays in filing mean your most recent year may not count.

- Hire a qualified accountant. Engaging a qualified accountant early improves the quality and timeliness of your accounts. Lenders take professionally prepared accounts more seriously than self-filed figures.

- Maintain consistent bank activity. Consistent deposits and withdrawals in your business account create a predictable income pattern. Erratic transactions raise concerns during underwriting.

- Check your credit file. Register on the electoral roll, pay all bills on time, and resolve any outstanding defaults at least six months before applying.

- Avoid large, unexplained transfers. Moving significant sums between accounts without a clear paper trail can trigger questions from underwriters.

You can review the self-employed criteria that lenders typically apply to understand exactly what documentation you need to prepare.

Pro Tip: Do not wait until you have found a property to start gathering documents. Mortgage applications for self-employed borrowers take longer to process. Having everything ready in advance puts you in a much stronger negotiating position.

Key takeaways

Self-employed mortgage applicants in the UK need at least two years of finalised trading accounts to access mainstream lenders, with three or more years unlocking the widest product range and most competitive rates.

| Point | Details |

|---|---|

| Two-year benchmark | Most lenders require two years of finalised accounts as the minimum for self-employed applications. |

| One year is possible | Specialist lenders may accept one year of trading with a strong financial profile and larger deposit. |

| Income stability counts | Consistent or growing earnings matter as much as trading length when lenders assess risk. |

| Prior employment helps | Connected industry experience before self-employment can sometimes satisfy trading history requirements. |

| Prepare 12–24 months early | Start organising accounts, bank records, and credit history well before you intend to apply. |

What I have learned about trading history and mortgage approval

The question I hear most often from self-employed clients is not “will I qualify?” but “when will I qualify?” Those are very different questions, and the answer to the second one is almost always: earlier than you think, if you plan properly.

The biggest mistake I see is applicants who focus entirely on hitting the two-year mark, then discover their accounts are not finalised, their income pattern looks erratic, or their credit file has an old default sitting on it. The trading period is just one piece of the picture. Lenders are underwriting your future ability to repay, not just counting years.

What actually moves the needle is income quality. A client with two years of clean, consistent accounts and a well-prepared application will outperform someone with four years of messy, fluctuating figures every time. The trading period gives lenders the data they need. What you do with that data, how you present it, and how you have managed your finances during that time, is what determines the outcome.

My advice is always the same: start talking to a specialist adviser at least a year before you want to apply. Not to apply early, but to understand exactly what your accounts need to show and to give yourself time to fix anything that could cause a problem.

— Paul

How Prosperhomeloans supports self-employed mortgage applicants

Self-employed mortgage applications are more complex than standard ones, but the right advice makes the process straightforward.

Prosperhomeloans works with a wide panel of lenders, including specialists who understand self-employed income structures and flexible trading history criteria. Whether you have one year of accounts or five, we assess your full financial picture and match you with the lender most likely to say yes on the best available terms. We also help you prepare your documentation correctly from the start, reducing delays and avoiding the common mistakes that hold applications back. If you are ready to take the next step, speak to our team and get clear, personalised advice on your mortgage options.

FAQ

How long do you need to be self-employed before getting a mortgage?

Most lenders require two years of trading history for a self-employed mortgage application. Some specialist lenders will consider one year if you have a strong financial profile, significant assets, or relevant prior industry experience.

What documents do self-employed applicants need for a mortgage?

You will typically need two to three years of SA302 tax calculations, finalised company accounts no older than 18 months, and at least three months of business bank statements. Draft accounts are not accepted by most lenders.

Does prior employment count towards self-employed mortgage eligibility?

Connected employment in the same industry before becoming self-employed can sometimes count towards the trading history requirement. This is assessed case by case and is more likely to be considered by specialist lenders.

Can I get a mortgage with only one year of self-employment?

Yes, but your options are limited. Specialist lenders may accept one year of trading, often requiring a larger deposit and charging higher rates. A strong credit history and consistent income improve your chances significantly.

How does income stability affect a self-employed mortgage application?

Lenders prioritise consistent or growing income over trading length alone. Erratic earnings or unexplained income drops can raise concerns during underwriting, even if you meet the minimum trading period requirement.