Foreign national mortgage broker role explained

A foreign national mortgage broker is a specialist intermediary who helps non-UK residents and overseas nationals secure mortgage financing in the UK property market. Unlike a standard mortgage adviser, this specialist understands the layered complexity of immigration status, foreign income verification, and lender underwriting rules that apply specifically to non-resident buyers. The foreign national mortgage broker role explained simply is this: they translate your financial profile into a format UK lenders will accept, then match you to the right product. Without this expertise, many foreign nationals face automatic rejections from mainstream banks, even when they are financially strong candidates. At Prosperhomeloans, we work with clients in exactly this position every week.

How mortgage brokers help foreign nationals navigate UK mortgage eligibility

Foreign nationals face a set of eligibility hurdles that simply do not exist for UK citizens, and understanding those hurdles is the starting point for any good broker. Immigration status directly shapes what lenders will offer you, how large a deposit you need, and whether mainstream or specialist lenders are even an option.

The differences are significant:

- Indefinite Leave to Remain (ILR) or settled status holders can access the mainstream mortgage market, with loan-to-value ratios up to 95% in some cases.

- Skilled worker visa holders typically require specialist lenders and deposits of between 10% and 25%.

- Family visa holders face similar restrictions, with some mainstream lenders declining applications outright regardless of income.

- Non-resident foreign nationals purchasing UK property from abroad face the most restrictive conditions, often requiring deposits of 25 to 40% from lenders such as Halifax, Skipton, and Hodge.

A specialist broker’s first task is to assess your immigration status accurately and map it to the correct lender tier. General brokers rarely have access to the specialist lender panels that serve visa holders or non-residents. A foreign national mortgage broker comparison UK would quickly reveal that specialist advisers hold relationships with lenders that simply do not appear on high-street comparison sites.

The broker then works through your income profile. If you earn in a foreign currency, receive income from multiple countries, or are employed by an overseas company, your application requires specific positioning before it reaches an underwriter. Getting this wrong at the outset is the most common reason foreign national applications are declined.

Pro Tip: Before you approach any lender or broker, gather your current visa documentation, the last three months of payslips, and your most recent two years of tax returns. Having these ready in their original language, plus certified translations, saves weeks at the application stage.

What qualifications should a foreign national mortgage broker hold?

Trust in a broker starts with verifiable credentials. FCA authorisation is mandatory for any broker advising on regulated UK residential mortgages, and you can confirm a broker’s status at any time through the public FCA Register at register.fca.org.uk. If a broker cannot provide their FCA reference number, do not proceed.

Beyond the regulatory minimum, the recognised professional standard for UK mortgage advisers is the Certificate in Mortgage Advice and Practice, known as CeMAP. This qualification covers UK lending law, product knowledge, and mortgage regulation. Specialist foreign national brokers typically hold CeMAP alongside additional knowledge of international lending policies, non-resident underwriting criteria, and cross-border income assessment.

When assessing a broker, ask the following questions directly:

- Are you FCA-authorised, and what is your FCA reference number?

- Do you hold CeMAP or an equivalent regulated qualification?

- How many foreign national mortgage applications have you completed in the past 12 months?

- Which specialist lenders do you have direct relationships with for non-resident borrowers?

- How do you charge: client fee, lender commission, or both?

That last question matters more than many borrowers realise. Fee structures vary widely, and a broker who earns commission from a lender has a different incentive structure from one who charges you a flat advisory fee. Neither model is inherently wrong, but you deserve to know which applies before you commit.

Buy-to-let mortgages for foreign nationals sit outside FCA regulation in most cases, meaning brokers in this space are not legally required to be FCA-authorised. However, many reputable specialist brokers choose voluntary FCA registration even for buy-to-let work, which is a useful indicator of professional standards.

How do brokers prepare foreign income documentation for UK lenders?

This is where the foreign national mortgage broker role becomes genuinely technical, and where the difference between a specialist and a generalist is most visible. Brokers act as translators between your international financial profile and the specific format each UK lender’s underwriting team requires.

The process typically follows these steps:

- Income assessment. The broker reviews your payslips, employment contract, and tax returns in their original form. If you are self-employed abroad, they will also assess business accounts and director’s loan records.

- Currency conversion. Foreign income must be converted to sterling using bank-mandated exchange rates, and lenders frequently apply a haircut to the converted figure to account for currency volatility. A specialist broker knows which lenders apply the smallest haircuts and which currencies they accept without restriction.

- Certified translation. Any document not in English requires a certified translation from a qualified translator. The broker coordinates this and confirms the translation meets the specific lender’s requirements, because standards differ between institutions.

- Credit profile positioning. UK lenders cannot access overseas credit files. The broker explains your credit history through alternative evidence: bank statements, utility payments, rental agreements, and reference letters from overseas financial institutions.

- Lender matching. With the full documentation package assembled, the broker identifies the two or three lenders most likely to approve the application based on your specific profile, then submits to the strongest candidate first.

Pro Tip: Never submit a mortgage application to multiple lenders simultaneously without broker guidance. Each application triggers a hard credit search on your UK credit file, and multiple searches in a short period reduce your credit score and signal financial distress to lenders.

The documentation stage is where most self-managed foreign national applications fail. A lender’s underwriting team will not coach you through what they need. They will simply decline and move on. A broker who has prepared dozens of similar packages knows precisely what each lender expects, which removes the guesswork entirely.

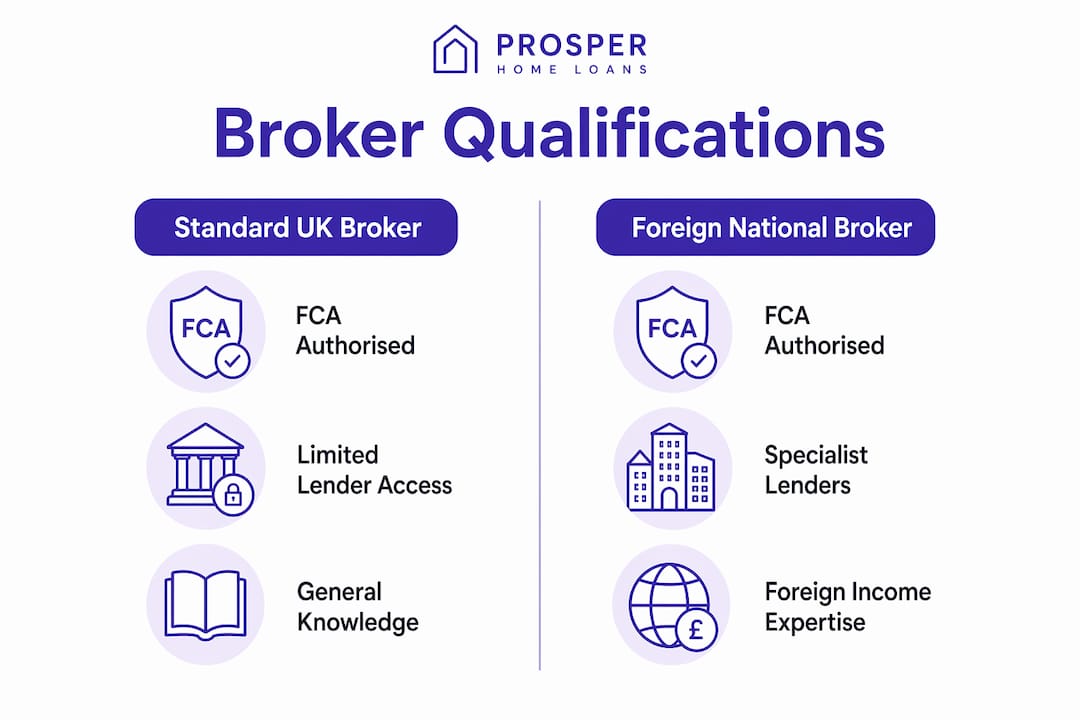

Foreign national broker versus standard UK broker: what is the difference?

Understanding foreign national mortgages requires recognising that not all mortgage brokers offer the same service. The table below summarises the core differences between a specialist foreign national broker and a standard UK mortgage adviser.

| Area | Standard UK broker | Foreign national specialist broker |

|---|---|---|

| Lender panel access | Mainstream and some specialist lenders | Specialist and non-resident lender panels including Halifax, Skipton, and Hodge |

| Immigration status knowledge | Limited or none | Detailed understanding of ILR, skilled worker, family, and non-resident visa categories |

| Foreign income handling | Not equipped for currency conversion or overseas tax returns | Experienced in currency haircuts, certified translations, and multi-jurisdiction income |

| Credit profile assessment | UK credit file only | Alternative evidence methods for borrowers without UK credit history |

| Application monitoring | Standard follow-up | Active liaison with underwriters throughout, particularly on complex cases |

| Client outcome | Suitable for straightforward UK resident applications | Suited to non-resident, visa holder, and overseas income cases |

The distinction matters because a well-intentioned standard broker who takes on a foreign national case without the right expertise can cause real damage. Submitting incomplete documentation, approaching the wrong lender, or misrepresenting income in the application can result in a declined record on your credit file that affects future applications for up to six years.

Foreign buyer mortgage options are genuinely broader than most people expect, but only a specialist broker has the lender relationships and technical knowledge to access the full range. This is the core value of the role.

Key takeaways

A specialist foreign national mortgage broker is the single most important factor in whether a non-UK resident secures mortgage finance in the UK, because lender access, documentation preparation, and eligibility assessment all require expertise that generalist advisers do not hold.

| Point | Details |

|---|---|

| Immigration status determines eligibility | ILR holders access mainstream lenders; visa holders need specialist lenders with larger deposits. |

| FCA authorisation is non-negotiable | Verify any broker’s status via the FCA Register before sharing financial information. |

| Documentation preparation is technical | Foreign income requires currency conversion, certified translations, and lender-specific formatting. |

| Specialist lender access is critical | Foreign national brokers hold panels including Halifax, Skipton, and Hodge, unavailable to general brokers. |

| Fee transparency protects you | Ask upfront whether the broker charges a client fee, lender commission, or both. |

Why I think most foreign nationals underestimate what a specialist broker actually does

From my experience working with overseas buyers and non-resident applicants, the biggest misconception I encounter is that a broker is simply someone who fills in forms. The reality is that a skilled foreign national mortgage broker is doing something far more sophisticated: they are building a case for a lender’s underwriting team that would otherwise have no framework for assessing you.

Lender behaviour has shifted noticeably in 2026. Several mainstream banks have tightened their non-resident policies following currency volatility, and a handful of specialist lenders have quietly expanded their criteria for skilled worker visa holders. A broker who is not actively monitoring these changes will be working from outdated assumptions, which directly harms their clients.

I also think the fee conversation puts too many people off seeking proper advice. Yes, some brokers charge a client fee on top of lender commission. But consider the alternative: a declined application, a damaged credit file, and months lost. The cost of good specialist advice is almost always smaller than the cost of getting it wrong. Ask about fees clearly, understand the structure, and then make a decision based on the full picture rather than the headline number.

Choosing a broker who holds CeMAP qualification and FCA authorisation, and who can name the specialist lenders they work with directly, is the most reliable way to protect yourself in what is genuinely a complex market.

— Paul

How Prosperhomeloans supports foreign nationals with expert mortgage advice

Prosperhomeloans is an FCA-authorised independent mortgage and protection adviser with direct experience handling foreign national mortgage applications across a range of visa categories and income profiles. We work with clients who earn in foreign currencies, hold skilled worker or family visas, and are purchasing UK property from abroad. Our access to specialist lender panels, including non-resident and overseas income products, means we can identify options that standard brokers simply cannot reach. If you are a foreign national looking to buy property in the UK and want clear, honest guidance on your eligibility and the options available to you, speak to our team today for a no-obligation conversation.

FAQ

What does a foreign national mortgage broker do?

A foreign national mortgage broker assesses your immigration status, income profile, and documentation, then matches your application to specialist UK lenders equipped to consider non-resident and overseas income cases. They prepare and position your financial evidence in the specific format each lender’s underwriting team requires.

Do foreign nationals need a specialist broker or can any broker help?

A specialist broker is strongly advisable. Standard UK brokers typically lack access to the specialist lender panels and the technical knowledge needed to handle foreign income, currency conversion, and non-resident credit profiles correctly.

How much deposit does a foreign national need for a UK mortgage?

Deposit requirements depend on immigration status. ILR holders can access up to 95% loan-to-value with mainstream lenders, while skilled worker and family visa holders typically need 10 to 25%. Non-resident foreign nationals purchasing from abroad often face requirements of 25 to 40%.

How do I verify that a mortgage broker is FCA-authorised?

You can check any broker’s status on the public FCA Register at register.fca.org.uk using their name or FCA reference number. FCA authorisation is a legal requirement for advising on regulated UK residential mortgages.

Do foreign national mortgage brokers charge fees?

Fee structures vary between brokers. Some charge a client advisory fee, some earn commission from the lender, and some use a combination of both. Ask your broker to confirm their fee structure in writing before proceeding with an application.