EWS1 form mortgage impact explained for flat buyers

The EWS1 form is defined as a standardised document used by mortgage lenders to assess fire safety risks in a residential building’s external wall system before approving a loan on a flat. It is not a legal requirement but functions as a vital commercial tool that most high-street lenders effectively demand before they will proceed with a mortgage valuation. Understanding the EWS1 form mortgage impact explained in full means knowing that it covers the building as a whole, remains valid for five years, and directly shapes whether your mortgage is approved, your property is valued fairly, and your sale can complete.

What does the EWS1 form mortgage impact mean for buyers?

The EWS1 form, formally known as the External Wall System fire review form, was introduced after the Grenfell Tower fire to give lenders a consistent way to evaluate cladding risk. RICS, the Royal Institution of Chartered Surveyors, developed and governs the form. Its purpose is strictly commercial: as RICS confirms, the EWS1 assists valuation and lending risk evaluation, not life safety certification. That distinction matters enormously for buyers who assume a clean EWS1 rating means the building is fully fire-safe.

For mortgage purposes, the form tells a lender whether the external walls of a block of flats present an acceptable financial risk. Without it, many lenders will simply decline to offer a mortgage, regardless of how desirable the property is. The impact on buyers is direct: no EWS1 form can mean no mortgage offer, no sale, and no ability to remortgage.

Pro Tip: Ask the seller or estate agent for the EWS1 form before you instruct a solicitor. Discovering a missing or poor-rated form late in the process costs time and money.

How do the 2026 RICS standards change when EWS1 is needed?

RICS updated its standards, effective november 2026, to set clearer and more proportionate criteria for when an EWS1 form should be requested. The aim is to reduce unnecessary delays on properties that present little or no cladding risk. The new guidance distinguishes between buildings based on height and cladding type.

The key thresholds work as follows:

- Buildings over six storeys: An EWS1 form is generally required where cladding or combustible materials are present on the external wall.

- Buildings of five to six storeys: An EWS1 form is required where specific risk indicators exist, such as certain cladding types or balcony configurations with combustible materials.

- Buildings of four storeys or fewer: These are often exempt unless specific risk indicators are present, reducing unnecessary paperwork and cost.

- Alternatives to EWS1: In some scenarios, a PAS 9980 appraisal report may be accepted as an alternative assessment route, particularly where a full EWS1 is disproportionate to the risk level.

The 2026 update reflects a broader push for proportionality. Lenders and valuers are now expected to apply the criteria carefully rather than requesting an EWS1 form as a default on every flat. This should, in practice, free up transactions on lower-risk buildings that were previously stalled unnecessarily.

Pro Tip: If your lender requests an EWS1 form on a low-rise building with no cladding, ask them to confirm their rationale under the 2026 RICS standards. You may be able to challenge an unnecessary request.

What do EWS1 ratings mean for your mortgage?

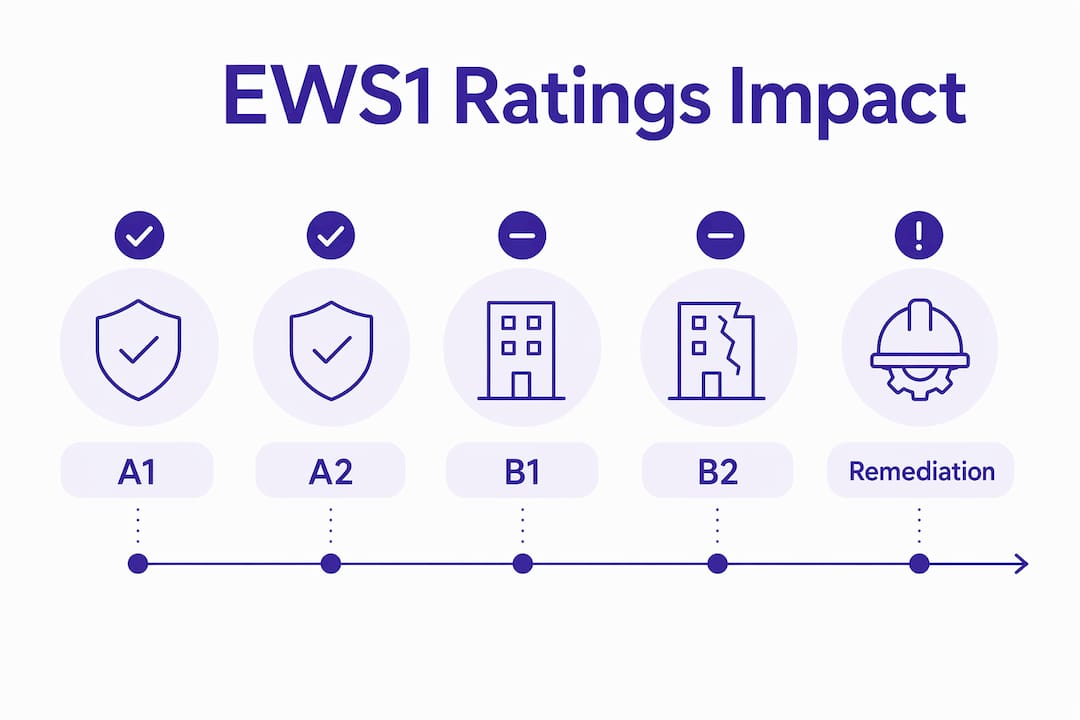

The EWS1 form uses a lettered rating system to categorise the fire risk of a building’s external wall. Each rating carries a direct consequence for mortgage lending and property value.

| Rating | Meaning | Mortgage impact |

|---|---|---|

| A1 | No cladding or attachments requiring further assessment | Generally accepted by lenders without conditions |

| A2 | Cladding present but assessed as low risk | Generally accepted; some lenders may request further detail |

| A3 | Cladding present with higher risk profile | Accepted by most lenders but may affect valuation |

| B1 | Combustible materials present but risk assessed as acceptable | Accepted by most lenders; buyer should verify Building Safety Act protections |

| B2 | Significant fire risk identified; remediation required | Often blocks mortgage approval until remediation is complete |

Ratings A1 through B1 are usually accepted by lenders, though individual lender policies vary. A B2 rating is the most serious outcome. It signals that the external wall system presents a high fire risk and that remediation works are needed before most lenders will proceed. Properties with a B2 rating can become effectively unmortgageable until those works are completed and a revised assessment is issued.

The impact on property value is equally significant. A B2 rating can cause a valuer to reduce the assessed value of a flat substantially, or to decline to value it at all. Even a B1 rating can prompt a valuer to flag uncertainty, which may lead to a lender offering a lower loan-to-value ratio. Buyers should treat the EWS1 rating as a core part of their due diligence, not an afterthought.

Pro Tip: If a property carries a B2 rating, check whether a remediation plan is already in place and funded. A clear, costed plan can sometimes allow a sale to proceed, depending on the lender.

Who is responsible for obtaining an EWS1 form?

Individual leaseholders cannot commission an EWS1 form. Only the freeholder or the building’s management company has the authority to do so. This is one of the most frustrating aspects of the process for buyers and sellers alike, because it removes direct control from the people most affected by the outcome.

If you are buying a leasehold flat and no EWS1 form exists, your options are limited but not exhausted. Here is what you can do:

- Contact the freeholder or managing agent directly. Request confirmation of whether an EWS1 form has been commissioned and ask for a timeline.

- Engage your solicitor. A solicitor experienced in leasehold matters can write formally to the freeholder and apply pressure through legal channels.

- Check service charge arrangements. Leaseholders may be able to recover assessment costs via the lease’s service charge provisions, which can incentivise the freeholder to act.

- Review Building Safety Act 2022 protections. If the building qualifies, leaseholder protections may limit your liability for remediation costs even if a poor rating is issued.

The Building Safety Act 2022 introduced significant protections for leaseholders. Crucially, these protections transfer when a qualifying lease is sold, meaning a new buyer inherits them. However, they do not apply to non-qualifying leases or to buildings under 11 metres in height. Your solicitor must confirm which protections apply before you exchange contracts.

Buildings that are exempt from requiring an EWS1 form include:

- Buildings of four storeys or fewer with no specific risk indicators under the 2026 RICS criteria.

- Buildings with no cladding or combustible attachments on the external wall.

- Buildings where a PAS 9980 appraisal has already been completed and accepted by the lender.

How does EWS1 status affect your mortgage application?

Mortgage lenders use the EWS1 form to make decisions on property valuations, mortgage approvals, remortgaging, and sales eligibility. Uncertainty about external wall safety causes lenders to act cautiously, and the consequences for buyers can be severe.

The practical effects on your mortgage application include:

- Mortgage refusal. A lender may decline to offer a mortgage entirely if no EWS1 form is available or if the rating is B2.

- Valuation reductions. A valuer may reduce the assessed value of the property to reflect fire safety risk, which reduces the amount a lender will lend.

- Transaction delays. Waiting for a freeholder to commission and complete an EWS1 assessment can take months, stalling a sale or purchase.

- Remortgaging difficulties. Homeowners seeking to remortgage a flat may find their current lender or a new lender unwilling to proceed without an up-to-date EWS1 form.

- Resale complications. Sellers of flats in affected buildings must disclose EWS1 status to buyers, and a poor rating or missing form can reduce the pool of buyers who can obtain a mortgage.

The importance of a clear remediation plan cannot be overstated. Where a B2 rating exists, lenders want to see a funded, time-bound plan for the works before they will consider lending. A vague promise of future remediation is not sufficient. Buyers should request written confirmation of any remediation programme and its funding source before proceeding.

Key takeaways

The EWS1 form is a commercial lending tool, not a fire safety certificate, and its rating directly determines whether a mortgage on a leasehold flat can proceed.

| Point | Details |

|---|---|

| EWS1 is not a legal requirement | Lenders treat it as essential for mortgage approval on flats with cladding risk. |

| 2026 RICS standards reduce unnecessary requests | Buildings of four storeys or fewer are often exempt under the updated criteria. |

| B2 rating blocks most mortgages | Remediation must be completed and reassessed before most lenders will proceed. |

| Only freeholders can commission the form | Leaseholders must engage managing agents or solicitors to apply pressure. |

| Building Safety Act 2022 protections transfer | New buyers inherit leaseholder protections on qualifying leases when they purchase. |

Paul’s perspective on EWS1 and the mortgage market in 2026

The single biggest misconception I see is buyers treating the EWS1 form as a fire safety certificate. It is not. RICS is explicit that the form assists valuation and lending, nothing more. Confusing the two leads buyers to either panic unnecessarily or, worse, to assume a clean rating means the building is safe in every sense.

What I have found consistently is that early engagement makes the biggest difference. Buyers who ask about EWS1 status before they make an offer are in a far stronger position than those who discover a problem at the mortgage valuation stage. The 2026 RICS update is genuinely helpful in reducing delays on lower-risk buildings, but it does not solve the core problem: freeholders still control the process, and some are slow to act.

My advice is to treat the EWS1 form as you would a structural survey. Get the information early, understand what the rating means for your specific lender, and take legal advice on Building Safety Act protections before you commit. The market is improving, but it rewards buyers who are prepared.

— Paul

How Prosperhomeloans can help with EWS1 mortgage challenges

Dealing with EWS1 complications during a mortgage application is stressful, but you do not have to work through it alone. At Prosperhomeloans, we work with buyers and homeowners who face exactly these situations every day.

We understand how EWS1 ratings affect lender decisions, valuation outcomes, and your ability to buy, sell, or remortgage a flat. As independent mortgage advisors, we have access to a wide panel of lenders and know which ones take a more flexible approach to EWS1-affected properties. Whether you are facing a B1 or B2 rating, a missing form, or a delayed assessment, we can help you understand your options and find the right mortgage solution for your circumstances. Get in touch with Prosperhomeloans for a no-obligation conversation about your situation.

FAQ

What is an EWS1 form used for?

The EWS1 form is used by mortgage lenders and valuers to assess fire safety risks in a residential building’s external wall system. It is a commercial tool for lending decisions, not a statutory fire safety certificate.

Does every flat need an EWS1 form?

Not every flat requires an EWS1 form. Under 2026 RICS standards, buildings of four storeys or fewer are often exempt unless specific risk indicators such as cladding or combustible balcony materials are present.

What happens if a flat has a B2 EWS1 rating?

A B2 rating indicates significant fire risk and generally prevents mortgage approval until remediation works are completed and a revised assessment is issued. Buyers should check whether Building Safety Act 2022 protections apply to limit their cost liability.

Can I get a mortgage on a flat without an EWS1 form?

Some lenders will proceed without an EWS1 form if the building meets exemption criteria under the 2026 RICS standards. Where a form is required and absent, most lenders will not offer a mortgage until one is provided.

Who pays for an EWS1 assessment?

The freeholder or management company commissions and typically pays for the EWS1 assessment. Leaseholders may be able to recover costs through service charge arrangements, but they cannot commission the form directly.