Construction worker mortgage lender criteria: 2026 guide

Construction worker mortgage lender criteria are specialised requirements focused on verifying CIS income, contract continuity, and industry-specific financial practices that standard PAYE assessments cannot capture. Most lenders require a minimum of 12 months of CIS income history, though some flexible providers accept as little as 3 months. If you work under the Construction Industry Scheme as a subcontractor, sole trader, or self-employed director, the mortgage process looks different from what a salaried employee faces. Prosperhomeloans works with construction workers every day to cut through that complexity and find lenders who genuinely understand how contractor income works.

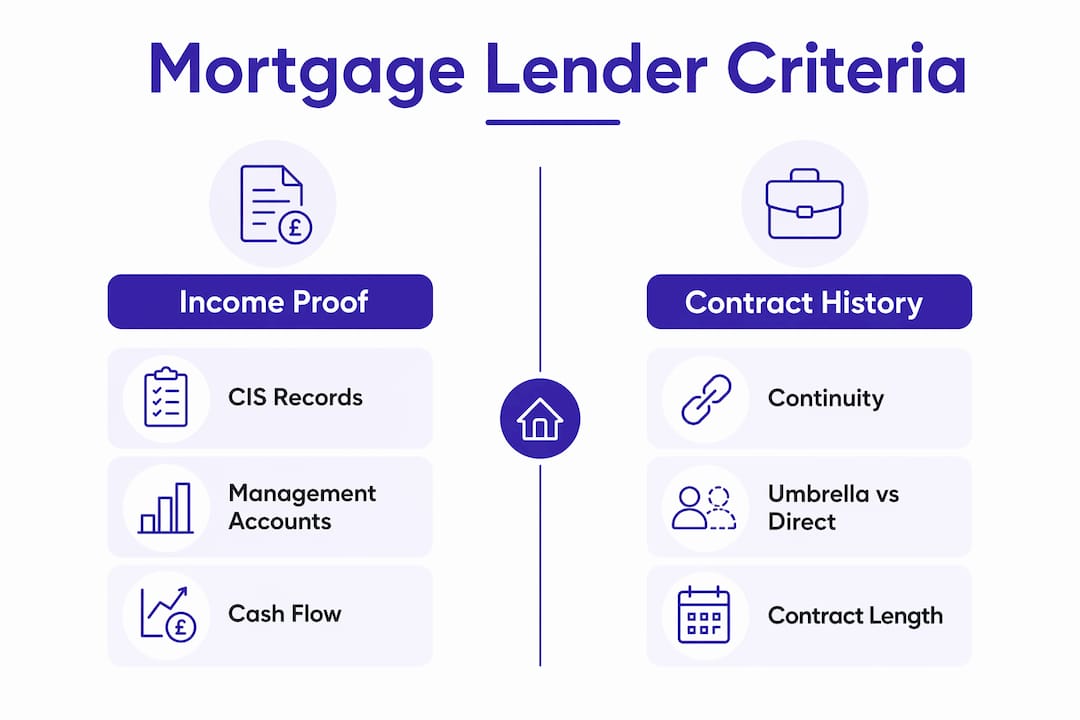

What income documentation do mortgage lenders require from construction workers?

Lenders assess construction worker income differently from PAYE employment because the money arrives through CIS deductions rather than a standard payslip. The minimum 12 months CIS history is the standard benchmark, though some flexible lenders will consider applications with as little as 3 months of CIS payslips if you can show a solid, unbroken track record in the same trade or sector. That flexibility matters if you have recently moved from employed to self-employed status.

The documents lenders typically request include:

- CIS payslips or monthly statements covering at least 12 months, showing gross payments and tax deductions

- SA302 tax calculations and the corresponding tax year overviews from HMRC, usually for the past two years

- Accountant-certified accounts if you operate as a limited company or sole trader with multiple income streams

- Current and previous contracts to confirm the nature and continuity of your work

- Umbrella company payslips if you operate through an umbrella arrangement, showing gross pay before deductions

For day-rate contractors, lenders commonly multiply your weekly rate by 46 weeks to calculate your annual income. That figure, rather than your net take-home pay, becomes the basis for affordability. This is a significant advantage if you have been presenting only net figures on previous applications.

Pro Tip: Ask your accountant to prepare a CIS income summary that separates gross contract payments from tax deductions. Presenting gross figures clearly can substantially increase the income a lender will use for affordability calculations.

How do lenders assess financial stability beyond income proof?

Income documents alone do not satisfy a lender’s full assessment. Banks and building societies also examine the financial health of your business through management accounts, cash flow forecasts, and construction-specific schedules.

Lenders want management accounts no older than three months and a 12-month cash flow forecast to assess financial stability. This requirement catches many construction workers off guard, particularly those who only prepare annual accounts. Up-to-date management accounts signal that your business is actively monitored and financially sound.

Retentions are another area where lenders frequently misread construction finances. Retentions of around 5% held by main contractors can appear as aged debt on your balance sheet, which raises red flags unless they are clearly labelled and explained as standard industry practice. A well-prepared set of accounts will separate retention debtors from overdue invoices so an underwriter does not confuse the two.

Work In Progress (WIP) schedules and order books serve as forward revenue evidence. They show a lender that you have contracted work ahead, reducing the perceived risk of income gaps. The table below summarises the key financial documents and what each one demonstrates to a lender.

| Document | What it demonstrates |

|---|---|

| Management accounts (under 3 months old) | Current trading position and business health |

| 12-month cash flow forecast | Ability to sustain income and meet repayments |

| WIP schedule and order book | Forward revenue and pipeline of contracted work |

| Retention debtor schedule | Clarifies aged-looking balances as industry-standard holdbacks |

| VAT reverse charge explanation | Confirms compliance with construction VAT rules |

Pro Tip: Ask your accountant to include a brief narrative note in your management accounts explaining retentions and VAT reverse charges. Underwriters unfamiliar with construction accounting will read that note before making a decision.

What contract and employment history criteria must construction workers meet?

Contract continuity is one of the most scrutinised areas of any construction mortgage application. Lenders want to see that your work history is consistent and that your current contract is live at the point of application.

The standard requirement is 12 to 24 months of continuous contracting in the same sector, with gaps between contracts of no more than six weeks. A six-week gap is considered acceptable because it reflects normal project turnaround time in construction. Longer gaps require a written explanation and, in some cases, additional income evidence to reassure the lender.

For your current contract, lenders require at least one month remaining at the point of mortgage decision, or a formal renewal intent letter from your contractor or client. The following criteria apply across most lender types:

- Minimum sector experience: 12 months in the same trade or construction discipline, with 24 months preferred by more cautious lenders.

- Current contract status: Active contract with at least one month remaining, or a signed renewal letter confirming continuation.

- Gap tolerance: Gaps of up to six weeks between contracts are generally accepted without explanation.

- Concurrent contracts: Some lenders cap the number of simultaneous contracts you can hold, as multiple short-term engagements can suggest instability rather than strength.

- Zero-hours and umbrella arrangements: These require additional evidence of consistent earnings, as the income pattern is less predictable than a fixed-term contract.

- Self-employed directors: Limited company directors must provide both personal and company accounts, along with dividend evidence if salary is drawn partly in dividends.

The distinction between umbrella employment and direct CIS subcontracting matters significantly. Umbrella workers are technically employed, so their payslips look closer to PAYE. Direct CIS subcontractors need to demonstrate gross income before deductions, which requires more careful document preparation.

What practical steps can construction workers take to improve their application?

Preparation separates successful applications from rejected ones. The most common reason construction workers receive lower mortgage offers or outright rejections is presenting net profits without first grossing up revenue. Presenting net profits without grossing up revenue in accounts can greatly reduce borrowing capacity. An accountant who understands CIS can restate your figures to show gross revenue before deductions, which directly increases the income a lender will use.

The practical steps that make the biggest difference are:

- Gross up your revenue: Work with your accountant to show gross contract income before CIS deductions and material costs, not just the net profit figure.

- Prepare a WIP schedule: List all current contracts, their values, and expected completion dates. This gives lenders a clear picture of your forward order book.

- Produce a 12-month cash flow forecast: Align projected income to your contract pipeline. Lenders treat this as evidence of future repayment capacity.

- Check your CIS tax deduction rate: Being verified at the 30% deduction rate instead of the standard 20% can raise lender concerns about tax compliance. If you are on the higher rate, get a written explanation from your accountant ready before you apply.

- Engage a specialist broker: Specialist brokers who understand non-standard incomes like CIS are vital, as traditional lender systems are built for PAYE income and may underestimate your earning potential.

- Reconcile retentions clearly: Label retention debtors separately in your accounts so they are not mistaken for bad debt.

Pro Tip: Apply for your mortgage before your current contract ends, not after. Lenders assess your position at the point of application, and an active contract with time remaining is far stronger evidence than a recently expired one.

Key takeaways

Construction workers who prepare CIS income records, management accounts, and contract documentation correctly are far more likely to secure a mortgage at the borrowing level they need.

| Point | Details |

|---|---|

| CIS income history | Most lenders require 12 months of CIS records; some accept 3 months with strong sector continuity. |

| Gross up your revenue | Presenting gross income before CIS deductions significantly increases the borrowing amount lenders will offer. |

| Management accounts currency | Accounts must be no older than 3 months, supported by a 12-month cash flow forecast. |

| Contract continuity | Lenders expect 12–24 months in the same sector with gaps of no more than six weeks between contracts. |

| Specialist broker value | Brokers familiar with CIS lending package your application correctly for lenders who understand contractor income. |

Why I think construction workers are underserved by standard mortgage advice

Most mortgage advice is written for people with a payslip and a permanent contract. That is not a criticism. It is simply a reflection of how lender systems were built, and those systems have not kept pace with how the construction industry actually works.

What I see regularly is construction workers with strong, consistent earnings being offered lower mortgage amounts than their income justifies, purely because their accounts were not presented in a way that lenders recognise. A bricklayer earning £70,000 gross through CIS should not be assessed on £35,000 net profit. The difference between those two figures is the difference between buying the home you want and settling for something smaller.

The modern contractor working patterns that are standard in construction genuinely clash with legacy lender systems. The good news is that specialist lenders and brokers are beginning to address this gap. More lenders now have dedicated contractor criteria, and the process of getting a fair assessment is more achievable than it was even three years ago. My strong advice is to engage a specialist broker before you approach any lender directly. The right broker will know which lenders have the most favourable criteria for your specific situation, whether you are a sole trader, a limited company director, or working through an umbrella arrangement. Going in without that knowledge costs you time, credit score points, and in some cases, the deal itself.

— Paul

How Prosperhomeloans helps construction workers secure the right mortgage

Getting a mortgage as a construction worker is achievable when you have the right support from the start.

Prosperhomeloans specialises in mortgage applications for contractors and CIS workers, working with a network of lenders who understand how construction income is structured. We know which lenders accept 3 months of CIS history, which ones gross up day rates correctly, and which ones have the most flexible contract gap policies. Rather than spending weeks approaching lenders who are not set up for your situation, you can work with us to identify the right fit from the outset. Contact Prosperhomeloans to discuss your circumstances and get a clear picture of what you can borrow.

FAQ

What is the minimum CIS history needed for a mortgage?

Most lenders require a minimum of 12 months of CIS income history, though some flexible providers will consider applications with as little as 3 months if you have a continuous track record in the same sector.

How do lenders calculate income for day-rate construction workers?

Lenders typically multiply your daily or weekly contract rate by 46 weeks to arrive at an annual income figure. This method is used in place of net profit figures, which often understate your actual earning capacity.

Can I get a mortgage if I have gaps between contracts?

Gaps of up to six weeks between contracts are generally accepted by lenders as normal for the construction sector. Longer gaps require a written explanation and may need supporting income evidence to satisfy the lender’s criteria.

Does my CIS tax deduction rate affect my mortgage application?

Being verified at the 30% CIS deduction rate rather than the standard 20% can raise concerns about tax compliance with some lenders. Providing a clear written explanation from your accountant before you apply will address this directly.

Do I need a specialist broker as a construction worker?

A specialist broker who understands CIS and contractor income is the most effective way to match your application to lenders whose criteria fit your situation. Standard mortgage advisors may not know which lenders assess contractor income correctly, which can result in lower offers or unnecessary rejections.