Consolidate loans with a fixed-rate mortgage: 2026 guide

Debt consolidation using a fixed-rate mortgage is defined as combining multiple unsecured debts, such as credit cards and personal loans, into a single secured loan tied to your property, with a predictable interest rate for a set term. This approach can reduce your monthly outgoings and simplify what may be several separate repayments into one. The Financial Conduct Authority (FCA) regulates this process closely, requiring lenders and advisers to assess affordability and suitability before recommending it. The trade-off is real: while you may pay less each month, spreading short-term debt over a 20–30 year mortgage term can significantly increase the total interest you pay. Understanding both sides is the foundation of any sound decision to consolidate loans with a fixed-rate mortgage.

What do you need to qualify for fixed-rate loan consolidation?

Lenders apply strict eligibility criteria before approving a debt consolidation mortgage. Meeting these requirements determines whether consolidation is even possible, let alone worthwhile.

The most important factor is your loan-to-value (LTV) ratio. Most lenders require a post-consolidation LTV below 85% to qualify for competitive rates. This means you need sufficient equity in your property to absorb the additional borrowing. If your LTV exceeds 85–90%, your options narrow considerably and the rates available will be higher.

Lenders also carry out a full affordability assessment under FCA guidelines. This includes reviewing your income, regular outgoings, and your ability to continue meeting repayments if interest rates rise. Stress testing is a standard part of this process. FCA guidance requires advisers to assess the root causes of your debt before recommending consolidation, not simply approve the request.

Your credit score matters too. A history of missed payments or defaults will reduce the number of lenders willing to offer consolidation products. Lenders also distinguish between acceptable debt types. Credit cards, personal loans, and store cards are commonly consolidated. Tax debts or court judgements are typically excluded.

Early repayment charges (ERCs) are a factor many borrowers overlook. If you are currently in a fixed-rate deal, switching early can trigger ERCs of 1%–5% of your outstanding balance. On a £200,000 mortgage, that could mean a charge of £2,000–£10,000, which may wipe out any short-term savings entirely.

Key eligibility requirements at a glance:

- Post-consolidation LTV below 85% (ideally lower for best rates)

- Sufficient and verifiable income to pass affordability stress tests

- Acceptable credit history with no recent defaults or CCJs

- Property in England, Wales, Scotland, or Northern Ireland with adequate equity

- Debts must be standard unsecured consumer credit (not tax arrears or court-ordered debts)

- Documentation including payslips, bank statements, and a list of all current debts

Pro Tip: Check your current mortgage deal’s ERC schedule before making any enquiries. If you are within the first two years of a five-year fix, the charges alone may make consolidation unviable until your deal ends.

How to consolidate multiple loans into a fixed-rate mortgage

The consolidation process follows a clear sequence. Rushing any step increases the risk of choosing a deal that costs more than it saves.

-

Calculate your total debt. List every outstanding balance, its interest rate, and its monthly repayment. Include credit cards, personal loans, and any other unsecured borrowing. Add these to your current mortgage balance to understand the total you need to borrow.

-

Assess your property equity. Get a current valuation of your property. Subtract your total mortgage balance (including the new debt) from that value to calculate your equity and resulting LTV. If the LTV exceeds 85%, consolidation through a standard remortgage may not be available to you.

-

Compare total costs, not just monthly payments. Monthly savings can mask significantly higher total interest when short-term debt is spread over 20–30 years. Use a mortgage calculator to compare the total amount repayable under each scenario, not just the monthly figure.

-

Consult a qualified mortgage adviser. An FCA-regulated adviser will assess your full financial picture and confirm whether consolidation is suitable. Professional advisers must document a clear rationale when recommending consolidation beyond your original request, protecting you from unsuitable advice.

-

Choose between a full remortgage and a second-charge mortgage. A full remortgage replaces your existing mortgage with a new, larger one. A second-charge mortgage sits alongside your existing deal as a separate secured loan. Second-charge mortgages are useful when remortgaging is unaffordable or when ERCs make switching your main mortgage too costly.

-

Submit your application. Your lender will require proof of income, bank statements, a list of debts to be consolidated, and a property valuation. The process typically takes 4–8 weeks from application to completion.

-

Understand how creditors are paid. Lenders usually pay creditors directly rather than releasing cash to you. This debt-to-debt settlement reduces the risk of funds being spent elsewhere and protects both you and the lender.

Pro Tip: Ask your adviser to model three scenarios side by side: keeping debts separate, consolidating via remortgage, and consolidating via a second-charge loan. The numbers often tell a different story than the headline monthly saving.

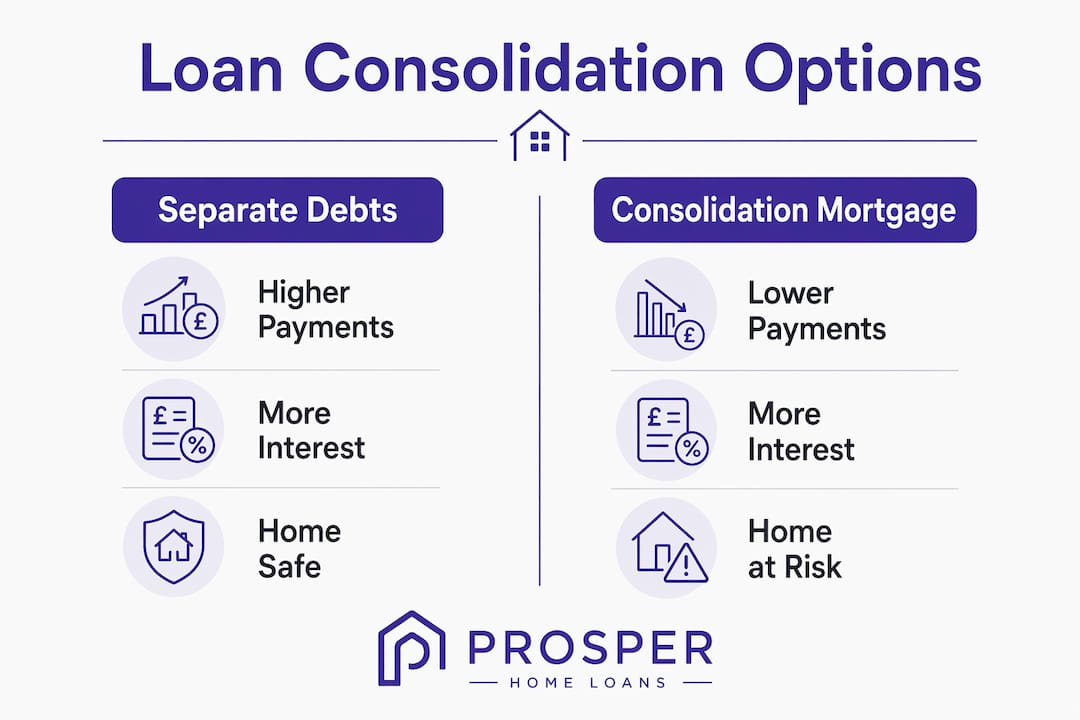

| Scenario | Monthly payment | Total interest paid | Home at risk? |

|---|---|---|---|

| Debts kept separate | Higher | Lower overall | No |

| Full remortgage consolidation | Lower | Higher over term | Yes |

| Second-charge mortgage | Moderate | Moderate | Yes |

What are the financial risks of consolidating debt with a mortgage?

The single biggest risk is one that borrowers consistently underestimate. Converting unsecured debt into secured mortgage debt means your home becomes collateral. If you miss payments, your lender can begin repossession proceedings. A credit card company cannot take your home. A mortgage lender can.

Consolidating unsecured debt into a mortgage does not reduce what you owe. It changes who holds the risk. The debt moves from your credit file to your front door. If your circumstances change and payments become unaffordable, the consequences are far more serious than a damaged credit score.

Beyond repossession risk, the most common pitfalls include:

- Ignoring ERCs. Switching mid-deal can cost thousands. Always check your current mortgage terms before proceeding.

- Underestimating total interest. Lower monthly repayments do not guarantee long-term savings. Spreading £15,000 of credit card debt over 25 years at a mortgage rate still generates substantial interest.

- Failing the affordability stress test. Lenders test your ability to pay if rates rise. If your finances are already stretched, you may not pass.

- Repeating the same spending patterns. Consolidation clears your credit cards but does not close them. Without a change in financial behaviour, many borrowers accumulate new unsecured debt on top of the enlarged mortgage.

- Overlooking FCA alternatives. The FCA emphasises that advisers must explore alternatives such as Debt Management Plans before recommending consolidation. These options do not put your home at risk.

- Choosing the wrong product. Consolidation mortgages carry higher rates than standard remortgages because lenders view them as higher risk. Comparing only the headline rate without accounting for arrangement fees and total cost leads to poor decisions.

How do you choose the best fixed-rate consolidation mortgage?

Selecting the right product requires comparing more than the interest rate. The best fixed-rate consolidation mortgage for your situation depends on several factors working together.

Interest rate and arrangement fees. A low headline rate with a high arrangement fee can cost more than a slightly higher rate with no fee. Always calculate the total cost of the deal over the fixed term, not just the monthly repayment.

Loan term length. A shorter term means higher monthly payments but significantly less total interest. A longer term reduces monthly pressure but increases the overall cost. The right balance depends on your current cash flow and long-term financial goals.

LTV and rate tiers. Post-consolidation LTV below 85% unlocks better rates. If your LTV sits at 80%, you access a meaningfully different rate tier than at 88%. Reducing your borrowing slightly, if possible, can shift you into a lower band.

Second-charge versus full remortgage. A second-charge loan is worth considering when your existing mortgage rate is very competitive and you do not want to lose it. Second-charge mortgages account for less than 4% of regulated mortgage sales for debt consolidation, but they are a legitimate and sometimes preferable route.

FCA regulation compliance. Only use lenders and advisers authorised by the FCA. This protects you through mandatory suitability assessments and gives you access to the Financial Ombudsman Service if something goes wrong.

Pro Tip: Do not apply to multiple lenders directly. Each hard credit search leaves a mark on your file. Use an FCA-regulated broker who can search the market on your behalf using a single soft search.

Key takeaways

Consolidating debt into a fixed-rate mortgage can reduce monthly payments, but the total interest cost over a longer term is almost always higher than keeping debts separate and paying them off quickly.

| Point | Details |

|---|---|

| LTV is the gateway | You need a post-consolidation LTV below 85% to access competitive fixed rates. |

| ERCs can cancel savings | Early repayment charges of 1%–5% may outweigh any monthly saving from consolidating mid-deal. |

| Secured debt raises the stakes | Moving unsecured debt to a mortgage puts your home at risk if repayments become unaffordable. |

| Total cost beats monthly payment | Always compare total interest over the full term, not just the reduction in monthly outgoings. |

| Second-charge loans are an option | When remortgaging is too costly, a second-charge mortgage can consolidate debt without losing your existing rate. |

My honest view on fixed-rate mortgage consolidation

I have seen consolidation work well for people who go in with clear eyes and a realistic plan. I have also seen it go badly wrong for people who focused only on the monthly saving and ignored everything else.

The cases that concern me most are those where someone consolidates £20,000 of credit card debt into a 25-year mortgage, feels immediate relief from the lower monthly payment, and then rebuilds the same credit card balances within two years. They now have a larger mortgage and the same unsecured debt. The consolidation achieved nothing except putting their home at greater risk.

The FCA’s requirement for advisers to explore alternatives like Debt Management Plans before recommending consolidation exists for good reason. For some people, a structured repayment plan that keeps debt unsecured is genuinely safer, even if the monthly payment is higher. The question is not just “can I afford the consolidated payment?” but “what happens if my income drops, my rate rises, or my circumstances change?”

That said, for someone with genuine equity, a stable income, and the discipline to close or reduce credit limits after consolidation, a fixed-rate mortgage can be a sound tool. The fixed rate removes interest rate uncertainty. The single payment simplifies budgeting. The key is treating it as a financial reset, not a financial shortcut. Get proper advice from an FCA-regulated adviser who will model the full picture, not just the headline numbers.

— Paul

How Prosperhomeloans can help with debt consolidation mortgages

Prosperhomeloans is an independent, FCA-regulated mortgage and protection adviser specialising in finding the right consolidation mortgage for your specific circumstances.

We assess your full financial position, including your existing mortgage, outstanding debts, income, and property equity, before recommending any product. We search across the market to find fixed-rate consolidation options that match your LTV, credit profile, and affordability. Whether a full remortgage or a second-charge mortgage is the better fit, we explain the trade-offs clearly so you can make a confident, informed decision. We handle the paperwork, liaise with lenders, and keep the process straightforward from start to finish.

FAQ

What is a debt consolidation mortgage?

A debt consolidation mortgage is a secured loan that combines multiple unsecured debts, such as credit cards and personal loans, into a single mortgage repayment. It is typically arranged as a remortgage or a second-charge loan against your property.

Does consolidating debt into a mortgage save money?

It can reduce your monthly payment, but total interest often increases when short-term debt is spread over a longer mortgage term. Always compare the total cost over the full term before deciding.

What LTV do I need to consolidate loans into a mortgage?

Most lenders require a post-consolidation LTV below 85%. A lower LTV, such as 75% or 80%, gives you access to better rates and a wider choice of lenders.

Are there risks to consolidating unsecured debt into a mortgage?

Yes. The primary risk is that your home becomes security for what was previously unsecured debt. If you cannot maintain repayments, your lender can pursue repossession.

What is a second-charge mortgage and when should I use one?

A second-charge mortgage is a separate secured loan that sits alongside your existing mortgage. It is worth considering when your current mortgage has a competitive rate you do not want to lose, or when early repayment charges make a full remortgage too expensive.